Bank of America 2004 Annual Report Download - page 107

Download and view the complete annual report

Please find page 107 of the 2004 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

|

|

ing scale. These risk classifications, in conjunction with an analysis

of historical loss experience, current economic conditions, perform-

ance trends within specific portfolio segments and any other perti-

nent information, result in the estimation of the reserve for unfunded

lending commitments.

The allowance for credit losses related to the loan and lease

portfolio, and the reserve for unfunded lending commitments are

reported on the Consolidated Balance Sheet in the Allowance for

Loan and Lease Losses, and Accrued Expenses and Other Liabilities,

respectively. Provision for Credit Losses related to the loans and

leases portfolio, and unfunded lending commitments are both

reported in the Consolidated Statement of Income in the Provision for

Credit Losses.

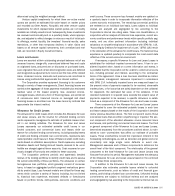

Nonperforming Loans and Leases

Credit card loans are charged off at 180 days past due or 60 days

from notification of bankruptcy filing and are not classified as non-

performing. Unsecured consumer loans and deficiencies in non-real

estate secured loans and leases are charged off at 120 days past

due and not classified as nonperforming. Real estate secured con-

sumer loans are placed on nonaccrual status and classified as non-

performing at 90 days past due. The amount deemed uncollectible on

real estate secured loans is charged off at 180 days past due.

Consumer loans are generally returned to performing status when

principal or interest is less than 90 days past due.

Commercial loans and leases that are past due 90 days or more

as to principal or interest, or where reasonable doubt exists as to

timely collection, including loans that are individually identified as

being impaired, are generally classified as nonperforming unless well-

secured and in the process of collection. Loans whose contractual

terms have been restructured in a manner which grants a concession

to a borrower experiencing financial difficulties, without compensa-

tion on restructured loans, are classified as nonperforming until the

loan is performing for an adequate period of time under the restruc-

tured agreement. In situations where the Corporation does not

receive adequate compensation, the restructuring is considered a

troubled debt restructuring. Interest accrued but not collected is

reversed when a commercial loan is classified as nonperforming.

Interest collections on commercial nonperforming loans and leases

for which the ultimate collectibility of principal is uncertain are

applied as principal reductions; otherwise, such collections are cred-

ited to income when received. Commercial loans and leases may be

restored to performing status when all principal and interest is cur-

rent and full repayment of the remaining contractual principal and

interest is expected, or when the loan otherwise becomes well-

secured and is in the process of collection.

Loans Held-for-Sale

Loans held-for-sale include residential mortgages, loan syndications,

and to a lesser degree, commercial real estate, consumer finance

and other loans, and are carried at the lower of aggregate cost or

market value. Loans held-for-sale are included in Other Assets.

Premises and Equipment

Premises and Equipment are stated at cost less accumulated depre-

ciation and amortization. Depreciation and amortization are recog-

nized using the straight-line method over the estimated useful lives

of the assets. Estimated lives range up to 40 years for buildings, up

to 12 years for furniture and equipment, and the shorter of lease

term or estimated useful life for leasehold improvements.

Mortgage Servicing Rights

Pursuant to agreements between the Corporation and its counterpar-

ties, $2.2 billion of Excess Spread Certificates (the Certificates) were

converted into Mortgage Servicing Rights (MSRs) on June 1, 2004.

Prior to the conversion of the Certificates into MSRs, the Certificates

were accounted for on a mark-to-market basis (i.e. fair value) and

changes in the value were recognized as Trading Account Profits. On

the date of the conversion, the Corporation recorded these MSRs at

the Certificates’ fair market value, and that value became their new

cost basis. Subsequent to the conversion, the Corporation accounts

for the MSRs at the lower of cost or market with impairment recog-

nized as a reduction of Mortgage Banking Income. Except for Note 8

of the Consolidated Financial Statements, what are now referred to

as MSRs include the Certificates for periods prior to the conversion.

During the second quarter of 2004, the Corporation entered

into discussions with the Securities and Exchange Commission Staff

(the Staff) regarding the accounting treatment for the Certificates and

MSRs. The Corporation has concluded its discussions with the Staff

regarding the prior accounting for the Certificates. Following discus-

sions with the Staff, the conclusion was reached that the Certificates

lacked sufficient separation from the MSRs to be accounted for as

described above (i.e. fair value). Accordingly, the Corporation should

have continued to account for the Certificates as MSRs (i.e. lower

of cost or market). The effect on our previously filed Consolidated

Financial Statements of following lower of cost or market accounting

for the Certificates compared to fair value accounting (i.e. the prior

accounting) is not material. Consequently, no revisions were made to

previously filed Consolidated Financial Statements.

When applying SFAS 133 hedge accounting for derivative finan-

cial instruments that have been designated to hedge MSRs, loans

underlying the MSRs being hedged are stratified into pools that pos-

sess similar interest rate and prepayment risk exposures. The

Corporation has designated the hedged risk as the change in the

overall fair value of these stratified pools within a daily hedge period.

The Corporation performs both prospective and retrospective hedge

effectiveness evaluations, using regression analyses. A prospective

test is performed to determine whether the hedge is expected to be

highly effective at the inception of the hedge. A retrospective test is

performed at the end of the hedge period to determine whether the

hedge was actually effective during the hedge period.

Other derivatives are used as economic hedges of the MSRs,

but are not designated as hedges under SFAS 133. These derivatives

are marked to market and recognized through Mortgage Banking

Income. Securities are also used as economic hedges of MSRs, but

106 BANK OF AMERICA 2004