Bank of America 2004 Annual Report Download - page 75

Download and view the complete annual report

Please find page 75 of the 2004 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

|

|

74 BANK OF AMERICA 2004

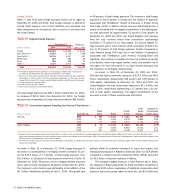

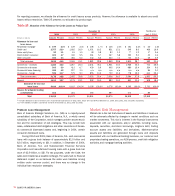

The above histogram does not include two losses greater than

$50 million associated with MSRs as the losses were related to

model changes rather than market changes in the portfolio. For

additional information on MSRs, see Notes 1 and 8 of the

Consolidated Financial Statements.

To evaluate risk in our trading activities, we focus on the actual

and potential volatility of individual positions as well as portfolios. At

a portfolio and corporate level, we use Value-at-Risk (VAR) modeling

and stress testing. VAR is a key statistic used to measure and man-

age market risk. Trading limits and VAR are used to manage day-to-

day risks and are subject to testing where we compare expected

performance to actual performance. This testing provides us a view

of our models’ predictive accuracy. All limit excesses are communicated

to senior management for review.

A VAR model estimates a range of hypothetical scenarios within

which the next day’s profit or loss is expected. These estimates are

impacted by the nature of the positions in the portfolio and the cor-

relation within the portfolio. Within any VAR model, there are signifi-

cant and numerous assumptions that will differ from company to

company. Our VAR model assumes a 99 percent confidence level.

Statistically this means that losses will exceed VAR, on average, one

out of 100 trading days, or two to three times each year.

In addition to reviewing our underlying model assumptions with

senior management, we seek to mitigate the uncertainties related to

these assumptions and estimates through close monitoring and by

updating the assumptions and estimates on an ongoing basis. If the

results of our analysis indicate higher than expected levels of risk,

proactive measures are taken to adjust risk levels.

Trading Risk Management

Trading-related revenues represent the amount earned from our trading

positions, which include trading account assets and liabilities, as well

as derivative positions and, prior to the conversion of the Certificates

into MSRs, market value adjustments to the Certificates and the

MSRs. Trading positions are taken in a diverse range of financial

instruments and markets. Trading account assets and liabilities, and

derivative positions are reported at fair value. MSRs are reported at

lower of cost or market. For more information on fair value, see

Complex Accounting Estimates beginning on page 78. For additional

information on MSRs, see Notes 1 and 8 of the Consolidated

Financial Statements. Trading Account Profits represent the net

amount earned from our trading positions and, as reported in the

Consolidated Statement of Income, do not include the Net Interest

Income recognized on trading positions, or the related funding charge

or benefit. Trading Account Profits can be volatile and are largely

driven by general market conditions and customer demand. Trading

Account Profits are dependent on the volume and type of transactions,

the level of risk assumed, and the volatility of price and rate movements

at any given time within the ever-changing market environment.

The histogram of daily revenue or loss below is a graphic

depiction of trading volatility and illustrates the level of trading-

related revenue for 2004. Trading-related revenue encompasses both

proprietary trading and customer-related activities. In 2004, positive

trading-related revenue was recorded for 87 percent of trading days.

Furthermore, only five percent of the total trading days had losses

greater than $10 million, and the largest loss was $27 million. This

can be compared to 2003 and 2002 as follows:

•In 2003, positive trading-related revenue was recorded for 88

percent of trading days and only four percent of total trading

days had losses greater than $10 million, and the largest loss

was $41 million.

•In 2002, positive trading-related revenue was recorded for 86

percent of trading days and only five percent of total trading

days had losses greater than $10 million, and the largest loss

was $32 million.

Revenue

Number of Days

(Dollars in millions)

Histogram of Daily Trading-related Revenue

Twelve Months Ended December 31, 2004

< -50 -50 to -40 -40 to -30 -30 to -20 -20 to -10 -10 to 0 0 to 10 10 to 20 20 to 30 30 to 40 40 to 50 > 50

0

30

60

80

70

50

40

20

10