Bank of America 2004 Annual Report Download - page 61

Download and view the complete annual report

Please find page 61 of the 2004 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

|

|

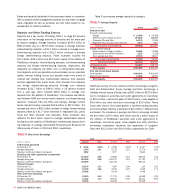

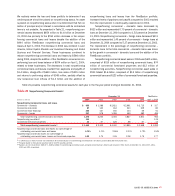

Credit card loans are charged off at 180 days past due or 60 days

from notification of bankruptcy filing and are not classified as non-

performing. Unsecured consumer loans and deficiencies in non-real

estate secured loans and leases are charged off at 120 days past

due and not classified as nonperforming. Real estate secured con-

sumer loans are placed on nonaccrual and classified as nonperforming

at 90 days past due. The amount deemed uncollectible on real estate

secured loans is charged off at 180 days past due.

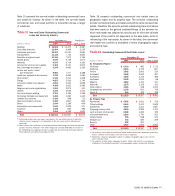

Table 11 presents the additions and reductions to nonperforming

assets in the consumer portfolio during 2004 and 2003.

Table 11

Nonperforming Consumer Assets Activity

(Dollars in millions) 2004 2003

Nonperforming loans and leases,

and foreclosed properties

Balance, January 1 $ 719 $ 832

Additions to nonperforming assets:

FleetBoston balance, April 1, 2004 127 –

New nonaccrual loans and leases,

and foreclosed properties 1,476 1,583

Transfers from assets held-for-sale(1) 15

Total additions 1,604 1,588

Reductions in nonperforming assets:

Paydowns and payoffs (376) (447)

Sales (219) (265)

Returns to performing status(2) (793) (878)

Charge-offs(3) (128) (111)

Total reductions (1,516) (1,701)

Total net additions to (reductions in)

nonperforming assets 88 (113)

Nonperforming consumer assets,

December 31 $ 807 $ 719

(1) Includes assets held-for-sale that were foreclosed and transferred to foreclosed properties.

(2) Consumer loans are generally returned to performing status when principal or interest is less

than 90 days past due.

(3) Consumer credit card and consumer non-real estate loans and leases are not classified as

nonperforming; therefore, the charge-offs on these loans are not included above.

On-balance sheet consumer loans and leases past due 90 days or

more and still accruing interest totaled $1.2 billion at December 31,

2004. This amount included $1.1 billion of credit card loans. When

the FleetBoston portfolio was acquired on April 1, 2004, it included

consumer loans and leases past due 90 days or more and still

accruing interest of $116 million including credit card loans of $98

million. At December 31, 2003, the comparable amount was $698

million, which included $616 million of credit card loans.

Nonperforming consumer asset sales in 2004 were $219 million,

comprised of $95 million of nonperforming consumer loans and

$124 million of consumer foreclosed properties. Nonperforming

consumer asset sales in 2003 totaled $265 million, comprised of

$141 million of nonperforming consumer loans and $124 million of

consumer foreclosed properties.

During the fourth quarter of 2004, we sold $1.1 billion of credit

card loans included in our held-for-sale portfolio that were acquired

as part of the FleetBoston acquisition.

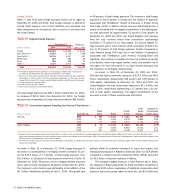

Table 12 presents consumer net charge-offs and net charge-off

ratios for 2004 and 2003.

Table 12

Consumer Net Charge-offs and Net Charge-off Ratios(1)

2004 2003

(Dollars in millions) Amount Percent Amount Percent

Residential mortgage $ 36 0.02% $ 40 0.03%

Credit card 2,305 5.31 1,514 5.37

Home equity lines 15 0.04 12 0.05

Direct/Indirect consumer 208 0.55 181 0.55

Other consumer 193 2.51 255 2.89

Total consumer $2,757 0.93% $ 2,002 0.91%

(1) Percentage amounts are calculated as net charge-offs divided by average outstanding loans and

leases during the year for each loan category.

60 BANK OF AMERICA 2004

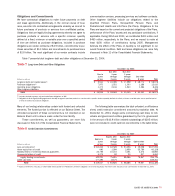

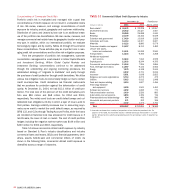

Table 10

Nonperforming Consumer Assets(1)

December 31 FleetBoston

(Dollars in millions) 2004 2003 2002 2001 2000 April 1, 2004

■■■■

Nonperforming consumer loans and leases

Residential mortgage $ 554 $ 531 $ 612 $ 556 $ 551 $ 55

Home equity lines 66 43 66 80 32 13

Direct/Indirect consumer 33 28 30 27 19 10

Other consumer 85 36 25 16 1,104 49

■■■■

Total nonperforming consumer loans and leases 738 638 733 679 1,706 127

Consumer foreclosed properties 69 81 99 334 182 –

■■■■

Total nonperforming consumer assets(2) $ 807 $ 719 $ 832 $1,013 $1,888 $ 127

■■■■

Nonperforming consumer loans and leases as a percentage of

outstanding consumer loans and leases 0.23% 0.27% 0.37% 0.41% 0.90% 0.20%

Nonperforming consumer assets as a percentage of outstanding

consumer loans, leases and foreclosed properties 0.25 0.30 0.42 0.61 1.00 0.20

■■■■

(1) In 2004, $40 in Interest Income was estimated to be contractually due on nonperforming consumer loans and leases.

(2) Balances do not include $28, $16, $41, $646 and $0 of nonperforming consumer loans held-for-sale, included in Other Assets at December 31, 2004, 2003, 2002, 2001 and 2000, respectively.