Bank of America 2004 Annual Report Download - page 47

Download and view the complete annual report

Please find page 47 of the 2004 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

|

|

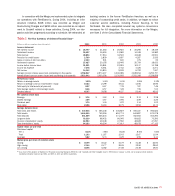

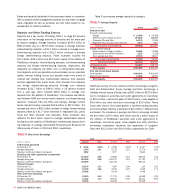

Global Business and Financial Services

(Dollars in millions) 2004 2003

Net interest income (fully taxable-equivalent basis) $ 4,593 $ 3,118

Noninterest income 2,129 1,399

Total revenue 6,722 4,517

Provision for credit losses (241) 458

Noninterest expense 2,476 1,797

Income before income taxes 4,487 2,262

Income tax expense 1,654 791

Net income $ 2,833 $ 1,471

Shareholder value added $ 884 $ 846

Net interest yield (fully taxable-equivalent basis) 3.40% 3.19%

Return on average equity 15.34 25.01

Efficiency ratio (fully taxable-equivalent basis) 36.84 39.75

Average:

Total loans and leases $ 129,671 $ 93,378

Total assets 154,521 103,786

Total deposits 53,088 31,461

Common equity/Allocated equity 18,473 5,882

Year end:

Total loans and leases 145,072 96,168

Total assets 178,093 107,791

Total deposits 61,395 37,882

Total Revenue for Global Business and Financial Services increased

$2.2 billion, or 49 percent, in 2004. The addition of FleetBoston

accounted for $1.7 billion of the increase. The Provision for Credit

Losses decreased $699 million, to a negative $241 million.

Noninterest Expense increased $679 million to $2.5 billion. Net

Income rose $1.4 billion, or 93 percent, including the $824 million

impact of the Merger. SVA increased $38 million, or four percent. This

segment’s capital allocation increased due to Goodwill as a result of

the Merger which was offset by the increase in Net Income.

Net Interest Income increased $1.5 billion, largely due to the

increase in commercial loan and lease, and deposit balances driven

by the addition of FleetBoston earning assets and the net results of

ALM activities. Net Interest Income was positively impacted by the

$36.3 billion, or 39 percent, increase in average outstanding com-

mercial loans. Also contributing to the improvement in Net Interest

Income was the $21.6 billion, or 69 percent, increase in average

commercial deposits. Impacting these increases was the $29.3 bil-

lion effect on average Loans and Leases, and the $17.6 billion effect

on average Deposits related to the addition of FleetBoston.

During 2004, Noninterest Income increased $730 million, or 52

percent, to $2.1 billion. Included in the results was $601 million of

Noninterest Income related to FleetBoston. Overall, the increase was

driven by a $341 million increase in Other Noninterest Income to

$518 million, and a $261 million, or 36 percent, increase in Service

Charges to $988 million. Other Noninterest Income increased by $109

million due to higher income from community development tax credit

real estate investments. The increase in Service Charges was primarily

driven by the Merger. Also affecting the increase in Noninterest Income

was the $43 million increase in Trading Account Profits.

The Provision for Credit Losses declined $699 million to a neg-

ative $241 million. The decrease was partially driven by a $264 mil-

lion, or 59 percent, decrease in net charge-offs. Additionally, notable

improvement in credit quality has been achieved in a number of our

major businesses. For more information, see Credit Risk

Management beginning on page 58.

Noninterest Expense increased $679 million, or 38 percent, due

to the $644 million addition of FleetBoston. Driving the increase was a

$300 million increase in total Personnel Expense and a $260 million

increase in Data Processing Expense.

Global Capital Markets and Investment Banking

Our strategy is to align our resources with sectors where we can

deliver value-added financial advisory solutions to our issuer and

investor clients. This segment provides a broad range of financial

services to domestic and international corporations, financial institu-

tions, and government entities. Clients are supported through offices

in 35 countries that are divided into four distinct geographic regions:

U.S. and Canada; Asia; Europe, Middle East and Africa; and Mexico.

Products and services provided include loan originations, mergers

and acquisitions advisory, debt and equity underwriting and trading,

cash management, derivatives, foreign exchange, leveraged finance,

structured finance and trade services.

This segment offers clients a comprehensive range of global

capabilities through the following three financial services:

Global Investment Banking, Global Credit Products and Global

Treasury Services.

Global Investment Banking is comprised of Corporate and

Investment Banking and Global Capital Markets. Global Investment

Banking underwrites and makes markets in equity and equity-linked

securities, high-grade and high-yield corporate debt securities, com-

mercial paper, and mortgage-backed and asset-backed securities. We

also provide debt and equity securities research, loan syndications,

mergers and acquisitions advisory services and private placements.

Further, we provide risk management solutions for customers using

interest rate, equity, credit and commodity derivatives, foreign

exchange, fixed income and mortgage-related products. In support of

these activities, the businesses may take positions in these products

and participate in market-making activities. The Global Investment

Banking business is a primary dealer in the U.S. and in several inter-

national locations.

Global Credit Products provides credit and lending services for

our corporate clients and institutional investors. Global Credit

Products is also responsible for actively managing loan and counter-

party risk in our large corporate portfolio using available risk mitigation

techniques, including credit default swaps.

Global Treasury Services provides the technology, strategies and

integrated solutions to help financial institutions, government agencies

and corporate clients manage their cash flows.

46 BANK OF AMERICA 2004