Bank of America 2004 Annual Report Download - page 136

Download and view the complete annual report

Please find page 136 of the 2004 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

|

|

BANK OF AMERICA 2004 135

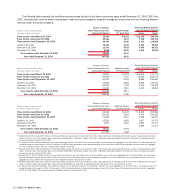

The regulatory capital guidelines measure capital in relation to

the credit and market risks of both on- and off-balance sheet items

using various risk weights. Under the regulatory capital guidelines,

Total Capital consists of three tiers of capital. Tier 1 Capital includes

Common Shareholders’ Equity, Trust Securities, minority interests

and qualifying Preferred Stock, less Goodwill and other adjustments.

Tier 2 Capital consists of Preferred Stock not qualifying as Tier 1

Capital, mandatory convertible debt, limited amounts of subordinated

debt, other qualifying term debt, the allowance for credit losses up to

1.25 percent of risk-weighted assets and other adjustments. Tier 3

Capital includes subordinated debt that is unsecured, fully paid, has

an original maturity of at least two years, is not redeemable before

maturity without prior approval by the FRB and includes a lock-in

clause precluding payment of either interest or principal if the pay-

ment would cause the issuing bank’s risk-based capital ratio to fall or

remain below the required minimum. Tier 3 Capital can only be used

to satisfy the Corporation’s market risk capital requirement and may

not be used to support its credit risk requirement. At December 31,

2004 and 2003, the Corporation had no subordinated debt that qual-

ified as Tier 3 Capital.

The capital treatment of Trust Securities is currently under

review by the FRB due to the issuing trust companies being decon-

solidated under FIN 46R. On May 6, 2004, the FRB proposed to allow

Trust Securities to continue to qualify as Tier 1 Capital with revised

quantitative limits that would be effective after a three-year transition

period. As a result, the Corporation will continue to report Trust

Securities in Tier 1 Capital. In addition, the FRB is proposing to revise

the qualitative standards for capital instruments included in regula-

tory capital. The proposed quantitative limits and qualitative stan-

dards are not expected to have a material impact to the Corporation’s

current Trust Securities position included in regulatory capital.

On July 28, 2004, the FRB and other regulatory agencies issued

the Final Capital Rule for Consolidated Asset-backed Commercial

Paper Program Assets (the Final Rule). The Final Rule allows compa-

nies to exclude from risk-weighted assets, the assets of consolidated

ABCP conduits when calculating Tier 1 and Total Risk-based Capital

ratios. The Final Rule also requires that liquidity commitments pro-

vided by the Corporation to ABCP conduits, whether consolidated or

not, be included in the capital calculations. The Final Rule was effec-

tive September 30, 2004. There was no material impact to Tier 1 and

Total Risk-based Capital as a result of the adoption of this rule.

To meet minimum, adequately-capitalized regulatory require-

ments, an institution must maintain a Tier 1 Capital ratio of four

percent and a Total Capital ratio of eight percent. A well-capitalized

institution must generally maintain capital ratios 200 bps higher than

the minimum guidelines. The risk-based capital rules have been

further supplemented by a leverage ratio, defined as Tier 1 Capital

divided by adjusted quarterly average Total Assets, after certain

adjustments. The leverage ratio guidelines establish a minimum of

three percent. Banking organizations must maintain a leverage capital

ratio of at least five percent to be classified as well-capitalized. As of

December 31, 2004, the Corporation was classified as well-capitalized

for regulatory purposes, the highest classification.

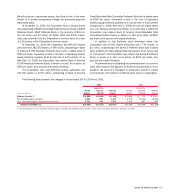

Net Unrealized Gains (Losses) on AFS Debt Securities, Net

Unrealized Gains on AFS Marketable Equity Securities and the Net

Unrealized Gains (Losses) on Derivatives included in Shareholders’

Equity at December 31, 2004 and 2003, are excluded from the cal-

culations of Tier 1 Capital and leverage ratios. The Total Capital ratio

excludes all of the above with the exception of up to 45 percent of

Net Unrealized Gains on AFS Marketable Equity Securities.

Regulatory Capital Developments

On June 26, 2004, the Basel Committee on Banking Supervision,

consisting of an international consortium of central banks and bank

supervisors, published the framework for a new set of risk-based cap-

ital standards (Basel

II

). Anticipating this event, in August 2003, the

U.S. banking regulators had already issued an advance notice of pro-

posed rulemaking to address issues in advance of publishing their

proposed rules incorporating the new Basel

II

standards. Since then,

the regulatory agencies have issued extensive supervisory guidance

on the proposed standards. A notice of proposed rule-making cover-

ing possible revisions to risk-based capital regulations relating to

the framework is expected in mid-2005; and final rules are expected

by mid-2006. The Corporation and other large internationally active

U.S. banks and bank holding companies will be expected to imple-

ment the framework’s “advanced approaches” – the advanced inter-

nal ratings-based approach for measuring credit risk and the

advanced measurement approaches for operational risk – by year-end

2007. The Corporation is in the process of finalizing its plans to

address Basel

II

.