Bank of America 2004 Annual Report Download - page 35

Download and view the complete annual report

Please find page 35 of the 2004 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

25 -

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

|

|

Economic Overview

In 2004, U.S. economic performance was solid, creating a generally

healthy environment for banking, while global growth exceeded

expectations. In the U.S., real Gross Domestic Product (GDP) grew

rapidly, as the negative impact of higher oil prices was more than offset

by sound fundamentals and the FRB's accommodative monetary pol-

icy. Consumer spending continued to rise, while consumer credit qual-

ity remained healthy. Sustained gains in productivity contributed to

rising corporate profits and cash flows. Businesses rebuilt invento-

ries and increased capital spending, particularly for information pro-

cessing equipment and software. Although overall corporate loan

demand remained soft, corporate credit quality improved as the econ-

omy strengthened in the second half of the year. Employment grew

and the unemployment rate receded, although the pace of job cre-

ation was soft relative to GDP growth, reflecting business efforts to

constrain operating costs. Housing activity rose to historic levels.

Inflation rose modestly but stayed low relative to historic standards.

The FRB raised the federal funds rate target from one percent at mid-

year to 2.25 percent, but the increases were widely anticipated and

bond yields remained low, generating a flatter yield curve.

Performance Overview

For the second year in a row, we achieved record earnings. Net

Income totaled $14.1 billion, or $3.69 per diluted common share in

2004, 31 percent and three percent increases, respectively, from

$10.8 billion, or $3.57 per diluted common share in 2003.

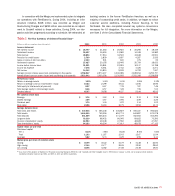

Business Segment Total Revenue and Net Income

Total Revenue Net Income

(Dollars in millions) 2004 2003 2004 2003

Global Consumer and

Small Business Banking $ 26,857 $20,930 $ 6,548 $ 5,706

Global Business and

Financial Services 6,722 4,517 2,833 1,471

Global Capital Markets

and Investment Banking 9,049 8,334 1,950 1,794

Global Wealth and

Investment Management 5,918 4,030 1,584 1,234

All Other 1,064 746 1,228 605

Total FTE basis(1) 49,610 38,557 14,143 10,810

FTE adjustment(1) (716) (643) ––

Total $ 48,894 $37,914 $ 14,143 $ 10,810

(1) Total revenue for the segments and All Other is on a fully taxable-equivalent (FTE) basis. For more

information on a FTE basis, see Supplemental Financial Data beginning on page 38.

Global Consumer and Small Business Banking

Net Income increased $842 million, or 15 percent, to $6.5 billion in

2004, including the $1.1 billion impact of the Merger. Driving this

increase was the $5.2 billion increase in Net Interest Income and a

$1.5 billion increase in Card Income. Partially offsetting this was the

$3.0 billion increase in Noninterest Expense, a $1.7 billion increase

in Provision for Credit Losses and a $1.5 billion decrease in

Mortgage Banking Income. The Provision for Credit Losses increased

$1.7 billion to $3.3 billion, including higher credit card net charge-offs

of $791 million, of which $320 million was attributed to the addition

of the FleetBoston credit card portfolio. For more information on

Global Consumer and Small Business Banking, see page 41.

Global Business and Financial Services

Net Income increased $1.4 billion, or 93 percent, to $2.8 billion for

2004 including the $824 million impact of the addition of FleetBoston.

Both average Loans and Leases, and Deposits grew significantly, with

increases of $36.3 billion, or 39 percent, and $21.6 billion, or 69 percent,

respectively. Impacting these increases were the $29.3 billion

increase in average Loans and Leases and the $17.6 billion increase

in average Deposits related to the addition of FleetBoston. Also driv-

ing the improved results was the $699 million decrease in Provision

for Credit Losses, driven by lower net charge-offs and the continued

credit quality improvement in the commercial portfolio. For more infor-

mation on Global Business and Financial Services, see page 45.

Global Capital Markets and Investment Banking

Net Income increased $156 million, or nine percent, to $2.0 billion in

2004. Contributing to the increase in Net Income was a reduction of

$762 million in the Provision for Credit Losses and increases in

Trading Account Profits and Investment Banking Income of $441 mil-

lion and $147 million, respectively. Notable improvements in credit

quality in the large corporate portfolio and a 71 percent reduction in

net charge-offs drove the $762 million decrease in Provision for

Credit Losses. Partially offsetting these increases were the $460 mil-

lion impact of charges taken for litigation matters in 2004, an

increase of $279 million of incentive compensation for market-based

activities and the $143 million impact of the charges taken for the

mutual fund matter. For more information on Global Capital Markets

and Investment Banking, see page 46.

Global Wealth and Investment Management

Net Income increased $350 million, or 28 percent, to $1.6 billion in

2004. The increase in Net Income was driven by the $253 million

impact of the addition of FleetBoston and growth in both average Loans

and Leases, and Deposits. Total assets under management increased

$154.8 billion, or 52 percent, to $451.5 billion at December 31, 2004,

due to the addition of $148.9 billion of FleetBoston assets under

management and increased market valuation partially offset by

outflows, primarily in money market products. For more information

on Global Wealth and Investment Management, see page 48.

34 BANK OF AMERICA 2004