Bank of America 2004 Annual Report Download - page 76

Download and view the complete annual report

Please find page 76 of the 2004 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

|

|

BANK OF AMERICA 2004 75

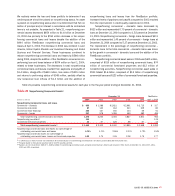

Approximately $4 million of the increase in average VAR for 2004 was

attributable to the addition of FleetBoston in the second quarter of

2004. The remaining increase in average VAR for 2004 was primarily

due to increases in the average risk taken in credit and equities. The

increase in equities was mainly due to the increased economic risk

from customer-facilitated transactions that were held in inventory dur-

ing portions of 2004. The increase in credit was mainly due to an

increase in credit protection purchased to hedge the credit risk in our

commercial credit portfolio.

Stress Testing

Because the very nature of a VAR model suggests results can exceed

our estimates, we “stress test” our portfolio. Stress testing estimates

the value change in our trading portfolio due to abnormal market

movements. Various stress scenarios are run regularly against the

trading portfolio to verify that, even under extreme market moves, we

will preserve our capital; to determine the effects of significant his-

torical events; and to determine the effects of specific, extreme hypo-

thetical, but plausible events. The results of the stress scenarios are

calculated daily and reported to senior management as part of the

regular reporting process. The results of certain specific, extreme

hypothetical scenarios are presented to ALCO.

(Dollars in millions)

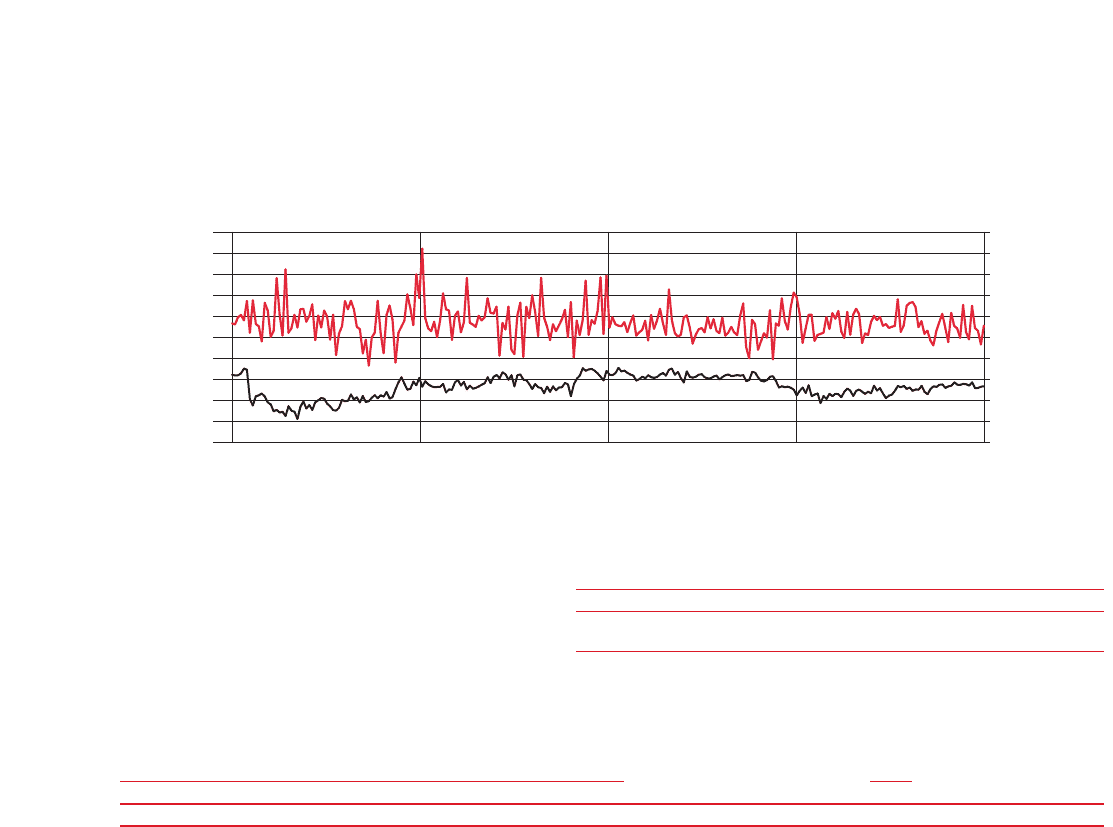

Trading Risk and Return

Daily VAR and Trading-related Revenue

12/31/03 3/31/04 6/30/04 9/30/04 12/31/04

Daily Trading-

related Revenue

VAR

-100

-80

60

0

-20

-40

-60

20

40

100

80

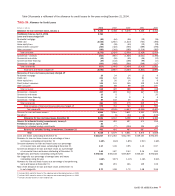

Table 26 presents average, high and low daily VAR for 2004 and 2003.

Table 26

Trading Activities Market Risk

Twelve Months Ended December 31

2004 2003

Average High Low Average High Low

(Dollars in millions) VAR VAR(1) VAR(1) VAR VAR(1) VAR(1)

Foreign exchange $ 3.6 $ 8.1 $ 1.4 $ 4.1 $ 7.8 $ 2.1

Interest rate 26.2 51.5 10.7 27.0 65.2 15.1

Credit(2) 35.7 61.4 21.9 20.7 32.6 14.9

Real estate/mortgage(3) 10.5 26.0 4.6 14.1 41.4 3.6

Equities 21.8 51.5 7.9 19.9 53.8 6.6

Commodities 6.5 10.2 3.8 8.7 19.3 4.1

Portfolio diversification (56.3) – – (60.9) – –

Total trading portfolio $ 48.0 $ 78.5 $ 29.4 $ 33.6 $ 91.0 $ 11.2

Total market-based trading portfolio(4) $ 44.1 $ 79.0 $ 23.7 $ 33.2 $ 82.0 $ 11.8

(1) The high and low for the total portfolio may not equal the sum of the individual components as the highs or lows of the individual portfolios may have occurred on different trading days.

(2) Credit includes credit fixed income and credit default swaps used for credit risk management. Average VAR for credit default swaps was $23.5 and $20.9 in 2004 and 2003, respectively.

(3) Real estate/mortgage includes capital market real estate and the Certificates. Effective June 1, 2004, Real estate/mortgage no longer includes the Certificates. For additional information on the

Certificates, see Note 1 of the Consolidated Financial Statements.

(4) Total market-based trading portfolio excludes credit default swaps used for credit risk management, net of the effect of diversification.

The following graph shows actual losses did not exceed VAR in 2004. Actual losses exceeded VAR twice during 2003.