Bank of America 2004 Annual Report Download - page 36

Download and view the complete annual report

Please find page 36 of the 2004 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

|

|

BANK OF AMERICA 2004 35

All Other

Net Income increased $623 million, or 103 percent, to $1.2 billion in

2004. This increase was driven by a $1.1 billion increase in Gains on

Sales of Debt Securities. In addition, Total Revenue increased $318

million, or 43 percent, to $1.1 billion due to improvements in both

Latin America and Equity Investments. Partially offsetting these

increases was a $607 million increase in Noninterest Expense,

driven by $618 million of Merger and Restructuring Charges. For

more information on All Other, see page 49.

Financial Highlights

Net Interest Income

Net Interest Income on a FTE basis increased $7.4 billion to $29.5

billion in 2004. This increase was driven by the impact of the Merger,

higher asset and liability management (ALM) portfolio levels (prima-

rily consisting of securities and whole loan mortgages), the impact of

higher rates, growth in consumer loan levels (primarily credit card and

home equity) and higher core deposit funding levels. Partially offset-

ting these increases were reductions in the large corporate and for-

eign loan balances, lower trading-related contributions, lower

mortgage warehouse levels and the continued runoff of previously

exited consumer businesses. The net interest yield on a FTE basis

declined 14 basis points (bps) to 3.26 percent due to the negative

impact of increased trading-related balances, which have a lower yield

than other earning assets. For more information on Net Interest

Income on a FTE basis, see Table

I

on page 84.

Noninterest Income

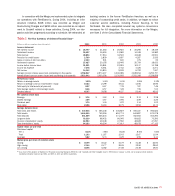

Noninterest Income

(Dollars in millions) 2004 2003

Service charges $ 6,989 $ 5,618

Investment and brokerage services 3,627 2,371

Mortgage banking income 414 1,922

Investment banking income 1,886 1,736

Equity investment gains 861 215

Card income 4,588 3,052

Trading account profits 869 409

Other income 863 1,127

Total noninterest income $ 20,097 $16,450

Noninterest Income increased $3.6 billion to $20.1 billion in 2004,

due primarily to the addition of FleetBoston, which contributed

$3.8 billion of Noninterest Income.

•Service Charges grew $1.4 billion driven by organic account

growth and approximately $960 million from the addition of

FleetBoston customers.

•Investment and Brokerage Services increased $1.3 billion due

to approximately $1.1 billion related to the addition of the

FleetBoston business as well as market appreciation.

•Mortgage Banking Income decreased $1.5 billion caused by

lower production levels, a decrease in the gains on sales of

loans to the secondary market and writedowns of the value of

Mortgage Servicing Rights (MSRs).

•Investment Banking Income increased $150 million on

increased market share in a variety of products.

•Equity Investment Gains increased $646 million due to a $576

million increase in Principal Investing gains.

•Card Income increased $1.5 billion due to increased fees and

interchange income, including the $832 million impact from the

addition of the FleetBoston card portfolio.

•Trading Account Profits increased $460 million due to

increased customer activity.

•Other Income decreased $264 million due to the absence of

whole mortgage loan sale gains in 2004, partially offset by the

addition of FleetBoston.

For more information on Noninterest Income, see Business Segment

Operations beginning on page 40.

Gains on Sales of Debt Securities

Gains on Sales of Debt Securities in 2004 were $2.1 billion compared

to $941 million in 2003, as we continued to reposition the ALM port-

folio in response to interest rate fluctuations and to manage mortgage

prepayment risk. For more information on Gains on Sales of Debt

Securities, see Market Risk Management beginning on page 72.

Provision for Credit Losses

The Provision for Credit Losses decreased $70 million to $2.8 billion

in 2004 driven by lower commercial net charge-offs of $748 million

and continued improvements in credit quality in the commercial loan

portfolio. Offsetting these decreases were increases in the Provision

for Credit Losses in our consumer credit card portfolio. These

increases included higher credit card net charge-offs of $791 million,

of which $320 million was attributed to the addition of the

FleetBoston credit card portfolio. Organic growth, overall seasoning of

credit card accounts, the return of securitized loans to the balance

sheet, and increases in minimum payment requirements drove higher

net charge-offs and Provision for Credit Losses. For more information

on credit quality, see Credit Risk Management beginning on page 58.