Bank of America 2004 Annual Report Download - page 55

Download and view the complete annual report

Please find page 55 of the 2004 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

|

|

54 BANK OF AMERICA 2004

Estate are frequently distributed in the secondary market. In connection

with our balance sheet management activities, we may retain mortgage

loans originated as well as purchase and sell loans based on our

assessment of market conditions.

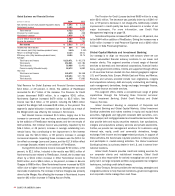

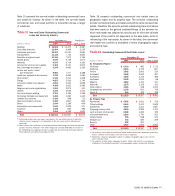

Deposits and Other Funding Sources

Deposits are a key source of funding. Table

I

on page 84 provides

information on the average amounts of deposits and the rates paid

by deposit category. Average Deposits increased $145.3 billion to

$551.6 billion due to a $97.9 billion increase in average domestic

interest-bearing deposits, a $31.1 billion increase in average nonin-

terest-bearing deposits and a $16.3 billion increase in average

foreign interest-bearing deposits. These increases included the

$71.0 billion, $25.3 billion and $5.5 billion impact of the addition of

FleetBoston domestic interest-bearing deposits, noninterest-bearing

deposits and foreign interest-bearing deposits, respectively. We

categorize our deposits into either core or market-based deposits.

Core deposits, which are generally customer-based, are an important

stable, low-cost funding source and typically react more slowly to

interest rate changes than market-based deposits. Core deposits

exclude negotiable CDs, public funds, other domestic time deposits

and foreign interest-bearing deposits. Average core deposits

increased $130.7 billion to $494.1 billion, a 36 percent increase

from a year ago, which included $95.6 billion in average core

deposits from the addition of FleetBoston. The increase was distrib-

uted between NOW and money market deposits, noninterest-bearing

deposits, consumer CDs and IRAs, and savings. Average market-

based deposit funding increased $14.6 billion to $57.5 billion. The

increase was due to a $16.3 billion increase in foreign interest-bearing

deposits offset by a $1.7 billion decrease in negotiable CDs, public

funds and other domestic time deposits. These increases also

reflected the $6.2 billion impact to average market-based deposit

funding from the addition of FleetBoston market-based deposit fund-

ing. Deposits, on average, represented 53 percent and 54 percent of

total sources of funds in 2004 and 2003, respectively.

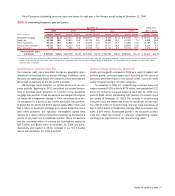

Table 5 summarizes average deposits by category.

Table 5

Average Deposits

(Dollars in millions) 2004 2003

Deposits by type

Domestic interest-bearing:

Savings $ 33,959 $ 24,538

NOW and money market accounts 214,542 148,896

Consumer CDs and IRAs 94,770 70,246

Negotiable CDs and other time deposits 5,977 7,627

Total domestic interest-bearing 349,248 251,307

Foreign interest-bearing:

Banks located in foreign countries 18,426 13,959

Governments and official institutions 5,327 2,218

Time, savings and other 27,739 19,027

Total foreign interest-bearing 51,492 35,204

Total interest-bearing 400,740 286,511

Noninterest-bearing 150,819 119,722

Total deposits $ 551,559 $ 406,233

Core and market-based deposits

Core deposits $ 494,090 $ 363,402

Market-based deposits 57,469 42,831

Total deposits $ 551,559 $ 406,233

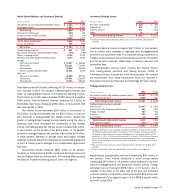

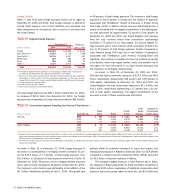

Additional sources of funds include short-term borrowings, Long-term

Debt and Shareholders’ Equity. Average short-term borrowings, a

relatively low-cost source of funds, were up $87.1 billion to $227.6 billion

due to increases in securities sold under agreements to repurchase

of $59.4 billion, commercial paper of $18.2 billion, notes payable of

$8.6 billion and other short-term borrowings of $2.9 billion. These

funds were used to fund asset growth or facilitate trading activities

and were partially offset by a decrease of $2.0 billion in federal funds

purchased. The increases in average short-term borrowings included

the $4.0 billion, $274 million, $18 million, and $1.1 billion impact of

the addition of FleetBoston securities sold under agreements to

repurchase, commercial paper, notes payable and other short-term

borrowings, respectively. Issuances and repayments of Long-term

Debt were $21.3 billion and $16.9 billion, respectively, for 2004.

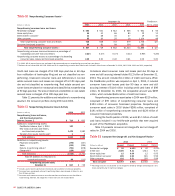

Table 6

Short–term Borrowings

2004 2003 2002

(Dollars in millions) Amount Rate Amount Rate Amount Rate

Federal funds purchased

At December 31 $ 3,108 2.32% $ 2,356 0.84% $ 5,167 1.15%

Average during year 3,724 1.31 5,736 1.10 5,470 1.63

Maximum month-end balance during year 7,852 – 7,877 – 9,663 –

Securities sold under agreements to repurchase

At December 31 116,633 2.85 75,690 1.12 59,912 1.44

Average during year 161,494 2.08 102,074 1.15 67,751 1.73

Maximum month-end balance during year 191,899 – 124,746 – 99,313 –

Commercial paper

At December 31 25,379 1.71 7,605 1.09 114 1.20

Average during year 21,178 1.45 2,976 1.29 1,025 1.73

Maximum month-end balance during year 26,486 – 9,136 – 1,946 –

Other short-term borrowings

At December 31 53,219 2.49 27,375 1.98 16,599 1.29

Average during year 41,162 1.73 29,672 2.02 24,231 2.90

Maximum month-end balance during year 53,756 – 46,635 – 33,549 –