Bank of America 2004 Annual Report Download - page 118

Download and view the complete annual report

Please find page 118 of the 2004 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

|

|

BANK OF AMERICA 2004 117

Note 8

Special Purpose Financing Entities

The Corporation securitizes assets and may retain a portion or all of

the securities, subordinated tranches, interest-only strips and, in

some cases, a cash reserve account, all of which are considered

retained interests in the securitized assets. Those assets may be

serviced by the Corporation or by third parties. The Corporation

also uses other special purpose financing entities to access the

commercial paper market and for other lending, leasing and real

estate activities. See Note 1 of the Consolidated Financial

Statements for a more detailed discussion of securitizations and

other special purpose financing entities.

Mortgage-related Securitizations

The Corporation securitizes the majority of its residential mortgage

loan originations in conjunction with or shortly after loan closing. In

addition, the Corporation may, from time to time, securitize commer-

cial mortgages and first residential mortgages that it originates or

purchases from other entities. In 2004 and 2003, the Corporation

converted a total of $96.9 billion (including $18.0 billion originated

by other entities) and $121.1 billion (including $13.0 billion originated

by other entities), respectively, of residential first mortgages and com-

mercial mortgages into mortgage-backed securities issued through

Fannie Mae, Freddie Mac, Government National Mortgage Association

(Ginnie Mae), Bank of America, N.A. and Banc of America Mortgage

Securities. At December 31, 2004 and 2003, the Corporation retained

$9.2 billion (including $1.2 billion issued prior to 2004) and $1.7 bil-

lion of securities, respectively. At December 31, 2004, these retained

interests were valued using quoted market prices.

For 2004, the Corporation reported $952 million in gains on

loans converted into securities and sold, of which $886 million was

from loans originated by the Corporation and $66 million was from

loans originated by other entities. For 2003, the Corporation reported

$2.4 billion in gains on loans converted into securities and sold, of

which $2.0 billion was from loans originated by the Corporation

and $381 million was from loans originated by other entities. At

December 31, 2004, the Corporation had recourse obligations of

$558 million with varying terms up to seven years on loans that had

been securitized and sold.

In addition to the retained interests in the securities, the

Corporation has retained MSRs from the sale or securitization of res-

idential mortgage loans. Servicing fee and ancillary fee income on all

loans serviced, including securitizations, was $568 million and $314

million in 2004 and 2003, respectively. The activity in MSRs for 2004

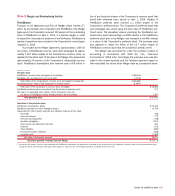

and 2003 is as follows:

(Dollars in millions) 2004 2003

Balance, January 1 $ 479 $ 499

Additions(1) 3,036 201

Amortization (360) (145)

Change in value attributed to SFAS 133 hedged MSRs(2) (210) –

Impairment, net of recoveries (463) (76)

Balance, December 31(3,4) $ 2,482 $ 479

(1) Includes $2.2 billion of Certificates converted to MSRs on June 1, 2004.

(2) Excludes $228 of offsetting derivative hedge gains recognized in Mortgage Banking Income

for 2004.

(3) Net of impairment allowance of $361 for 2004.

(4) 2003 does not include $2.3 billion of Certificates.

The estimated fair value of MSRs was $2.5 billion and $479 mil-

lion at December 31, 2004 and 2003, respectively. The additions

during 2004 included $2.2 billion of MSRs as a result of the con-

version of Certificates discussed in Note 1 of the Consolidated

Financial Statements.

The key economic assumptions used in valuations of MSRs

include modeled prepayment rates and resultant expected weighted

average lives of the MSRs and the option adjusted spread (OAS) levels.

An OAS model runs multiple interest rate scenarios and projects pre-

payments specific to each one of those interest rate scenarios.

As of December 31, 2004, the modeled weighted average lives

of MSRs related to fixed and adjustable rate loans (including hybrid

ARMs) were 4.65 years and 3.02 years, respectively. A decrease of

10 and 20 percent in modeled prepayments would extend the

expected weighted average lives for MSRs related to fixed rate loans

to 5.01 years and 5.40 years, respectively, and would extend the

expected weighted average lives for MSRs related to adjustable rate

loans to 3.32 years and 3.68 years, respectively. The expected exten-

sion of weighted average lives would increase the value of MSRs by

a range of $143 million to $295 million. An increase of 10 and 20

percent in modeled prepayments would reduce the expected

weighted average lives for MSRs related to fixed rate loans to 4.38

years and 4.11 years, respectively, and would reduce the expected

weighted average lives for MSRs related to adjustable rate loans to

2.78 years and 2.57 years, respectively. The expected reduction of

weighted average lives would decrease the value of MSRs by a range

of $112 million to $219 million. A decrease of 100 and 200 basis

points (bps) in the OAS level would result in an increase in the value

of MSRs ranging from $89 million to $185 million, and an increase

of 100 and 200 bps in the OAS level would result in a decrease in

the value of MSRs ranging from $83 million to $160 million.

For purposes of evaluating and measuring impairment, the

Corporation stratifies the portfolio based on the predominant risk

characteristics of loan type and note rate. Indicated impairment, by

risk stratification, is recognized as a reduction in Mortgage Banking

Income, through a valuation allowance, for any excess of adjusted car-

rying value over estimated fair value. Impairment, net of recoveries of

MSRs totaled $463 million for 2004. For 2003, changes in the value

of the Certificates and MSRs were recognized as Trading Account

Profits. Impairment charges in 2004 included changes to valuation

assumptions and prepayment adjustments related to expectations

regarding future prepayment speeds and other assumptions totaling

$261 million. Additional impairment reflects decreases in the value of

MSRs primarily due to increased probability of prepayments driven by

decreases in market interest rates during the second half of 2004.

Other Securitizations

As a result of the Merger, the Corporation acquired an interest in sev-

eral credit card, home equity loan and commercial loan securitization

vehicles, which had aggregate debt securities outstanding of $10.3

billion as of December 31, 2004. During 2004, the Corporation secu-

ritized $2.0 billion of automobile loans and retained $1.7 billion of

the AAA securities, which are held in the AFS securities portfolio.