Bank of America 2004 Annual Report Download - page 53

Download and view the complete annual report

Please find page 53 of the 2004 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

|

|

52 BANK OF AMERICA 2004

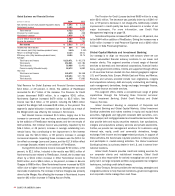

Oversight

The Board evaluates risk through the Chief Executive Officer (CEO)

and three committees. The Finance Committee, a committee

appointed by the Board, establishes policies and strategies for man-

aging the strategic, liquidity, credit, market and operational risks to

corporate earnings and capital. The Asset Quality Committee, a

Board committee, reviews credit and selected market risks; and the

Audit Committee, a Board committee, provides direct oversight of

the corporate audit function and the independent registered public

accounting firm. Additionally, senior management oversight of our

risk-taking and risk management activities is conducted through three

senior management committees: the Risk and Capital Committee

(RCC), the Asset and Liability Committee (ALCO) and the Credit Risk

Committee (CRC). The RCC, a senior management committee,

reviews corporate strategies and corporate objectives, evaluates

business performance, and reviews business plans, including capital

allocation, for the Corporation and for major businesses. The ALCO,

a subcommittee of the Finance Committee, approves limits for trad-

ing activities, and was established to manage the risk of loss of value

and related Net Interest Income of our trading positions. ALCO also

provides oversight for Corporate Treasury’s and Corporate

Investment’s process of managing interest rate risk, otherwise known

as the ALM process, and reviews hedging techniques. In addition,

ALCO provides oversight guidance over our credit hedging program.

The CRC, a subcommittee of the Finance Committee, establishes cor-

porate credit practices and limits, including industry and country con-

centration limits, approval requirements and exceptions. The CRC

also reviews business asset quality results versus plan, portfolio

management, and the adequacy of the allowance for credit losses.

Each committee and subcommittee has the ability to delegate author-

ity to officers of subcommittees to manage specific risks.

Management is in the process of finalizing its plans to address

the Basel Committee on Banking Supervision’s new risk-based capital

standards (Basel

II

). The Finance Committee and the Audit

Committee provide oversight of management’s plans including the

Corporation’s preparedness and compliance with Basel

II

. For additional

information, see Note 14 of the Consolidated Financial Statements.

In 2005, the Finance Committee chartered the Compliance and

Operational Risk Committee (CORC) as a subcommittee of the

Finance Committee. CORC provides oversight and consistent com-

munication of operational and compliance issues.

The following sections, Strategic Risk Management, Liquidity

Risk Management, Credit Risk Management beginning on page 58,

Market Risk Management beginning on page 72 and Operational

Risk Management on page 78, address in more detail the specific

procedures, measures and analyses of the major categories of risk

that we manage.

Strategic Risk Management

The Board provides oversight for strategic risk through the CEO and the

Finance Committee. We use an integrated business planning process to

help manage strategic risk. A key component of the planning process

aligns strategies, goals, tactics and resources. The process begins with

an assessment that creates a plan for the Corporation, setting the cor-

porate strategic direction. The planning process then cascades through

the business units, creating business unit plans that are aligned with the

Corporation’s direction. Tactics and metrics are monitored to ensure

adherence to the plans. As part of this monitoring, business units per-

form a quarterly self-assessment further described in the Operational

Risk Management section on page 78. This assessment looks at chang-

ing market and business conditions, and the overall risk in meeting objec-

tives. Corporate Audit in turn monitors, and independently reviews and

evaluates the plans and self-assessments.

One of the key tools for managing strategic risk is capital allo-

cation. Through allocating capital, we effectively manage each busi-

ness segment’s ability to take on risk. Review and approval of

business plans incorporates approval of capital allocation, and eco-

nomic capital usage is monitored through financial and risk reporting.

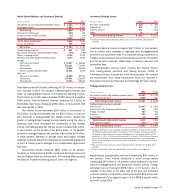

Liquidity Risk Management

Liquidity is the ongoing ability to accommodate liability maturities and

deposit withdrawals, fund asset growth and business operations, and

meet contractual obligations through unconstrained access to fund-

ing at reasonable market rates. Liquidity management involves fore-

casting funding requirements and maintaining sufficient capacity to

meet the needs and accommodate fluctuations in asset and liability

levels due to changes in our business operations or unanticipated

events. Sources of liquidity include deposits and other customer-

based funding, wholesale market-based funding, and liquidity pro-

vided by the sale or securitization of assets.

We manage liquidity at two levels. The first is the liquidity of the

parent company, which is the holding company that owns the banking

and nonbanking subsidiaries. The second is the liquidity of the banking

subsidiaries. The management of liquidity at both levels is essential

because the parent company and banking subsidiaries each have

different funding needs and sources, and each are subject to certain

regulatory guidelines and requirements. Through ALCO, the Finance

Committee is responsible for establishing our liquidity policy as well as

approving operating and contingency procedures, and monitoring liquidity

on an ongoing basis. Corporate Treasury is responsible for planning and

executing our funding activities and strategy.

In order to ensure adequate liquidity through the full range of

potential operating environments and market conditions, we conduct

our liquidity management and business activities in a manner that

will preserve and enhance funding stability, flexibility, and diversity.

Key components of this operating strategy include a strong focus on

customer-based funding, maintaining direct relationships with whole-

sale market funding providers, and maintaining the ability to liquefy

certain assets when, and if requirements warrant.