Bank of America 2004 Annual Report Download - page 135

Download and view the complete annual report

Please find page 135 of the 2004 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

|

|

134 BANK OF AMERICA 2004

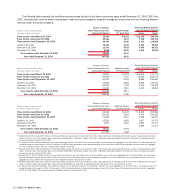

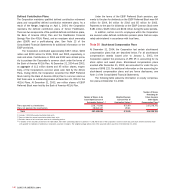

The calculation of earnings per common share and diluted earnings

per common share for 2004, 2003 and 2002 is presented below.

See Note 1 of the Consolidated Financial Statements for a discus-

sion on the calculation of earnings per common share.

(Dollars in millions,

except per share information;

shares in thousands) 2004 2003 2002

Earnings per common share

Net income $ 14,143 $ 10,810 $ 9,249

Preferred stock dividends (16) (4) (5)

Net income available to

common shareholders $ 14,127 $ 10,806 $ 9,244

Average common shares

issued and outstanding 3,758,507 2,973,407 3,040,085

Earnings per common share $ 3.76 $ 3.63 $ 3.04

Diluted earnings per

common share

Net income available to

common shareholders $ 14,127 $ 10,806 $ 9,244

Convertible preferred

stock dividends 245

Net income available to

common shareholders and

assumed conversions $ 14,129 $ 10,810 $ 9,249

Average common shares

issued and outstanding 3,758,507 2,973,407 3,040,085

Dilutive potential

common shares(1,2) 65,436 56,949 90,850

Total diluted average common

shares issued and outstanding 3,823,943 3,030,356 3,130,935

Diluted earnings per

common share $ 3.69 $ 3.57 $ 2.95

(1) For 2004, 2003 and 2002, average options to purchase 10 million, 19 million and 45 million

shares, respectively, were outstanding but not included in the computation of earnings per

common share because they were antidilutive.

(2) Includes incremental shares from assumed conversions of convertible preferred stock,

restricted stock units, restricted stock shares and stock options.

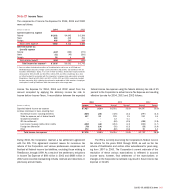

Note 14

Regulatory Requirements and Restrictions

The Board of Governors of the Federal Reserve System (FRB) requires

the Corporation’s banking subsidiaries to maintain reserve balances

based on a percentage of certain deposits. Average daily reserve bal-

ances required by the FRB were $6.9 billion and $4.1 billion for 2004

and 2003, respectively. Currency and coin residing in branches and

cash vaults (vault cash) are used to partially satisfy the reserve

requirement. The average daily reserve balances, in excess of vault

cash, held with the Federal Reserve Bank amounted to $70 million

and $317 million for 2004 and 2003, respectively.

The primary source of funds for cash distributions by the

Corporation to its shareholders is dividends received from its bank-

ing subsidiaries. Bank of America, N.A. and Fleet National Bank

declared and paid dividends of $5.9 billion and $1.3 billion, respec-

tively, for 2004 to the parent. In 2005, Bank of America, N.A. and

Fleet National Bank can declare and pay dividends to the parent of

$4.7 billion and $790 million plus an additional amount equal to their

net profits for 2005, as defined by statute, up to the date of any such

dividend declaration. The other subsidiary national banks can initiate

aggregate dividend payments in 2005 of $2.6 billion plus an addi-

tional amount equal to their net profits for 2005, as defined by

statute, up to the date of any such dividend declaration. The amount

of dividends that each subsidiary bank may declare in a calendar year

without approval by the OCC is the subsidiary bank’s net profits for

that year combined with its net retained profits, as defined, for the

preceding two years.

The FRB, the OCC and the Federal Deposit Insurance

Corporation (collectively, the Agencies) have issued regulatory capital

guidelines for U.S. banking organizations. Failure to meet the capital

requirements can initiate certain mandatory and discretionary

actions by regulators that could have a material effect on the

Corporation’s financial statements. At December 31, 2004 and

2003, the Corporation and Bank of America, N.A. were classified as

well-capitalized under this regulatory framework. At December 31,

2004, Fleet National Bank was classified as well-capitalized under

this regulatory framework. There have been no conditions or events

since December 31, 2004 that management believes have changed

the Corporation’s, Bank of America, N.A.’s or Fleet National Bank’s

capital classifications.