Bank of America 2004 Annual Report Download - page 42

Download and view the complete annual report

Please find page 42 of the 2004 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

|

|

BANK OF AMERICA 2004 41

Equity is allocated to business segments using a risk-adjusted

methodology incorporating each unit’s credit, market and operational

risk components. The nature of these risks is discussed further

beginning on page 58. ROE is calculated by dividing Net Income by

allocated equity. SVA is defined as cash basis earnings on an oper-

ating basis less a charge for the use of capital (i.e. equity). Cash

basis earnings on an operating basis are defined as Net Income

adjusted to exclude Merger and Restructuring Charges, and

Amortization of Intangibles. The charge for use of capital is calcu-

lated by multiplying 11 percent (management’s estimate of the share-

holders’ minimum required rate of return on capital invested) by

average total common shareholders’ equity at the corporate level and

by average allocated equity at the business segment level. Average

equity is allocated to the business level using a methodology identi-

cal to that used in the ROE calculation. Management reviews the esti-

mate of the rate used to calculate the capital charge annually. In

2003, management reduced this rate from 12 percent to 11 percent.

We use the Capital Asset Pricing Model to estimate our cost of capital.

The change in the cost of capital rate from 12 percent to 11 percent

was driven by a decline in long-term Treasury rates, which impacted

the risk-free rate component of the calculation.

See Note 19 of the Consolidated Financial Statements for addi-

tional business segment information, selected financial information

for the business segments and reconciliations to consolidated Total

Revenue, Net Income and Total Assets amounts.

Global Consumer and Small Business Banking

Our strategy is to attract, retain and deepen customer relationships.

A critical component of that strategy includes continuously improving

customer satisfaction. We believe this focus will help us achieve our

goal of being recognized as the best retail bank in North America.

The major businesses within this segment are Consumer

Banking, Consumer Products and Small Business Banking.

Consumer Banking distributes a wide range of services to

33 million consumer households in 29 states and the District of

Columbia through its network of 5,885 banking centers, 16,791

domestic branded ATMs, and telephone and Internet channels.

Consumer Banking distributes a wide range of products, and serv-

ices, including deposit products such as checking accounts, money

market savings accounts, time deposits and IRAs, debit card products,

and credit products such as credit card, home equity products and

residential mortgages. Consumer Banking recorded $16.7 billion of

Total Revenue for 2004. This represented a 35 percent increase. Total

average Deposits within Consumer Banking were $276.7 billion, up 35

percent from 2003.

Consumer Products provides and manages products and services

including the issuance and servicing of credit cards, origination,

fulfillment and servicing of residential mortgage loans, including

home equity loan products, direct banking via the Internet, deposit

services, student lending and certain insurance services. Consumer

Products contributed $8.4 billion of Total Revenue, which represented

a 16 percent improvement. Average Loans and Leases during the

year increased 52 percent to $49.9 billion.

Small Business Banking helps small businesses grow through

the offering of business products and services which include payroll,

merchant services, online banking and bill payment, as well as 401(k)

programs. In addition, we provide specialized products like treasury

management, lockbox, check cards with photo security and succession

planning. Small Business Banking reported $1.7 billion of Total

Revenue, compared to $1.2 billion in 2003. Average Loans and

Leases improved 28 percent to $15.3 billion. Also, Total Deposits

within Small Business Banking grew 37 percent to $31.9 billion due

to the impact of the Merger and account growth.

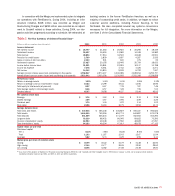

Global Consumer and Small Business Banking

(Dollars in millions) 2004 2003

Net interest income (fully taxable-equivalent basis) $ 17,308 $ 12,114

Noninterest income 9,549 8,816

Total revenue 26,857 20,930

Provision for credit losses 3,341 1,678

Gains on sales of debt securities 117 13

Noninterest expense 13,334 10,333

Income before income taxes 10,299 8,932

Income tax expense 3,751 3,226

Net income $ 6,548 $ 5,706

Shareholder value added $ 3,390 $ 4,367

Net interest yield (fully taxable-equivalent basis) 5.35% 4.98%

Return on average equity 19.89 42.25

Efficiency ratio (fully taxable-equivalent basis) 49.64 49.37

Average:

Total loans and leases $137,357 $ 92,776

Total assets 352,789 258,251

Total deposits 314,652 240,371

Common equity/Allocated equity 32,925 13,505

Year end:

Total loans and leases 156,280 97,341

Total assets 378,359 264,578

Total deposits 333,723 240,428

Total Revenue for Global Consumer and Small Business Banking

increased $5.9 billion, or 28 percent, of which FleetBoston con-

tributed $4.3 billion. Provision for Credit Losses increased $1.7 billion

to $3.3 billion. Noninterest Expense grew by $3.0 billion, or 29 percent,

to $13.3 billion. Net Income rose $842 million, or 15 percent, including

the $1.1 billion impact of the addition of FleetBoston. SVA decreased

$977 million, or 22 percent. This decrease was caused by an

increase in the capital allocation as a result of the Merger partially

offset by the increase in cash basis earnings.