Bank of America 2004 Annual Report Download - page 63

Download and view the complete annual report

Please find page 63 of the 2004 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

|

|

62 BANK OF AMERICA 2004

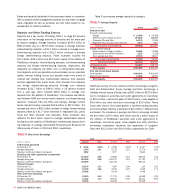

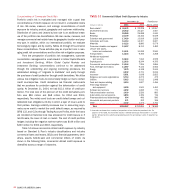

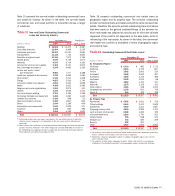

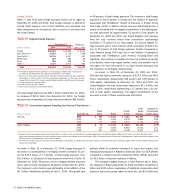

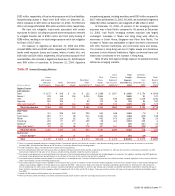

Concentrations of Commercial Credit Risk

Portfolio credit risk is evaluated and managed with a goal that

concentrations of credit exposure do not result in undesirable levels

of risk. We review, measure, and manage concentrations of credit

exposure by industry, product, geography and customer relationship.

Distribution of Loans and Leases by loan size is an additional meas-

ure of the portfolio risk diversification. We also review, measure, and

manage commercial real estate loans by geographic location and prop-

erty type. In addition, within our international portfolio, we evaluate

borrowings by region and by country. Tables 14 through 19 summarize

these concentrations. These activities play an important role in man-

aging credit risk concentrations and for other risk mitigation purposes.

From the perspective of portfolio risk management, customer

concentration management is most relevant in Global Capital Markets

and Investment Banking. Within Global Capital Markets and

Investment Banking, concentrations continue to be addressed

through the underwriting and ongoing monitoring processes, the

established strategy of “originate to distribute” and partly through

the purchase of credit protection through credit derivatives. We utilize

various risk mitigation tools to economically hedge our risk to certain

credit counterparties. Credit derivatives are financial instruments

that we purchase for protection against the deterioration of credit

quality. At December 31, 2004, we had $13.1 billion of credit pro-

tection. The total cost of the premium of the credit derivatives port-

folio was $84 million and $68 million for 2004 and 2003,

respectively. Two widely used tools are credit default swaps and col-

lateralized loan obligations (CLOs) in which a layer of loss is sold to

third parties. Earnings volatility increases due to accounting asym-

metry as we mark to market the credit default swaps, as required by

SFAS 133, and CLOs through Trading Account Profits, while the loans

are recorded at historical cost less allowance for credit losses or, if

held-for-sale, the lower of cost or market. The cost of credit portfolio

hedges including the negative mark-to-market was $144 million and

$330 million for 2004 and 2003, respectively.

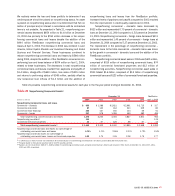

Table 14 shows commercial utilized credit exposure by industry

based on Standard & Poor’s industry classifications and includes

commercial loans and leases, SBLCs and financial guarantees, deriv-

atives, assets held-for-sale and commercial letters of credit. As

shown in the following table, commercial utilized credit exposure is

diversified across a range of industries.

Table 14

Commercial Utilized Credit Exposure by Industry

December 31 FleetBoston

(Dollars in millions) 2004 2003 April 1, 2004

■■■■■

Real estate(1) $ 36,672 $ 22,228 $ 12,957

Diversified financials 25,932 20,427 3,557

Banks 25,265 25,088 1,040

Retailing 23,149 15,152 6,539

Education and government 17,429 13,919 1,629

Individuals and trusts 16,110 14,307 2,627

Materials 14,123 8,860 5,079

Consumer durables and apparel 13,427 8,313 3,482

Leisure and sports,

hotels and restaurants 13,331 10,099 2,940

Transportation 13,234 9,355 3,268

Healthcare equipment

and services 12,643 7,064 4,939

Capital goods 12,633 8,244 4,355

Commercial services and supplies 11,944 7,206 3,866

Food, beverage and tobacco 11,687 9,134 2,552

Energy 7,579 4,348 2,044

Media 6,232 4,701 2,616

Insurance 5,851 3,638 2,822

Religious and social organizations 5,710 4,272 475

Utilities 5,615 5,012 1,948

Food and staples retailing 3,610 1,837 1,456

Technology hardware

and equipment 3,398 1,941 1,463

Software and services 3,292 1,655 770

Telecommunication services 3,030 2,526 883

Automobiles and components 1,894 1,326 746

Pharmaceuticals and biotechnology 994 466 590

Household and personal products 371 302 195

Other 3,132 1,474 3,751

■■■■■

Total $298,287 $212,894 $ 78,589

■■■■■

(1) Industries are viewed from a variety of perspectives to best isolate the perceived risks. For

purposes of this table, the real estate industry is defined based upon the borrowers’ or counter-

parties’ primary business activity using operating cash flow and primary source of repayment as

key factors.