Bank of America 2004 Annual Report Download - page 41

Download and view the complete annual report

Please find page 41 of the 2004 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

|

|

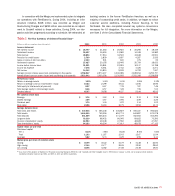

Core Net Interest Income

In addition, we review core net interest income which adjusts reported

Net Interest Income on a FTE basis for the impact of trading-related

activities. As discussed in the Global Capital Markets and Investment

Banking business segment section beginning on page 46, we evaluate

our trading results and strategies based on total trading-related rev-

enue, calculated by combining trading-related Net Interest Income with

Trading Account Profits. We also adjust for loans that we originated and

sold into revolving credit card, home equity line and commercial loan

securitizations. Noninterest Income, rather than Net Interest Income

and Provision for Credit Losses, is recorded for assets that have been

securitized as we are compensated for servicing the securitized assets

and record servicing income and gains or losses on securitizations,

where appropriate. An analysis of core net interest income, earning

assets and yields, which excludes these two non-core items from

reported Net Interest Income on a FTE basis, is shown below.

Table 3

Core Net Interest Income

(Dollars in millions) 2004 2003 2002

Net interest income

As reported

(fully taxable-equivalent basis) $ 29,513 $ 22,107 $ 21,511

Trading-related net interest income (2,039) (2,239) (1,977)

Impact of revolving securitizations 931 313 517

Core net interest income $ 28,405 $ 20,181 $ 20,051

Average earning assets

As reported $ 905,302 $ 649,548 $ 570,530

Trading-related earning assets (227,861) (172,825) (121,291)

Impact of revolving securitizations 10,181 3,342 5,943

Core average earning assets $ 687,622 $ 480,065 $ 455,182

Net interest yield on earning assets

As reported

(fully taxable-equivalent basis) 3.26% 3.40% 3.77%

Impact of trading-related activities 0.80 0.76 0.58

Impact of revolving securitizations 0.06 0.03 0.05

Core net interest yield on

earning assets 4.12% 4.19% 4.40%

Core net interest income increased $8.2 billion for 2004. Approximately

half of the increase was due to the Merger. Other activities within the

portfolio affecting core net interest income were higher ALM portfolio lev-

els, the impact of higher rates, higher consumer loan levels (primarily

credit card loans and home equity lines) and higher core deposit fund-

ing levels, partially offset by reductions in the large corporate and foreign

loan balances, and lower mortgage warehouse levels.

Core average earning assets increased $207.6 billion primarily

due to higher ALM levels, (primarily securities and mortgages) and

higher levels of consumer loans (primarily credit card loans and home

equity lines). The increases in these assets were due to both the

Merger and organic growth.

The core net interest yield decreased seven bps due to the

impact of ALM portfolio repositioning, partially offset by the impact of

higher levels of consumer loans and core deposits.

Business Segment Operations

Segment Description

In connection with the Merger, we realigned our business segment

reporting to reflect the new business model of the combined company.

As a part of this realignment, the segment formerly reported as

Consumer and Commercial Banking was split into two new segments,

Global Consumer and Small Business Banking and Global Business and

Financial Services. We have repositioned Asset Management as Global

Wealth and Investment Management, which now includes Premier

Banking. Premier Banking was included in Consumer and Commercial

Banking in the past, and is made up of our affluent retail customers.

This will enable us to serve our customers with a diverse offering of

wealth management products. Global Capital Markets and Investment

Banking remained relatively unchanged, with the exception of moving

the commercial leasing business to Global Business and Financial

Services, and Latin America moving to All Other. All Other consists

primarily of Latin America, the former Equity Investments segment,

Noninterest Income and Expense amounts associated with the ALM

process, including Gains on Sales of Debt Securities, the allowance

for credit losses process, the residual impact of methodology allocations,

intersegment eliminations, and the results of certain consumer

finance and commercial lending businesses that are being liquidated.

Basis of Presentation

We prepare and evaluate segment results using certain non-GAAP

methodologies and performance measures many of which were dis-

cussed in Supplemental Financial Data on page 38. The starting

point in evaluating results is the operating results of the businesses,

which by definition excludes Merger and Restructuring Charges. The

segment results also reflect certain revenue and expense method-

ologies, which are utilized to determine operating income. The Net

Interest Income of the business segments includes the results of a

funds transfer pricing process that matches assets and liabilities

with similar interest rate sensitivity and maturity characteristics. Net

Interest Income also reflects an allocation of Net Interest Income

generated by assets and liabilities used in our ALM process. The

results of business segments will fluctuate based on the perform-

ance of corporate ALM activities.

Certain expenses not directly attributable to a specific business

segment are allocated to the segments based on pre-determined

means. The most significant of these expenses include data pro-

cessing costs, item processing costs and certain centralized or

shared functions. Data processing costs are allocated to the seg-

ments based on equipment usage. Item processing costs are allo-

cated to the segments based on the volume of items processed for

each segment. The costs of certain centralized or shared functions

are allocated based on methodologies which reflect utilization.

40 BANK OF AMERICA 2004