Bank of America 2004 Annual Report Download - page 77

Download and view the complete annual report

Please find page 77 of the 2004 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

|

|

76 BANK OF AMERICA 2004

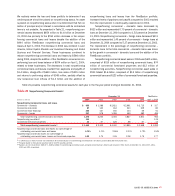

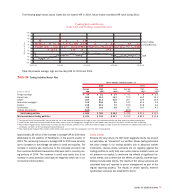

Interest Rate Risk Management

Interest rate risk represents the most significant market risk exposure

to our nontrading financial instruments. Our overall goal is to manage

interest rate sensitivity so that movements in interest rates do not

adversely affect Net Interest Income. Interest rate risk is measured

as the potential volatility in our Net Interest Income caused by

changes in market interest rates. Client facing activities, primarily

lending and deposit-taking, create interest rate sensitive positions on

our Balance Sheet. Interest rate risk from these activities as well as

the impact of ever-changing market conditions, is mitigated using the

ALM process.

Sensitivity simulations are used to estimate the impact on Net

Interest Income of numerous interest rate scenarios, balance sheet

trends and strategies. These simulations estimate levels of short-

term financial instruments, debt securities, loans, deposits, borrow-

ings and derivative instruments. In addition, these simulations

incorporate assumptions about balance sheet dynamics such as loan

and deposit growth and pricing, changes in funding mix, and asset

and liability repricing and maturity characteristics. In addition to Net

Interest Income sensitivity simulations, market value sensitivity

measures are also utilized.

The Balance Sheet Management group maintains a Net Interest

Income forecast utilizing different rate scenarios, with the base case

utilizing the forward market curve. The Balance Sheet Management

group constantly updates the Net Interest Income forecast for chang-

ing assumptions and differing outlooks based on economic trends

and market conditions.

The Balance Sheet Management group reviews the impact on

Net Interest Income of parallel and nonparallel shifts in the yield curve

over different time horizons. The overall interest rate risk position and

strategies are reviewed on an ongoing basis with ALCO. At December

31, 2004, we remain positioned for future rising interest rates and

curve flattening to the extent implied by the forward market curve.

The estimated impact to Net Interest Income over the subse-

quent year from December 31, 2004, resulting from a 100 bp grad-

ual (over 12 months) parallel increase or decrease in interest rates

from the forward market curve calculated as of December 31, 2004

was (1.5) percent and 0.5 percent, respectively. The estimated

impact to Net Interest Income over the subsequent year from

December 31, 2003, resulting from a 100 bp gradual (over 12

months) parallel increase or decrease in interest rates from the for-

ward market curve calculated as of December 31, 2003, was (1.1)

percent and 1.2 percent, respectively.

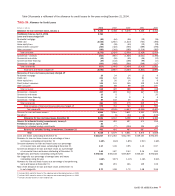

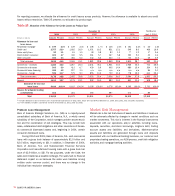

As part of the ALM process, we use securities, residential

mortgages, and interest rate and foreign exchange derivatives in

managing interest rate sensitivity.

Securities

The securities portfolio is integral to our ALM process. The decision

to purchase or sell securities is based upon the current assessment

of economic and financial conditions, including the interest rate envi-

ronment, liquidity and regulatory requirements, and the relative mix of

our cash and derivative positions. During 2004 and 2003, we pur-

chased securities of $232.6 billion and $195.9 billion, respectively,

sold $105.0 billion and $171.5 billion, respectively, and received pay-

downs of $31.8 billion and $27.2 billion, respectively. Not included in

the purchases above were $46.7 billion of forward purchase con-

tracts of both mortgage-backed securities and mortgage loans at

December 31, 2004 settling from January 2005 to February 2005

with an average yield of 5.26 percent, and $65.2 billion of forward

purchase contracts of both mortgage-backed securities and mort-

gage loans at December 31, 2003 that settled from January 2004 to

February 2004 with an average yield of 5.79 percent. There were also

$25.8 billion of forward sale contracts of mortgage-backed securities

at December 31, 2004 settling from January 2005 to February 2005

with an average yield of 5.47 percent compared to $8.0 billion at

December 31, 2003 that settled in February 2004 with an average

yield of 6.14 percent. These forward purchase and sale contracts

were accounted for as derivatives and designated as cash flow

hedges with their net-of-tax unrealized gains and losses included in

Accumulated Other Comprehensive Income (OCI). For additional infor-

mation on derivatives designated as cash flow hedges, see Note 4 of

the Consolidated Financial Statements. The forward purchase and

sale contracts at December 31, 2004 and 2003 were also included in

Table

IV

on pages 88 and 89. During the year, we continuously moni-

tored the interest rate risk position of the portfolio and repositioned

the securities portfolio in order to manage prepayment risk and to take

advantage of interest rate fluctuations. Through sales in the securities

portfolio, we realized $2.1 billion and $941 million in Gains on Sales

of Debt Securities in 2004 and 2003, respectively.