Bank of America 2004 Annual Report Download - page 8

Download and view the complete annual report

Please find page 8 of the 2004 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

|

|

The results for our first nine months as one company, from April 1 to December 31, confirm that we achieved

what we set out to do.

For example, net checking account growth in the Northeast increased from about 35,000 in 2003 to about

200,000 in 2004, and savings account growth registered strong gains as well. Not only are customers giving us a vote

of confidence with their purchase decisions, they’re also telling us their satisfaction is growing, which bodes well for

future growth. Between June and December, customers in the Northeast who rated their experience in the banking

centers a 9 or a 10 on a 10-point scale increased from 51% to 61%.

We have been extremely pleased with our early results, and these results have been gaining in strength since

we launched the Bank of America brand across the Northeast between August and December of last year. Even so,

we believe our greatest growth potential in the Northeast lies before us, not behind us. Even given our strong results

so far, our market penetration and share of wallet in Northeast markets remains low relative to potential business

opportunity. This is especially true in Global Wealth and Investment Management, where we see significant opportuni-

ties to grow by capturing more of our existing customers’ wealth planning business.

The merger transition process itself has been, without qualification, the smoothest and fastest I have seen in

my career. From the beginning, we planned and executed the transition and all associated projects with strict

adherence to a disciplined Six Sigma approach, improving processes, driving down costs and enhancing quality and

productivity along the way.

We continue to face significant transition challenges and opportunities in the Northeast in 2005. We will meet

those challenges and seize those opportunities with the same energy, enthusiasm and intensity that led to our success

in 2004, and drive toward ever-higher growth goals throughout the Northeast for the future.

Smart growth

To generate strong, consistent, sustainable organic growth in financial services, achieving excellence in sales and

service is half the battle. The other half is developing the art and science of risk and reward management as a core

competency and competitive advantage.

Today, your company is developing the skills and tools that enable us to grow by taking the right risks, and by

getting paid appropriately for the risks we take. We are continuing to build a risk and reward management structure

and culture of shared responsibility, in which every associate—from front-line bankers to risk managers to auditors—

is accountable for managing risks to help the business grow.

This structure is important in helping us manage credit risk, but we also apply it to a broad view of risk, including

market risks and operational risks related to technology, systems, events, or legal, compliance and reputation issues.

We believe industry-leading risk management means playing good offense as well as good defense. At the

beginning of this letter, for example, I mentioned a partnership through which we distribute fixed-income

BANK OF AMERICA 2004 7

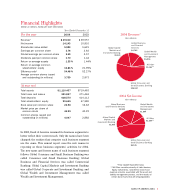

'02 '03 '04

$2.95

$3.57 $3.69

'02 '03 '04

19.4%

22.0%

16.8%

Earnings Per Common Share

(Diluted)

Return on Average Common

Shareholders’ Equity