Bank of America 2004 Annual Report Download - page 71

Download and view the complete annual report

Please find page 71 of the 2004 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

|

|

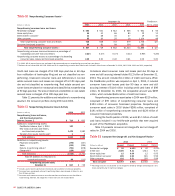

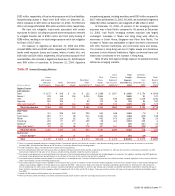

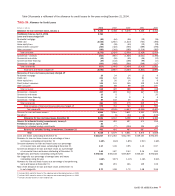

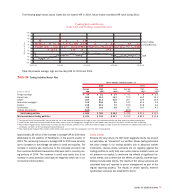

The allowance for commercial loan and lease losses as presented

in Table 25 was $3.2 billion at December 31, 2004, a $726 million

increase from December 31, 2003. This increase was due to the

addition on April 1, 2004 of $1.7 billion of FleetBoston allowance for

commercial loans and leases to the portfolio partially offset by reduc-

tions resulting from improvement in the commercial loan portfolio.

Commercial credit quality continues to improve as reflected in the

continued declines in both commercial criticized exposure and com-

mercial nonperforming loans and leases. Specific reserves on com-

mercial impaired loans decreased $189 million, or 48 percent, in

2004, reflecting the decrease in our investment in specific loans con-

sidered impaired of $910 million to $1.2 billion at December 31,

2004. The net decrease of $910 million included the addition of

FleetBoston impaired loans on April 1, 2004 of $914 million offset

by net decreases of $1.8 billion in 2004. The decreased levels of crit-

icized, nonperforming and impaired loans, and the respective

reserves were driven by overall improvement in commercial credit

quality, including paydowns and payoffs, loan sales, net charge-offs

and returns to performing status.

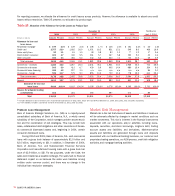

The general portion of the Allowance for Loan and Lease Losses

increased $438 million during 2004. The addition of FleetBoston

general reserves on April 1, 2004 accounted for $508 million of the

increase. Although uncertainty regarding the depth and pace of the

economic recovery existed early in the year, the fourth quarter demon-

strated a strengthening of the economy, which led to a reduction in gen-

eral reserves of $70 million in 2004.

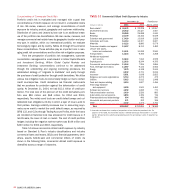

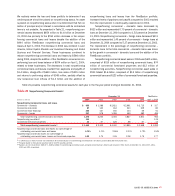

Reserve for Unfunded Lending Commitments

In addition to the Allowance for Loan and Lease Losses, we also estimate

probable losses related to unfunded lending commitments, such as

letters of credit and financial guarantees, and binding unfunded loan

commitments. Unfunded lending commitments are subject to individ-

ual reviews, and are analyzed and segregated by risk according to the

Corporation’s internal risk rating scale. These risk classifications, in

conjunction with an analysis of historical loss experience, current

economic conditions and performance trends within specific portfolio

segments, and any other pertinent information result in the estima-

tion of the reserve for unfunded lending commitments. The reserve

for unfunded lending commitments is included in Accrued Expenses

and Other Liabilities on the Consolidated Balance Sheet.

We monitor differences between estimated and actual incurred

credit losses. This monitoring process includes periodic assess-

ments by senior management of credit portfolios and the models

used to estimate incurred losses in those portfolios.

Additions to the reserve for unfunded lending commitments are

made by charges to the Provision for Credit Losses. Credit exposures

(excluding derivatives) deemed to be uncollectible are charged

against the reserve.

The reserve for unfunded lending commitments decreased $14

million from December 31, 2003, primarily due to improved economic

conditions and improvement in the level of criticized letters of credit,

partially offset by the addition of $85 million of reserves on April 1,

2004 associated with FleetBoston unfunded lending commitments.

70 BANK OF AMERICA 2004