Bank of America 2004 Annual Report Download - page 44

Download and view the complete annual report

Please find page 44 of the 2004 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

|

|

BANK OF AMERICA 2004 43

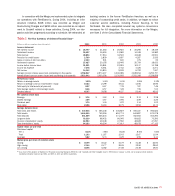

The following table presents the components of Total Revenue

for Card Services on a managed and held basis.

Card Services Revenue

2004 2003

(Dollars in millions) Managed Held Managed Held

Net interest income $ 5,079 $4,236 $ 2,856 $ 2,537

Noninterest income 3,061 3,246 1,930 2,065

Total card services revenue $ 8,140 $7,482 $ 4,786 $ 4,602

Strong credit card performance and the addition of the FleetBoston

card portfolio drove Card Services results. Held credit card revenue

increased $2.9 billion, or 63 percent, to $7.5 billion. Driving this

increase was the $1.7 billion increase in held Net Interest Income,

due to a $15.2 billion, or 54 percent, increase in average held con-

sumer credit card outstandings, partially offset by a decline in average

Deposits of $3.3 billion. The increase in held consumer credit card

outstandings was due to the addition of over five million new accounts

through our branch network and direct marketing programs, and the

$5.0 billion impact of the addition of the held FleetBoston consumer

credit card portfolio. The decline in Deposits was due to a change in

the fee structure in the merchant business for certain accounts from

a compensating balance to a fee for service agreement. Managed

credit card revenue increased $3.4 billion, or 70 percent, to $8.1 billion.

This increase included the $2.2 billion, or 78 percent, increase in

managed Net Interest Income. Average managed consumer credit card

outstandings were $50.3 billion in 2004 compared to $31.6 billion.

The increase in held credit card Noninterest Income of $1.2 billion

resulted from higher interchange fees of $381 million. Interchange

fees increased mainly due to a $21.4 billion, or 38 percent, increase

in consumer credit card purchase volumes. Also impacting

Noninterest Income were increases in late fees of $238 million, mer-

chant discount fees of $197 million, overlimit fees of $107 million

and cash advance fees of $64 million. The effect of the addition of

FleetBoston on these fee categories was $169 million on interchange

fees, $77 million on late fees, $47 million on merchant discount

fees, $37 million on overlimit fees, and $24 million on cash advance

fees, respectively. Noninterest Income on a managed basis increased

$1.1 billion, or 59 percent, during 2004.

The held Provision for Credit Losses increased $1.2 billion, or

68 percent, to $3.0 billion driven by higher net charge-offs of $791

million, of which $320 million was attributable to the addition of the

FleetBoston card portfolio. Organic growth, overall seasoning of

accounts, the return of securitized loans to the balance sheet and

increases in minimum payment requirements drove higher net

charge-offs and Provision for Credit Losses. Net losses on the port-

folio that was securitized were $524 million and $177 million for

2004 and 2003. The increase was attributable to the addition of the

FleetBoston portfolio. For more information, see Credit Risk

Management beginning on page 58.

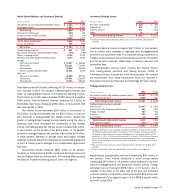

Consumer Real Estate

Consumer Real Estate generates revenue by providing an extensive

line of mortgage products and services to customers nationwide.

Consumer Real Estate products are available to our customers

through a retail network of personal bankers located in 5,885 bank-

ing centers, dedicated sales account executives in over 190 loca-

tions and through a devoted sales force offering our customers direct

telephone and online access to our products. Additionally, we serve

our customers through a partnership with more than 7,200 mortgage

brokers in all 50 states. The mortgage product offerings for home

purchase and refinancing needs include fixed and adjustable rate

loans, first and second lien loans, home equity lines of credit, and lot

and construction loans. To manage this portfolio, these products are

either sold into the secondary mortgage market to investors while we

retain the customer relationship and servicing rights or are held in

our ALM portfolio.

Consumer Real Estate is managed with a focus on its two primary

businesses, first mortgage and home equity. The first mortgage busi-

ness includes the origination, fulfillment and servicing of first mort-

gage loan products. The home equity business includes lines of

credit and second mortgages. These two businesses provide us with

a business model that meets customer mortgage borrowing needs in

various interest rate cycles.

The following table shows the revenue components of the

Consumer Real Estate business.

Consumer Real Estate Revenue

(Dollars in millions) 2004 2003

Net interest income $ 2,224 $ 1,795

Mortgage banking income(1,2) 595 2,140

Trading account profits (349) (159)

Gains on sales of debt securities 117 –

Other income 61 96

Total consumer real estate revenue $ 2,648 $ 3,872

(1) Includes gains related to hedge ineffectiveness of cash flow hedges on our mortgage

warehouse of $117 and $38 for 2004 and 2003.

(2) For 2004 and 2003, Mortgage Banking Income included revenue of $181 and $218 for

mortgage services provided to other segments that are eliminated in consolidation (in All Other).

Total revenue for the Consumer Real Estate business decreased by

$1.2 billion, or 32 percent, in 2004. Net Interest Income increased

by $429 million driven by higher average balances in the home equity

line and loan portfolio, which grew from $21.7 billion in 2003 to

$39.0 billion in 2004. This portfolio growth was attributable to an

expanded home equity market through the addition of FleetBoston,

which contributed $18.5 billion, and the increased product distribu-

tion. The home equity business had a record year in 2004, producing

$57.1 billion in loans and lines compared to $23.4 billion in 2003.

Partially offsetting this growth, Net Interest Income decreased $90

million in 2004 due to a lower level of escrow deposits held on loans

serviced. Average escrow balances declined $2.8 billion during the

year.