Bank of America 2004 Annual Report Download - page 46

Download and view the complete annual report

Please find page 46 of the 2004 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

|

|

BANK OF AMERICA 2004 45

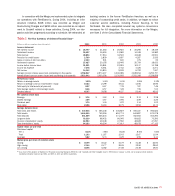

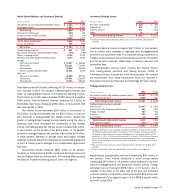

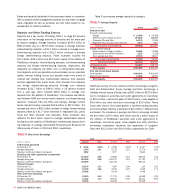

Consumer Deposit Products

Consumer Deposit Products provides a comprehensive range of deposit

products to consumers and small businesses. Our deposit products

include traditional savings accounts, money market savings accounts,

CDs and IRAs, regular and interest checking accounts, and a variety of

business checking options. These products are further segmented to

address customer specific needs and our multicultural strategy.

We added approximately 2.1 million net new checking accounts

and 2.6 million net new savings accounts during 2004. This growth

resulted from continued improvement in sales and service results in

the Banking Center Channel, improved cross-sale ratios, the intro-

duction of new products, advancement of our multicultural strategy,

and access to the former FleetBoston franchise, where we opened

174,000 net new checking and 193,000 net new savings accounts

since April 1, 2004. Account growth has occurred through productivity

improvements in existing stores, as well as new store openings,

which totaled 167 in 2004.

We generate revenue on deposit products through the results of

a funds transfer pricing process that matches assets and liabilities

with similar interest rate sensitivity and maturity characteristics, fees

generated on our accounts, and interchange income from our debit

cards. Our deposit-taking activities are integrally linked to our liquid-

ity management and ALM interest rate risk management processes.

We seek to optimize the value of deposits through both our client-fac-

ing asset generation and our ALM investment process. The following

table presents the components of Total Revenue for Consumer

Deposit Products.

Consumer Deposit Products Revenue

(Dollars in millions) 2004 2003

Net interest income $ 7,735 $ 5,647

Deposit service charges 4,496 3,577

Debit card income 1,232 896

Total noninterest income 5,728 4,473

Total deposit revenue(1) $ 13,463 $ 10,120

(1) Deposit revenue outside of Global Consumer and Small Business Banking was $985 and $666,

respectively, for 2004 and 2003.

Deposit revenue grew $3.3 billion, or 33 percent. Driving this

growth was the addition of FleetBoston, which contributed $2.1 bil-

lion of deposit revenue.

Net Interest Income increased $2.1 billion, or 37 percent. The

primary driver of the increase was the $80.3 billion, or 35 percent,

increase in average Deposits. Of this growth, $63.0 billion was related

to the addition of FleetBoston customers through the Merger. The addi-

tion of FleetBoston contributed $1.5 billion to Net Interest Income.

Deposit service charges increased $919 million, or 26 percent,

due to the $515 million impact of the addition of FleetBoston, and

the growth of new accounts across our franchise.

Debit card income increased $336 million, or 38 percent. Driving

the increase was growth in transaction activity, evidenced by a 40 percent

increase in purchase volumes, partially offset by the negative impact of

a lower interchange rate on signature debit card transactions. The impact

of the addition of FleetBoston to debit card income was $134 million.

Global Business and Financial Services

This segment provides financial solutions to our clients throughout all

stages of their financial cycles. Our strategy is to bring the capabili-

ties of a global financial services organization to the local level. We

serve our clients through a variety of businesses including Global

Treasury Services, Middle Market Banking, Commercial Real Estate

Banking, Leasing, Business Capital and Dealer Financial Services.

Beginning in 2005, Global Business and Financial Services will include

Latin America. See page 49 for more information on Latin America.

Also beginning in 2005, Global Business and Financial Services will

include Business Banking, which serves our client-managed small

business customers.

Global Treasury Services provides integrated working capital

management and treasury solutions to clients across the U.S. and

37 countries. Our clients include multi-nationals, middle market com-

panies, correspondent banks, commercial real estate firms and gov-

ernments. Our services include treasury management, trade finance,

foreign exchange, short-term credit facilities and short-term investing.

The revenues and operating results where customers and clients are

serviced are reflected in this segment, as well as Global Consumer

and Small Business Banking, and Global Capital Markets and

Investment Banking.

Middle Market Banking provides commercial lending, treasury

management products and investment banking services to middle-

market companies across the U.S.

Commercial Real Estate Banking, with offices in more than 60

cities across the U.S., provides project financing and treasury man-

agement to private developers, homebuilders and commercial real

estate firms. Commercial Real Estate Banking also includes commu-

nity development banking, which provides lending and investing serv-

ices to low- and moderate-income communities.

Leasing provides leasing solutions to small business, middle-

market and large corporations in the U.S. and internationally, offer-

ing expertise in the municipal, corporate aircraft, healthcare and

vendor markets.

Business Capital provides asset-based lending financing solu-

tions customized to meet clients' capital needs by leveraging their

assets on a secured basis in the U.S., Canada and European markets.

Dealer Financial Services provides lending and investing serv-

ices, including floor plan programs for marine, recreational vehicle and

auto dealerships to more than 10,000 dealer clients across the U.S.