Bank of America 2004 Annual Report Download - page 78

Download and view the complete annual report

Please find page 78 of the 2004 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

|

|

BANK OF AMERICA 2004 77

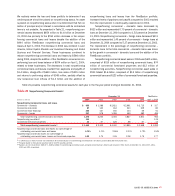

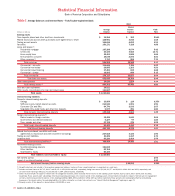

Residential Mortgage Portfolio

In 2004 and 2003, we purchased $65.9 billion and $92.8 billion,

respectively, of residential mortgages for our ALM portfolio and inter-

est rate risk management. Not included in the purchases above were

$3.3 billion of forward purchase commitments of mortgage loans at

December 31, 2004 settling from January 2005 to February 2005

and $4.6 billion at December 31, 2003 that settled in January 2004.

These commitments, included in Table

IV

on pages 88 and 89, were

accounted for as derivatives and designated as cash flow hedges,

and their net-of-tax unrealized gains and losses were included in

Accumulated OCI. During 2004, there were no sales of whole mort-

gage loans. In 2003, we sold $27.5 billion of whole mortgage loans

and recognized $772 million in gains on the sales included in Other

Noninterest Income. Additionally, during the same periods, we

received paydowns of $44.4 billion and $62.8 billion, respectively.

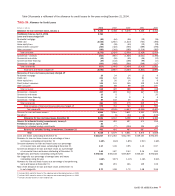

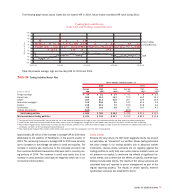

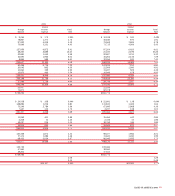

Interest Rate and Foreign Exchange Derivative Contracts

Interest rate and foreign exchange derivative contracts are utilized in

our ALM process and serve as an efficient, low-cost tool to mitigate

our risk. We use derivatives to hedge or offset the changes in cash

flows or market values of our Balance Sheet. See Note 4 of the

Consolidated Financial Statements for additional information on our

hedging activities.

Our interest rate contracts are generally nonleveraged generic

interest rate and basis swaps, options, futures, and forwards. In addi-

tion, we use foreign currency contracts to mitigate the foreign

exchange risk associated with foreign currency-denominated assets

and liabilities, as well as our equity investments in foreign sub-

sidiaries. Table

IV

, on pages 88 and 89, reflects the notional

amounts, fair value, weighted average receive fixed and pay fixed

rates, expected maturity, and estimated duration of our ALM deriva-

tives at December 31, 2004 and 2003.

Consistent with our strategy of managing interest rate sensitiv-

ity to mitigate changes in value of other financial instruments, the

notional amount of our net received fixed interest rate swap position

decreased $11.7 billion to $9.5 billion at December 31, 2004 com-

pared to December 31, 2003. The net option position increased

$238.9 billion to $323.8 billion at December 31, 2004 compared to

December 31, 2003 to offset interest rate risk in other portfolios.

The changes in our swap and option positions were part of our interest

sensitivity management.

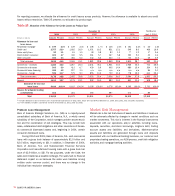

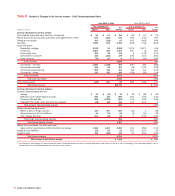

Mortgage Banking Risk Management

We manage changes in the value of MSRs by entering into derivative

financial instruments and by purchasing and selling securities. MSRs

are assets created when the underlying mortgage loan is sold to

investors and we retain the right to service the loan. As of December

31, 2004, the MSR balance was $2.5 billion, or 10 percent lower

than December 31, 2003.

We designate certain derivatives such as purchased options

and interest rate swaps as fair value hedges of specified MSRs under

SFAS 133. At December 31, 2004, the amount of MSRs identified as

being hedged by derivatives in accordance with SFAS 133 was

approximately $1.8 billion. The notional amount of the derivative con-

tracts designated as SFAS 133 hedges of MSRs at December 31,

2004 was $18.5 billion. The changes in the fair values of the deriv-

ative contracts are substantially offset by changes in the fair values

of the MSRs that are hedged by these derivative contracts. During

2004, derivative hedge gains of $228 million were offset by a

decrease in the value of the MSRs of $210 million resulting in $18

million of hedge ineffectiveness.

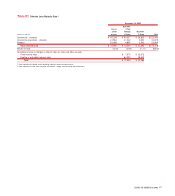

From time to time, we hold additional derivatives and certain

securities (i.e. mortgage-backed securities) as economic hedges of

MSRs, which are not designated as SFAS 133 accounting hedges.

During 2004, Gains on Sales of Debt Securities of $117 million and

$65 million of Interest Income from Securities used as an economic

hedge of MSRs were realized. At December 31, 2004, the amount of

MSRs covered by such economic hedges was $564 million. The car-

rying value of AFS securities held as economic hedges of MSRs was

$1.9 billion at December 31, 2004. The related net-of-tax unrealized

gain on these AFS securities, which is recorded in Accumulated OCI,

was $13 million at December 31, 2004.

See Notes 1 and 8 of the Consolidated Financial Statements for

additional information.