Bank of America 2004 Annual Report Download - page 43

Download and view the complete annual report

Please find page 43 of the 2004 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

|

|

42 BANK OF AMERICA 2004

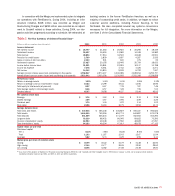

Our extensive network of delivery channels including banking

centers, ATMs, telephone channel and online banking enable us to

provide cost effective, convenient and innovative products to our

customers. Active online banking subscribers increased 73 percent

in 2004. Approximately half of this growth was due to the addition

of FleetBoston.

Net Interest Income increased $5.2 billion largely due to the net

effect of the growth in consumer loan and lease, and deposit bal-

ances, and ALM activities. Net Interest Income was positively

impacted by the $44.6 billion, or 48 percent, increase in average

Loans and Leases. This increase was driven by a $15.2 billion, or 54

percent, increase in average on-balance sheet consumer credit card

outstandings, a $14.8 billion, or 83 percent, increase in home equity

lines and a $6.8 billion, or 26 percent, increase in residential mort-

gages. The FleetBoston portfolio accounted for $5.0 billion, $14.0

billion and $10.8 billion of the increases, respectively.

Deposit growth positively impacted Net Interest Income. Higher

consumer deposit balances from the addition of FleetBoston cus-

tomers of $63.1 billion, government tax cuts, higher customer retention

and our focus on adding new customers drove the $74.3 billion, or

31 percent, increase in average Deposits.

Noninterest Income increased $733 million, or eight percent, to

$9.5 billion in 2004. FleetBoston contributed $1.4 billion to

Noninterest Income. Overall, this increase was primarily due to a

$1.5 billion, or 49 percent, increase in Card Income to $4.5 billion

and a $913 million, or 25 percent, increase in Service Charges to

$4.5 billion. Card Income increased mainly due to increases in pur-

chase volumes for both credit and debit cards, and increases in aver-

age managed credit card outstandings. These increases were due to

both the growth of our card businesses, and the addition of the

FleetBoston portfolio. The increase in Service Charges was due pri-

marily to the addition of FleetBoston customers and the growth in

new accounts. Partially offsetting these increases was a $1.5 billion,

or 72 percent, decrease in Mortgage Banking Income to $595 million

and a $186 million decrease in Trading Account Profits to a loss of

$359 million. The decrease in Mortgage Banking Income was due to

decreases in production volume and secondary market sales, com-

bined with the MSR impairments recorded during the second half of the

year. The decrease in Trading Account Profits was due to the negative

impact of faster prepayment speeds and changes in other assumptions

on the value of the Excess Spread Certificates (Certificates) prior

to their conversion to MSRs. For more information on the conversion

of the Certificates into MSRs, see Note 1 of the Consolidated

Financial Statements.

The Provision for Credit Losses increased $1.7 billion to

$3.3 billion, including higher credit card net charge-offs of $791 million,

of which $320 million was attributed to the addition of the

FleetBoston credit card portfolio. Organic growth, overall seasoning of

credit card accounts, the return of securitized loans to the balance

sheet, and increases in minimum payment requirements drove higher

net charge-offs and Provision for Credit Losses. The increase in min-

imum payment requirements is the result of changes in industry prac-

tices and will result in increased charge-offs in 2005. For more

information, see Credit Risk Management beginning on page 58.

Noninterest Expense increased $3.0 billion, or 29 percent.

Driving this increase were increases in Processing Costs of $977 million,

Personnel Expense of $763 million and Other General Operating

Expense of $512 million. Personnel Expense increased as a result of

higher salaries of $537 million and higher benefit costs of $185 million.

The impact of the addition of FleetBoston to Noninterest Expense

was $1.9 billion, including $538 million of Personnel Expense and

$443 million of Data Processing Costs.

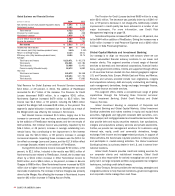

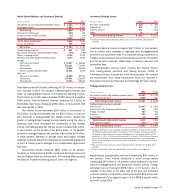

Across the three major businesses within Global Consumer and

Small Business Banking, our most significant product lines are Card

Services, Consumer Real Estate and Consumer Deposit Products.

Card Services

Card Services provides a broad offering of credit cards to an array of

customers including consumers and small businesses. Our products

include traditional credit cards, a variety of co-branded and affinity

card products, as well as purchasing, and travel and entertainment

card products. We also provide processing services for merchant

card receipts, a business where we are a market leader, due in part

to our acquisition of NPC during the fourth quarter of 2004.

We evaluate our Card Services business on both a held and

managed basis. Managed card revenue excludes the impact of card

securitization activity, which is used as a financing tool. On a held

basis, for assets that have been securitized, we record Noninterest

Income, rather than Net Interest Income and Provision for Credit

Losses, as we are compensated for servicing income and gains or

losses on securitizations. Managed card revenue excludes the impact

of the securitized credit card portfolio of $134 million and $7 million

for 2004 and 2003, respectively. These amounts are the result of the

differences in internal and external funding costs as well as the amor-

tization of previously recognized securitization gains. After the revolv-

ing period of the securitizations, the card receivables will return to our

Balance Sheet. This has the effect of increasing Loans and Leases on

our Balance Sheet and increasing Net Interest Income and the

Provision for Credit Losses, with a reduction in Noninterest Income.