Bank of America 2004 Annual Report Download - page 39

Download and view the complete annual report

Please find page 39 of the 2004 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

|

|

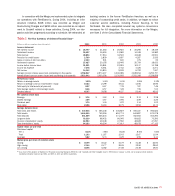

Supplemental Financial Data

Table 2 provides a reconciliation of the supplemental financial data

mentioned below with GAAP financial measures. Other companies

may define or calculate supplemental financial data differently.

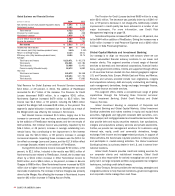

Operating Basis Presentation

In managing our business, we may at times look at performance

excluding certain non-recurring items. For example, as an alternative

to Net Income, we view results on an operating basis, which repre-

sents Net Income excluding Merger and Restructuring Charges. The

operating basis of presentation is not defined by accounting princi-

ples generally accepted in the United States (GAAP). We believe that

the exclusion of Merger and Restructuring Charges, which represent

events outside our normal operations, provides a meaningful period-

to-period comparison and is more reflective of normalized operations.

Net Interest Income - FTE Basis

In addition, we view Net Interest Income and related ratios and analysis

(i.e. efficiency ratio, net interest yield and operating leverage) on a

FTE basis. Although this is a non-GAAP measure, we believe manag-

ing the business with Net Interest Income on a FTE basis provides a

more accurate picture of the interest margin for comparative pur-

poses. To derive the FTE basis, Net Interest Income is adjusted to

reflect tax-exempt interest income on an equivalent before tax basis

with a corresponding increase in Income Tax Expense. For purposes

of this calculation, we use the federal statutory tax rate of 35 percent.

This measure ensures comparability of Net Interest Income arising

from both taxable and tax-exempt sources.

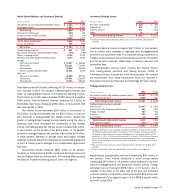

Performance Measures

As mentioned above, certain performance measures including the

efficiency ratio, net interest yield, and operating leverage utilize Net

Interest Income (and thus Total Revenue) on a FTE basis. The effi-

ciency ratio measures the costs expended to generate a dollar of

revenue, and net interest yield evaluates how many basis points we

are earning over the cost of funds. Operating leverage measures the

total percentage revenue growth minus the total percentage expense

growth for the corresponding period. During our annual integrated

plan process, we set operating leverage and efficiency targets for the

Corporation and each line of business. Targets vary by year and by

business and are based on a variety of factors, including: maturity of

the business, investment appetite, competitive environment, market

factors, and other items (i.e. risk appetite). The aforementioned per-

formance measures and ratios, earnings per common share (EPS),

return on average assets, return on average common shareholders’

equity and dividend payout ratio, as well as those measures discussed

more fully below are presented in Table 2, Supplemental Financial

Data and Reconciliations to GAAP Financial Measures.

Return on Average Equity and Shareholder Value Added

We also evaluate our business based upon return on average equity

(ROE) and shareholder value added (SVA) measures. ROE and SVA,

both utilize non-GAAP allocation methodologies. ROE measures the

earnings contribution of a unit as a percentage of the Shareholders’

Equity allocated to that unit. SVA is defined as cash basis earnings

on an operating basis less a charge for the use of capital. For more

information, see Basis of Presentation beginning on page 40. Both

measures are used to evaluate the Corporation’s use of equity

(i.e. capital) at the individual unit level and are integral components

in the analytics for resource allocation. Using SVA as a performance

measure places specific focus on whether incremental investments

generate returns in excess of the costs of capital associated with

those investments. Investments and initiatives are analyzed using

SVA during the annual planning process for maximizing allocation of

corporate resources. In addition, profitability, relationship and

investment models all use SVA and ROE as key measures to support

our overall growth goal.

38 BANK OF AMERICA 2004