Bank of America 2004 Annual Report Download - page 89

Download and view the complete annual report

Please find page 89 of the 2004 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

|

|

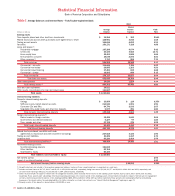

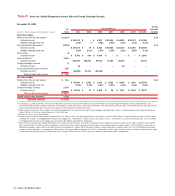

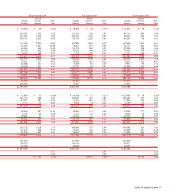

Table IV

Asset and Liability Management Interest Rate and Foreign Exchange Contracts

December 31, 2004

Average

Fair Expected Maturity Estimated

(Dollars in millions, average estimated duration in years) Value Total 2005 2006 2007 2008 2009 Thereafter Duration

Cash flow hedges

Receive fixed interest rate swaps(1) $ (1,413) 4.16

Notional amount $ 122,274 $ – $ 2,927 $ 21,098 $ 44,223 $ 22,237 $ 31,789

Weighted average fixed rate 3.68% –% 3.46% 2.94% 3.47% 3.73% 4.43%

Pay fixed interest rate swaps(1) (2,248) 4.77

Notional amount $ 157,837 $ 39 $ 6,320 $ 62,584 $ 16,136 $ 10,289 $ 62,469

Weighted average fixed rate 4.24% 5.01% 3.54% 3.58% 3.91% 3.85% 5.13%

Basis swaps (4)

Notional amount $ 6,700 $ 500 $ 4,400 $ – $ – $ – $ 1,800

Option products(2) 3,492

Notional amount(3) 323,835 145,200 90,000 17,500 58,404 – 12,731

Foreign exchange contracts 9

Notional amount 16–––16––

Futures and forward rate contracts(4) 287

Notional amount(3) (10,889) 10,111 (21,000) – – – –

Total net cash flow positions $ 123

Fair value hedges

Receive fixed interest rate swaps(1) $ 534 5.14

Notional amount $ 45,050 $ 2,580 $ 4,363 $ 2,500 $ 2,694 $ 3,364 $ 29,549

Weighted average fixed rate 5.02% 4.78% 5.23% 4.53% 3.47% 4.44% 5.25%

Foreign exchange contracts 2,739

Notional amount $ 13,590 $ 71 $ 1,529 $ 55 $ 1,571 $ 2,091 $ 8,273

Total net fair value positions $ 3,273

Closed interest rate contracts(5) 1,328

Total ALM contracts $ 4,724

(1) At December 31, 2004, $39.9 billion of the receive fixed interest rate swap notional and $75.9 billion of the pay fixed interest swap notional represented forward starting swaps that will not be

effective until their respective contractual start dates. At December 31, 2003, $14.2 billion of the receive fixed interest rate swap notional and $114.5 billion of the pay fixed interest rate swap notional

represented forward starting swaps that will not be effective until their respective contractual start dates.

(2) Option products include caps, floors, swaptions and exchange-traded options on index futures contracts. These strategies may include option collars or spread strategies, which involve the buying and

selling of options on the same underlying security or interest rate index.

(3) Reflects the net of long and short positions.

(4) Futures and forward rate contracts include Eurodollar futures, U.S. Treasury futures, and forward purchase and sale contracts. Included are $50.0 billion of forward purchase contracts, and $25.6 billion

of forward sale contracts of mortgage-backed securities and mortgage loans, at December 31, 2004, as discussed on page 76 and 77. At December 31, 2003, the forward purchase and sale contracts

of mortgage-backed securities and mortgage loans amounted to $69.8 billion and $8.0 billion, respectively.

(5) Represents the unamortized net realized deferred gains associated with closed contracts. As a result, no notional amount is reflected for expected maturity. The $1.3 billion and $839 million deferred

gains as of December 31, 2004 and 2003, respectively, on closed interest rate contracts primarily consisted of gains on closed ALM swaps and forward contracts. Of the $1.3 billion unamortized net

realized deferred gains, a gain of $836 million was included in Accumulated OCI, a gain of $514 million was included as a basis adjustment of Long-term Debt, and a loss of $22 million was primarily

included as a basis adjustment to mortgage loans, AFS Securities and Long-term Debt at December 31, 2004. As of December 31, 2003, a gain of $238 million was included in Accumulated OCI, a gain

of $631 million was primarily included as a basis adjustment of long-term debt, and a loss of $30 million was included as a basis adjustment to mortgage loans.

88 BANK OF AMERICA 2004