Bank of America 2004 Annual Report Download - page 146

Download and view the complete annual report

Please find page 146 of the 2004 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154

|

|

BANK OF AMERICA 2004 145

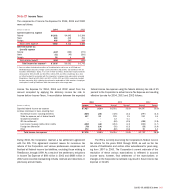

the same counterparty on a net basis. For exchange-traded contracts,

fair value is based on quoted market prices. For non-exchange traded

contracts, fair value is based on dealer quotes, pricing models or

quoted prices for instruments with similar characteristics. The fair

value of the Corporation’s derivative assets and liabilities is pre-

sented in Note 4 of the Consolidated Financial Statements.

Loans

Fair values were estimated for groups of similar loans based upon

type of loan and maturity. The fair value of loans was determined by

discounting estimated cash flows using interest rates approximating

the Corporation’s current origination rates for similar loans and

adjusted to reflect the inherent credit risk. Where quoted market

prices were available, primarily for certain residential mortgage loans

and commercial loans, such market prices were utilized as estimates

for fair values.

Substantially all of the foreign loans reprice within relatively

short timeframes. Accordingly, for foreign loans, the net carrying val-

ues were assumed to approximate their fair values.

Deposits

The fair value for deposits with stated maturities was calculated by

discounting contractual cash flows using current market rates for

instruments with similar maturities. The carrying value of foreign time

deposits approximates fair value. For deposits with no stated matu-

rities, the carrying amount was considered to approximate fair value

and does not take into account the significant value of the cost

advantage and stability of the Corporation’s long-term relationships

with depositors.

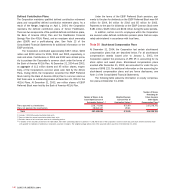

The book and fair values of certain financial instruments at

December 31, 2004 and 2003 were as follows:

December 31

2004 2003

Book Fair Book Fair

(Dollars in millions) Value Value Value Value

Financial assets

Loans $491,615 $496,873 $353,924 $357,770

Financial liabilities

Deposits 618,570 618,409 414,113 414,379

Long-term debt 98,078 102,439 75,343 79,442

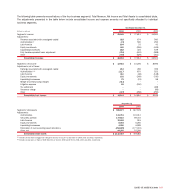

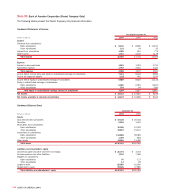

Note 19

Business Segment Information

In connection with the Merger, the Corporation realigned its business

segment reporting to reflect the new business model of the combined

company. The Corporation reports the results of its operations

through four business segments: Global Consumer and Small

Business Banking, Global Business and Financial Services, Global

Capital Markets and Investment Banking, and Global Wealth and

Investment Management. Certain operating segments have been

aggregated into a single business segment. The Corporation may

periodically reclassify business segment results based on modifica-

tions to its management reporting and profitability measurement

methodologies, and changes in organizational alignment.

Global Consumer and Small Business Banking provides a diver-

sified range of products and services to individuals and small busi-

nesses through multiple delivery channels. Global Business and

Financial Services primarily provides commercial lending and treasury

management services to middle-market companies. Global Capital

Markets and Investment Banking provides capital-raising solutions,

advisory services, derivatives capabilities, equity and debt sales and

trading for the Corporation’s clients as well as traditional bank

deposit and loan products, treasury management and payment

services to large corporations and institutional clients. Global Wealth

and Investment Management offers investment, fiduciary and com-

prehensive banking and credit expertise, asset management

services to institutional clients, high-net-worth individuals and retail

customers, investment, securities and financial planning services to

affluent and high-net-worth individuals, and retail clearing services

for broker/dealers.

All Other consists primarily of Latin America, Equity Investments,

Noninterest Income and Expense amounts associated with the ALM

process, including Gains on Sales of Debt Securities, the allowance

for credit losses process, the residual impact of methodology alloca-

tions, intersegment eliminations, and the results of certain consumer

finance and commercial lending businesses that are being liquidated.

Latin America includes the Corporation’s full-service Latin American

operations in Brazil, Argentina and Chile.

Total Revenue includes Net Interest Income on a fully taxable-

equivalent basis and Noninterest Income. The adjustment of Net

Interest Income to a fully taxable-equivalent basis results in a corre-

sponding increase in Income Tax Expense. The Net Interest Income

of the business segments includes the results of a funds transfer

pricing process that matches assets and liabilities with similar inter-

est rate sensitivity and maturity characteristics. Net Interest Income

also reflects an allocation of Net Interest Income generated by

assets and liabilities used in the Corporation’s ALM process.

Certain expenses not directly attributable to a specific business

segment are allocated to the segments based on pre-determined

means. The most significant of these expenses include data pro-

cessing costs, item processing costs and certain centralized or

shared functions. Data processing costs are allocated to the seg-

ments based on equipment usage. Item processing costs are allo-

cated to the segments based on the volume of items processed for

each segment. The costs of certain centralized or shared functions

are allocated based on methodologies which reflect utilization.