Bank of America 2004 Annual Report Download - page 54

Download and view the complete annual report

Please find page 54 of the 2004 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

|

|

BANK OF AMERICA 2004 53

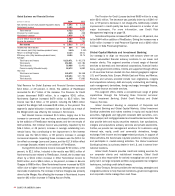

We develop and maintain contingency funding plans for both the

parent company and bank liquidity positions. These plans evaluate our

liquidity position under various operating circumstances and allow us

to ensure that we would be able to operate through a period of stress

when access to normal sources of funding is constrained. The plans

project funding requirements during a potential period of stress, specify

and quantify sources of liquidity, outline actions and procedures for

effectively managing through the problem period, and define roles and

responsibilities. They are reviewed and approved annually by ALCO.

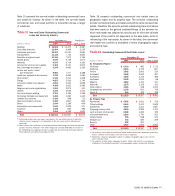

Our borrowing costs and ability to raise funds are directly

impacted by our credit ratings. The credit ratings of Bank of America

Corporation and Bank of America, National Association (Bank of

America, N.A.) and Fleet National Bank are reflected in the table below.

On February 1, 2005, Standard & Poor’s raised its credit ratings on

Bank of America Corporation and its subsidiaries to AA- on senior

debt, A+ on subordinated debt and A-1+ on commercial paper; Bank

of America, N.A. to AA on long-term debt; and Fleet National Bank to

AA on long-term debt.

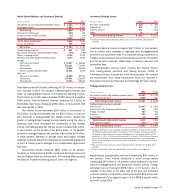

Under normal business conditions, primary sources of funding

for the parent company include dividends received from its banking

and nonbanking subsidiaries, and proceeds from the issuance of sen-

ior and subordinated debt, as well as commercial paper and equity.

Primary uses of funds for the parent company include repayment of

maturing debt and commercial paper, share repurchases, dividends

paid to shareholders, and subsidiary funding through capital or debt.

The parent company maintains a cushion of excess liquidity that

would be sufficient to fully fund holding company and nonbank affiliate

operations for an extended period during which funding from normal

sources is disrupted. The primary measure used to assess the parent

company’s liquidity is the “Time to Required Funding” during such a

period of liquidity disruption. This measure assumes that the parent

company is unable to generate funds from debt or equity issuance,

receives no dividend income from subsidiaries, and no longer pays div-

idends to shareholders while continuing to meet nondiscretionary

uses needed to maintain bank operations and repayment of contrac-

tual principal and interest payments owed by the parent company and

affiliated companies. Under this scenario, the amount of time the par-

ent company and its nonbank subsidiaries can operate and meet all

obligations before the current liquid assets are exhausted is consid-

ered the “Time to Required Funding”. ALCO approves the target range

set for this metric, in months, and monitors adherence to the target.

Maintaining excess parent company cash that ensures that “Time to

Required Funding” remains in the target range is the primary driver of

the timing and amount of the Corporation’s debt issuances. As of

December 31, 2004 “Time to Required Funding” was 29 months.

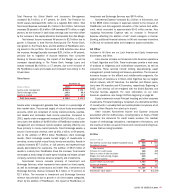

Primary sources of funding for the banking subsidiaries include

customer deposits, wholesale market-based funding, and asset secu-

ritizations. Primary uses of funds for the banking subsidiaries include

repayment of maturing obligations, and growth in the ALM and core

asset portfolios, including loan demand.

ALCO determines prudent parameters for wholesale market-based

borrowing and regularly reviews the funding plan for the bank sub-

sidiaries to ensure compliance with these parameters. The contingency

funding plan for the banking subsidiaries evaluates liquidity over a

12-month period in a variety of business environment scenarios

assuming different levels of earnings performance and credit ratings

as well as public and investor relations factors. Funding exposure

related to our role as liquidity provider to certain off-balance sheet

financing entities is also measured under a stress scenario. In this

analysis, ratings are downgraded such that the off-balance sheet

financing entities are not able to issue commercial paper and backup

facilities that we provide are drawn upon. In addition, potential draws

on credit facilities to issuers with ratings below a certain level are

analyzed to assess potential funding exposure.

One ratio used to monitor the stability of our funding composition is

the “loan to domestic deposit” (LTD) ratio. This ratio reflects the percent

of Loans and Leases that are funded by domestic customer deposits, a

relatively stable funding source. A ratio below 100 percent indicates that

our loan portfolio is completely funded by domestic customer deposits.

The ratio was 93 percent for 2004 compared to 98 percent for 2003.

For further discussion, see Deposits and Other Funding Sources on

page 54.

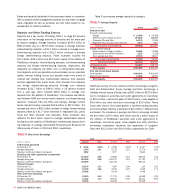

We originate loans both for retention on our Balance Sheet and

for distribution. As part of our “originate to distribute” strategy,

commercial loan originations are distributed through syndication

structures, and residential mortgages originated by Consumer Real

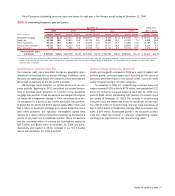

Table 4

Credit Ratings

December 31, 2004

Bank of America Corporation Bank of America, N.A. Fleet National Bank

Senior Subordinated Commercial Short-term Long-term Short-term Long-term

Debt Debt Paper Borrowings Debt Borrowings Debt

Moody’s Aa2 Aa3 P-1 P-1 Aa1 P-1 Aa1

Standard & Poor’s A+ A A-1 A-1+ AA- A-1+ AA-

Fitch, Inc. AA- A+ F1+ F1+ AA- F1+ AA-