Bank of America 2004 Annual Report Download - page 74

Download and view the complete annual report

Please find page 74 of the 2004 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

|

|

BANK OF AMERICA 2004 73

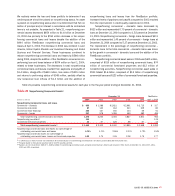

Our traditional banking loan and deposit products are nontrading

positions and are reported at amortized cost for assets or the amount

owed for liabilities (historical cost). While the accounting rules require

a historical cost view of traditional banking assets and liabilities,

these positions are still subject to changes in economic value based

on varying market conditions. Interest rate risk is the effect of

changes in the economic value of our loans and deposits, as well as

our other interest rate sensitive instruments, and is reflected in the

levels of future income and expense produced by these positions ver-

sus levels that would be generated by current levels of interest rates.

We seek to mitigate interest rate risk as part of the ALM process.

We seek to mitigate trading risk within our prescribed risk

appetite using hedging techniques. Trading positions are reported at

estimated market value with changes reflected in income. Trading

positions are subject to various risk factors, which include exposures

to interest rates and foreign exchange rates, as well as mortgage,

equity market, commodity and issuer credit risk factors. We seek to

mitigate these risk exposures by utilizing a variety of financial instru-

ments. The following discusses the key risk components along with

respective risk mitigation techniques.

Interest Rate Risk

Interest rate risk represents exposures we have to instruments

whose values vary with the level of interest rates. These instruments

include, but are not limited to, loans, debt securities, certain trading-

related assets and liabilities, deposits, borrowings and derivative

instruments. We seek to mitigate risks associated with the expo-

sures in a variety of ways that typically involve taking offsetting posi-

tions in cash or derivative markets. The cash and derivative

instruments allow us to seek to mitigate risks by reducing the effect

of movements in the level of interest rates, changes in the shape of

the yield curve as well as changes in interest rate volatility. Hedging

instruments used to mitigate these risks include related derivatives

such as options, futures, forwards and swaps.

Foreign Exchange Risk

Foreign exchange risk represents exposures we have to changes in

the values of current holdings and future cash flows denominated in

other currencies. The types of instruments exposed to this risk

include investments in foreign subsidiaries, foreign currency-denomi-

nated loans, foreign currency-denominated securities, future cash

flows in foreign currencies arising from foreign exchange transac-

tions, and various foreign exchange derivative instruments whose val-

ues fluctuate with changes in currency exchange rates or foreign

interest rates. Instruments used to mitigate this risk are foreign

exchange options, currency swaps, futures, forwards and deposits.

These instruments help insulate us against losses that may arise

due to volatile movements in foreign exchange rates or interest rates.

Mortgage Risk

Our exposure to mortgage risk takes several forms. First, we trade

and engage in market-making activities in a variety of mortgage

securities, including whole loans, pass-through certificates, commer-

cial mortgages, and collateralized mortgage obligations. Second, we

originate a variety of asset-backed securities, which involves the

accumulation of mortgage-related loans in anticipation of eventual

securitization. Third, we may hold positions in mortgage securities

and residential mortgage loans as part of the ALM portfolio. Fourth,

we create MSRs as part of our mortgage activities. See Notes 1 and

8 of the Consolidated Financial Statements for additional information

on MSRs. These activities generate market risk since these instru-

ments are sensitive to changes in the level of market interest rates,

changes in mortgage prepayments and interest rate volatility.

Options, futures, forwards, swaps, swaptions, U.S. Treasury securi-

ties and mortgage-backed securities are used to hedge mortgage risk

by seeking to mitigate the effects of changes in interest rates.

Equity Market Risk

Equity market risk arises from exposure to securities that represent an

ownership interest in a corporation in the form of common stock or other

equity-linked instruments. The instruments held that would lead to this

exposure include, but are not limited to, the following: common stock,

listed equity options (puts and calls), over-the-counter equity options,

equity total return swaps, equity index futures and convertible bonds. We

seek to mitigate the risk associated with these securities via hedging on

a portfolio or name basis that focuses on reducing volatility from

changes in stock prices. Instruments used for risk mitigation include

options, futures, swaps, convertible bonds and cash positions.

Commodity Risk

Commodity risk represents exposures we have to products traded in the

petroleum, natural gas, metals and power markets. Our principal expo-

sure to these markets emanates from customer-driven transactions.

These transactions consist primarily of futures, forwards, swaps and

options. We seek to mitigate exposure to the commodity markets with

instruments including, but not limited to, options, futures and swaps in

the same or similar commodity product, as well as cash positions.

Issuer Credit Risk

Our portfolio is exposed to issuer credit risk where the value of an

asset may be adversely impacted for various reasons directly related

to the issuer, such as management performance, financial leverage

or reduced demand for the issuer’s goods or services. Perceived

changes in the creditworthiness of a particular debtor or sector can

have significant effects on the replacement costs of both cash and

derivative positions. We seek to mitigate the impact of credit

spreads, credit migration and default risks on the market value of the

trading portfolio with the use of credit default swaps, and credit fixed

income and similar securities.