Bank of America 2004 Annual Report Download - page 114

Download and view the complete annual report

Please find page 114 of the 2004 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

|

|

BANK OF AMERICA 2004 113

The average fair value of Derivative Assets for 2004 and 2003 was

$28.0 billion and $27.8 billion, respectively. The average fair value

of Derivative Liabilities for 2004 and 2003 was $15.7 billion and

$15.9 billion, respectively. Included in the average fair value of

Derivative Assets and Derivative Liabilities in 2004 was $1.5 billion

and $920 million, respectively, from the addition of derivatives

acquired from FleetBoston.

ALM Process

Interest rate contracts and foreign exchange contracts are utilized in

the Corporation’s ALM process. The Corporation maintains an overall

interest rate risk management strategy that incorporates the use of

interest rate contracts to minimize significant unplanned fluctuations

in earnings that are caused by interest rate volatility. The

Corporation’s goal is to manage interest rate sensitivity so that move-

ments in interest rates do not significantly adversely affect Net

Interest Income. As a result of interest rate fluctuations, hedged

fixed-rate assets and liabilities appreciate or depreciate in market

value. Gains or losses on the derivative instruments that are linked

to the hedged fixed-rate assets and liabilities are expected to sub-

stantially offset this unrealized appreciation or depreciation. Interest

Income and Interest Expense on hedged variable-rate assets and

liabilities, respectively, increase or decrease as a result of interest

rate fluctuations. Gains and losses on the derivative instruments that

are linked to these hedged assets and liabilities are expected to sub-

stantially offset this variability in earnings.

Interest rate contracts, which are generally non-leveraged

generic interest rate and basis swaps, options and futures, allow the

Corporation to manage its interest rate risk position. Non-leveraged

generic interest rate swaps involve the exchange of fixed-rate and

variable-rate interest payments based on the contractual underlying

notional amount. Basis swaps involve the exchange of interest pay-

ments based on the contractual underlying notional amounts, where

both the pay rate and the receive rate are floating rates based on dif-

ferent indices. Option products primarily consist of caps, floors, swap-

tions and options on index futures contracts. Futures contracts used

for the ALM process are primarily index futures providing for cash pay-

ments based upon the movements of an underlying rate index.

The Corporation uses foreign currency contracts to manage the

foreign exchange risk associated with certain foreign currency-denom-

inated assets and liabilities, as well as the Corporation’s equity

investments in foreign subsidiaries. Foreign exchange contracts,

which include spot, futures and forward contracts, represent agree-

ments to exchange the currency of one country for the currency of

another country at an agreed-upon price on an agreed-upon settle-

ment date. Foreign exchange option contracts are similar to interest

rate option contracts except that they are based on currencies rather

than interest rates. Exposure to loss on these contracts will increase

or decrease over their respective lives as currency exchange and

interest rates fluctuate.

Fair Value and Cash Flow Hedges

The Corporation uses various types of interest rate and foreign cur-

rency exchange rate derivative contracts to protect against changes

in the fair value of its fixed-rate assets and liabilities due to fluctua-

tions in interest rates and exchange rates. The Corporation also uses

these contracts to protect against changes in the cash flows of its

variable-rate assets and liabilities, and other forecasted transactions.

For cash flow hedges, gains and losses on derivative contracts

reclassified from Accumulated OCI to current period earnings are

included in the line item in the Consolidated Statement of Income in

which the hedged item is recorded and in the same period the hedged

item affects earnings. During the next 12 months, net losses on deriv-

ative instruments included in Accumulated OCI, of approximately $136

million (pre-tax) are expected to be reclassified into earnings. These

net gains reclassified into earnings are expected to increase income

or decrease expense on the respective hedged items.

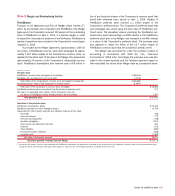

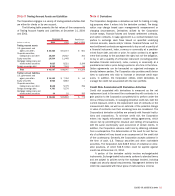

The following table summarizes certain information related to

the Corporation’s hedging activities for 2004 and 2003.

(Dollars in millions) 2004 2003

Fair value hedges

Hedge ineffectiveness recognized in earnings(1) $10 $–

Net loss excluded from assessment of effectiveness(2) (6) (101)

Cash flow hedges

Hedge ineffectiveness recognized in earnings(3) 104 53

Net gain excluded from assessment of effectiveness –26

Net investment hedges

Gains (losses) included in foreign currency

translation adjustments within accumulated

other comprehensive income (157) (194)

(1) Included $(8) recorded in Net Interest Income and $18 recorded in Mortgage Banking Income in

the Consolidated Statement of Income in 2004.

(2) Included $(5) and $(101), respectively, recorded in Net Interest Income related to the excluded

time value of certain hedges and $(1) and $0, respectively, recorded in Mortgage Banking

Income in the Consolidated Statement of Income in 2004 and 2003.

(3) Included $117 and $38, respectively, recorded in Mortgage Banking Income in the Consolidated

Statement of Income for 2004 and 2003, and $(13) and $15 recorded in Net Interest Income

from other various cash flow hedges in 2004 and 2003, respectively.