Bank of America 2004 Annual Report Download - page 145

Download and view the complete annual report

Please find page 145 of the 2004 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154

|

|

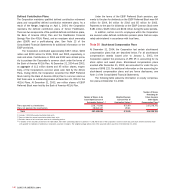

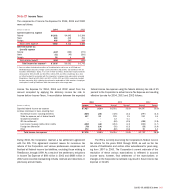

Significant components of the Corporation’s net deferred tax

liability at December 31, 2004 and 2003 are presented in the

following table.

December 31

(Dollars in millions) 2004 2003

Deferred tax liabilities

Equipment lease financing $ 6,192 $5,321

Investments 1,088 905

Intangibles 803 955

Deferred gains and losses 251 189

State income taxes 192 281

Fixed assets 47 246

Employee compensation and

retirement benefits 13 17

Other 435 560

Gross deferred tax liabilities 9,021 8,474

Deferred tax assets

Allowance for credit losses 3,668 2,421

Security valuations 2,326 1,876

Accrued expenses 533 421

Foreign tax credit carryforward 467 –

Available-for-sale securities 146 46

Loan fees and expenses 241 85

Net operating loss carryforwards 91 129

Other 1,150 280

Gross deferred tax assets 8,622 5,258

Valuation allowance(1) (155) (120)

Total deferred tax assets,

net of valuation allowance 8,467 5,138

Net deferred tax liabilities(2) $ 554 $3,336

(1) At December 31, 2004, $70 of the valuation allowance related to gross deferred tax assets

was attributable to the Merger. Future recognition of the tax attributes associated with these

gross deferred tax assets would result in tax benefits being allocated to reduce Goodwill.

(2) The Corporation’s net deferred tax liability was adjusted on April 1, 2004, to include a net

deferred tax asset of $2.0 billion attributable to the Merger.

The valuation allowance recorded by the Corporation at December 31,

2004 and 2003 represents net operating loss carryforwards gener-

ated by foreign subsidiaries and certain state deferred tax assets,

where, in each case, it is more likely than not that realization will not

occur. These net operating loss carryforwards begin to expire after

2005 and could fully expire after 2010.

The foreign tax credit carryforward reflected in the table above

represents foreign income taxes paid that are creditable against

future U.S. income taxes. If not used, these credits begin to expire

after 2009 and could fully expire after 2014.

At December 31, 2004 and 2003, federal income taxes had not

been provided on $1.1 billion and $871 million, respectively, of undis-

tributed earnings of foreign subsidiaries, earned prior to 1987 and

after 1997 that have been reinvested for an indefinite period of time.

If the earnings were distributed, an additional $221 million and $185

million of tax expense, net of credits for foreign taxes paid on such

earnings and for the related foreign withholding taxes, would result in

2004 and 2003, respectively.

On December 21, 2004, the FASB issued FSP No. 109-2 that

provides accounting and disclosure guidance for the foreign earn-

ings repatriation provision within the Act. For additional information

on FSP No. 109-2 and the Act, see Note 1 of the Consolidated

Financial Statements.

Note 18

Fair Value of Financial Instruments

SFAS No. 107, “Disclosures About Fair Value of Financial

Instruments” (SFAS 107), requires the disclosure of the estimated

fair value of financial instruments. The fair value of a financial instru-

ment is the amount at which the instrument could be exchanged in a

current transaction between willing parties, other than in a forced or

liquidation sale. Quoted market prices, if available, are utilized as

estimates of the fair values of financial instruments. Since no quoted

market prices exist for certain of the Corporation’s financial instru-

ments, the fair values of such instruments have been derived based

on management’s assumptions, the estimated amount and timing of

future cash flows and estimated discount rates. The estimation meth-

ods for individual classifications of financial instruments are

described more fully below. Different assumptions could significantly

affect these estimates. Accordingly, the net realizable values could

be materially different from the estimates presented below. In addi-

tion, the estimates are only indicative of the value of individual finan-

cial instruments and should not be considered an indication of the

fair value of the combined Corporation.

The provisions of SFAS 107 do not require the disclosure of the

fair value of lease financing arrangements and nonfinancial instru-

ments, including intangible assets such as goodwill, franchise, and

credit card and trust relationships.

Short-term Financial Instruments

The carrying value of short-term financial instruments, including cash

and cash equivalents, time deposits placed, federal funds sold and

purchased, resale and repurchase agreements, commercial paper

and other short-term investments and borrowings, approximates the

fair value of these instruments. These financial instruments generally

expose the Corporation to limited credit risk and have no stated

maturities or have short-term maturities and carry interest rates that

approximate market.

Financial Instruments Traded in the Secondary Market

Held-to-maturity securities, AFS debt and marketable equity securities,

trading account instruments and long-term debt traded actively in the

secondary market have been valued using quoted market prices. The

fair values of trading account instruments and securities are reported

in Notes 3 and 5 of the Consolidated Financial Statements.

Derivative Financial Instruments

All derivatives are recognized on the Consolidated Balance Sheet at

fair value, net of cash collateral held and taking into consideration

the effects of legally enforceable master netting agreements that

allow the Corporation to settle positive and negative positions with

144 BANK OF AMERICA 2004