Bank of America 2004 Annual Report Download - page 140

Download and view the complete annual report

Please find page 140 of the 2004 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

-

152

-

153

-

154

|

|

BANK OF AMERICA 2004 139

$56 million, respectively, in 2004, $4 million and $52 million, respec-

tively, in 2003, and $5 million and $61 million, respectively, in 2002.

A one-percentage-point decrease in assumed health care cost trend

rates would have lowered the service and interest costs and the ben-

efit obligation by $3 million and $48 million, respectively, in 2004, $3

million and $48 million, respectively, in 2003, and $4 million and $52

million, respectively, in 2002.

Plan Assets

The Qualified Pension Plans have been established as retirement

vehicles for participants, and trusts have been established to secure

benefits promised under the Qualified Pension Plans. The

Corporation’s policy is to invest the trust assets in a prudent manner

for the exclusive purpose of providing benefits to participants and

defraying reasonable expenses of administration. The Corporation’s

investment strategy is designed to provide a total return that, over

the long-term, increases the ratio of assets to liabilities. The strategy

attempts to maximize the investment return on assets at a level of

risk deemed appropriate by the Corporation while complying with

ERISA and any subsequent applicable regulations and laws. The

investment strategy utilizes asset allocation as a principal determi-

nant for establishing the risk/reward profile of the assets. Asset allo-

cation ranges are established, periodically reviewed, and adjusted as

funding levels and liability characteristics change. Active and passive

investment managers are employed to help enhance the risk/return

profile of the assets. An additional aspect of the investment strategy

used to minimize risk (part of the asset allocation plan) includes

matching the equity exposure of participant-selected earnings meas-

ures. For example, the common stock of the Corporation held in the

trust is maintained as an offset to the exposure related to partici-

pants who selected to receive an earnings measure based on the

return performance of common stock of the Corporation.

The Expected Return on Asset Assumption (EROA assumption)

was developed through analysis of historical market returns, histori-

cal asset class volatility and correlations, current market conditions,

anticipated future asset allocations, the funds’ past experience, and

expectations on potential future market returns. The EROA assump-

tion represents a long-term average view of the performance of the

Qualified Pension Plans and Postretirement Health and Life Plan

assets, a return that may or may not be achieved during any one cal-

endar year. In a simplistic analysis of the EROA assumption, the build-

ing blocks used to arrive at the long-term return assumption would

include an implied return from equity securities of 9 percent, debt

securities of 6 percent, and real estate of 9 percent for all pension

plans and postretirement health and life plans.

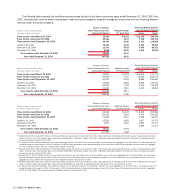

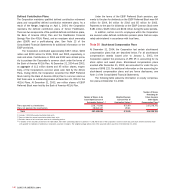

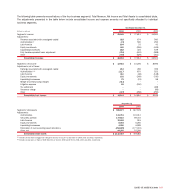

The Qualified Pension Plans’ asset allocation at December 31,

2004 and 2003 and target allocation for 2005 by asset category are

as follows:

Percentage of Plan Assets

2005 Target at December 31

Asset Category Allocation 2004 2003

Equity securities 65 -80% 75% 71%

Debt securities 20- 35% 23 28

Real estate 0-3% 21

Total 100% 100%

Equity securities include common stock of the Corporation in the

amounts of $871 million (7.17 percent of total plan assets) and

$809 million (9.02 percent of total plan assets) at December 31,

2004 and 2003, respectively.

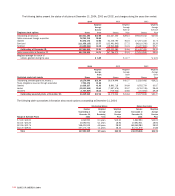

The Postretirement Health and Life Plans’ asset allocation at

December 31, 2004 and 2003 and target allocation for 2005 by

asset category are as follows:

Percentage of Plan Assets

2005 Target at December 31

Asset Category Allocation 2004 2003

Equity securities 60 -75% 75% 69%

Debt securities 22- 40% 24 31

Real estate 0-3% 1–

Total 100% 100%

The Bank of America Postretirement Health and Life Plans had no

investment in the common stock of the Corporation at December 31,

2004 or 2003. The FleetBoston Postretirement Health and Life Plans

included common stock of the Corporation in the amount of $0.3 mil-

lion (0.20 percent of total plan assets) at December 31, 2004.

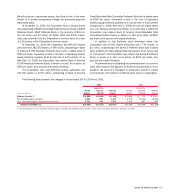

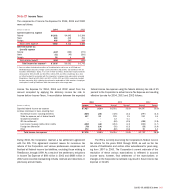

Projected Benefit Payments

Benefit payments projected to be made from the Qualified Pension

Plans, the Nonqualified Pension Plans and the Postretirement Health

and Life Plans are as follows: Postretirement

Qualified Nonqualified Health and Life Plans

Pension Pension Net Medicare

(Dollars in millions) Plans(1) Plans(2) Payments(3) Subsidy

2005 $ 806 $ 114 $ 109 $ –

2006 831 89 109 (6)

2007 856 81 107 (6)

2008 881 93 104 (6)

2009 908 92 101 (6)

2010-2014 4,803 519 457 (26)

(1) Benefit payments expected to be made from the plans’ assets.

(2) Benefit payments expected to be made from the Corporation’s assets.

(3) Benefit payments (net of retiree contributions) expected to be made from a combination of the

plans’ and the Corporation’s assets.