Bank of America 2004 Annual Report Download - page 59

Download and view the complete annual report

Please find page 59 of the 2004 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

|

|

58 BANK OF AMERICA 2004

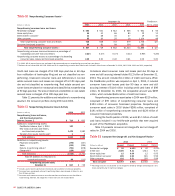

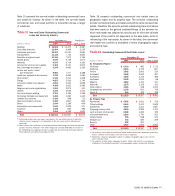

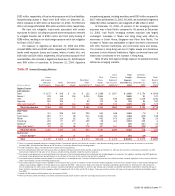

Capital Management

The final component of liquidity risk is capital management, which

focuses on the level of Shareholders’ Equity. Shareholders’ Equity

was $99.6 billion at December 31, 2004, an increase of $51.7 billion

from December 31, 2003. This increase was driven by stock issued

for the acquisition of FleetBoston of $46.8 billion, Net Income of

$14.1 billion and Common Stock Issued Under Employee Plans and

Related Tax Benefits of $3.9 billion, offset by dividends paid of $6.5

billion and common share repurchases of $6.3 billion. For additional

information on common share repurchases, see Note 13 of the

Consolidated Financial Statements. We will continue to repurchase

shares, from time to time, in the open market or in private transac-

tions through our previously approved repurchase plans.

During the second quarter of 2004, the Board approved a 2-for-1

stock split in the form of a common stock dividend and increased the

quarterly cash dividend 12.5 percent from $0.40 to $0.45 per post-

split share. The common stock dividend was effective August 27,

2004 to common shareholders of record on August 6, 2004 and the

cash dividend was effective September 24, 2004 to common share-

holders of record on September 3, 2004. All prior period common

share and related per common share information has been restated

to reflect the 2-for-1 stock split.

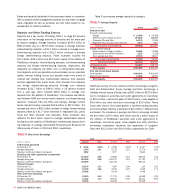

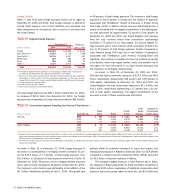

As part of the SVA calculation, equity is allocated to business

units based on an assessment of risk. The allocated amount of capital

varies according to the risk characteristics of the individual business

segments and the products they offer. Capital is allocated separately

based on the following types of risk: credit, market and operational.

Average common equity allocated to business units was $69.3 billion

and $31.4 billion in 2004 and 2003, respectively. The increase in aver-

age allocated common equity was primarily due to the Merger. Average

unallocated common equity (not allocated to business units) was

$14.7 billion and $17.7 billion in 2004 and 2003, respectively.

As a regulated financial services company, we are governed by

certain regulatory capital requirements. The regulatory Tier 1 Capital

ratio was 8.10 percent at December 31, 2004, an increase of 25 bps

from a year ago, reflecting higher Tier 1 Capital partially offset by

higher risk-weighted assets. The minimum Tier 1 Capital ratio

required is four percent. As of December 31, 2004, we were classified

as “well-capitalized” for regulatory purposes, the highest classifica-

tion. For additional information on the regulatory capital ratios along

with a description of the components of risk-based capital, capital

adequacy requirements and prompt corrective action provisions, see

Note 14 of the Consolidated Financial Statements.

The capital treatment of trust preferred securities (Trust

Securities) is currently under review by the FRB due to the issuing

trust companies being deconsolidated under FIN 46R. On May 6,

2004, the FRB proposed to allow Trust Securities to continue to qualify

as Tier 1 Capital with revised quantitative limits that would be effective

after a three-year transition period. As a result, we will continue to

report Trust Securities in Tier 1 Capital. In addition, the FRB is

proposing to revise the qualitative standards for capital instruments

included in regulatory capital. The proposed quantitative limits and

qualitative standards are not expected to have a material impact to

our current Trust Securities position included in regulatory capital.

On July 28, 2004, the FRB and other regulatory agencies issued

the Final Capital Rule for Consolidated Asset-backed Commercial

Paper Program Assets (the Final Rule). The Final Rule allows compa-

nies to exclude from risk-weighted assets, the assets of consolidated

ABCP conduits when calculating Tier 1 and Total Risk-based Capital

ratios. The Final Rule also requires that liquidity commitments pro-

vided by the Corporation to ABCP conduits, whether consolidated or

not, be included in the capital calculations. The Final Rule was effec-

tive September 30, 2004. There was no material impact to Tier 1 and

Risk-based Capital as a result of the adoption of this rule.

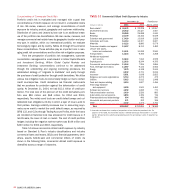

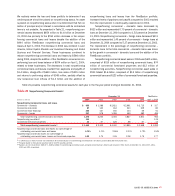

Credit Risk Management

Credit risk is the risk of loss arising from a borrower’s or counterparty’s

inability to meet its obligations. Credit risk exists in our outstanding

loans and leases, derivatives, trading account assets and unfunded

lending commitments that include loan commitments, letters of

credit and financial guarantees. We define the credit exposure to

a borrower or counterparty as the loss potential arising from all prod-

uct classifications, including loans and leases, standby letters of

credit and financial guarantees, derivative and trading account

assets, assets held-for-sale and commercial letters of credit. For deriv-

ative positions, we use the current mark-to-market value to represent

credit exposure without giving consideration to future mark-to-market

changes. Our consumer and commercial credit extension and review

procedures take into account credit exposures that are both funded

and unfunded. For additional information on derivatives and credit

extension commitments, see Notes 4 and 12 of the Consolidated

Financial Statements.

We manage credit risk based on the risk profile of the borrower

or counterparty, repayment sources, the nature of underlying collateral,

and other support given current events and conditions. We classify

our Loans and Leases as either consumer or commercial and moni-

tor their credit risk separately as discussed below.

Consumer Portfolio Credit Risk Management

Credit risk management for the consumer portfolio begins with initial

underwriting and continues throughout a borrower’s credit cycle.

Statistical techniques are used to establish product pricing, risk

appetite, operating processes and metrics to balance risks and

rewards. Consumer exposure is grouped by product and other attrib-

utes for purposes of evaluating credit risk. Statistical models are

built using detailed behavioral information from external sources

such as credit bureaus as well as internal historical experience.

These models are essential to our consumer credit risk management

process and are used, where applicable, in the determination of

credit decisions, collections management procedures, portfolio man-

agement decisions, determination of the allowance for consumer

loan and lease losses, and economic capital allocation for credit risk.