Bank of America 2004 Annual Report Download - page 57

Download and view the complete annual report

Please find page 57 of the 2004 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

|

|

56 BANK OF AMERICA 2004

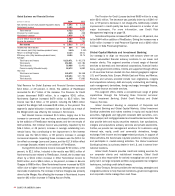

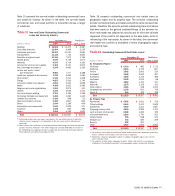

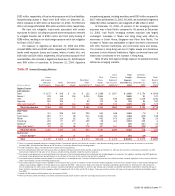

On- and Off-balance Sheet Financing Entities

Off-balance Sheet Commercial Paper Conduits

In addition to traditional lending, we also support our customers’

financing needs by facilitating their access to the commercial paper

markets. These markets provide an attractive, lower-cost financing

alternative for our customers. Our customers sell assets, such as

high-grade trade or other receivables or leases, to a commercial

paper financing entity, which in turn issues high-grade short-term

commercial paper that is collateralized by the assets sold.

Additionally, some customers receive the benefit of commercial paper

financing rates related to certain lease arrangements. We facilitate

these transactions and collect fees from the financing entity for the

services it provides including administration, trust services and

marketing the commercial paper.

We receive fees for providing combinations of liquidity, standby

letters of credit (SBLCs) or similar loss protection commitments, and

derivatives to the commercial paper financing entities. These forms

of asset support are senior to the first layer of asset support pro-

vided by customers through over-collateralization or by support pro-

vided by third parties. The rating agencies require that a certain

percentage of the commercial paper entity’s assets be supported by

both the seller’s over-collateralization and our SBLC in order to

receive their respective investment rating. The SBLC would be drawn

on only when the over-collateralization provided by the seller is not

sufficient to cover losses of the related asset. Liquidity commitments

made to the commercial paper entity are designed to fund scheduled

redemptions of commercial paper if there is a market disruption or

the new commercial paper cannot be issued to fund the redemption

of the maturing commercial paper. The liquidity facility has the same

legal priority as the commercial paper. We do not enter into any other

form of guarantee with these entities.

We manage our credit risk on these commitments by subjecting

them to our normal underwriting and risk management processes. At

December 31, 2004 and 2003, the Corporation had off-balance sheet

liquidity commitments and SBLCs to these entities of $23.8 billion

and $21.6 billion, respectively. Substantially all of these liquidity com-

mitments and SBLCs mature within one year. These amounts are

included in Table 8. Net revenues earned from fees associated with

these off-balance sheet financing entities were approximately $80 million

and $72 million for 2004 and 2003, respectively.

From time to time, we may purchase some of the commercial

paper issued by certain of these entities for our own account or acting

as a dealer on behalf of third parties. Derivative instruments related

to these entities are marked to market through the Consolidated

Statement of Income. SBLCs are initially recorded at fair value in

accordance with Financial Accounting Standards Board (FASB)

Interpretation No. 45, “Guarantor’s Accounting and Disclosure

Requirements for Guarantees” (FIN 45). Liquidity commitments and

SBLCs subsequent to inception are accounted for pursuant to SFAS

No. 5, “Accounting for Contingencies” (SFAS 5), and are discussed

further in Note 12 of the Consolidated Financial Statements.

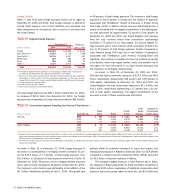

In January 2003, the FASB issued FASB Interpretation No. 46,

“Consolidation of Variable Interest Entities, an interpretation of ARB

No. 51” (FIN 46), which provides a framework for identifying variable

interest entities (VIEs) and determining when a company should

include the assets, liabilities, noncontrolling interests and results of

activities of a VIE in its consolidated financial statements. We

adopted FIN 46 on July 1, 2003 and consolidated approximately

$12.2 billion of assets and liabilities related to certain of our multi-

seller asset-backed commercial paper (ABCP) conduits. On October

8, 2003, one of these entities, Ranger Funding Company (RFC) (for-

merly known as Receivables Capital Corporation), entered into a

Subordinated Note Purchase Agreement (the Note) with an unrelated

third party which reduced our exposure to this entity’s losses under

liquidity and credit agreements as these agreements are senior to

the Note. This Note was issued in the principal amount of $23 mil-

lion, an original maturity of five years and pays interest at 23 percent.

Proceeds from the issuance of the Note were deposited into a sepa-

rate account and may be used to cover losses incurred by RFC. Upon

RFC’s issuance of this Note, we evaluated whether the Corporation

continued to be the primary beneficiary of RFC and determined that

the unrelated party which purchased the Note absorbed over 50 per-

cent of the expected losses of RFC. We determined the amount of

expected loss through mathematical analysis utilizing a Monte Carlo

model that incorporates the cash flows from RFC’s assets and utilizes

independent loss information. The noteholder is therefore the primary

beneficiary of and is required to consolidate the entity. As a result of

the sale of the Note, we deconsolidated approximately $8.0 billion of

the previously consolidated assets and liabilities of the entity. The

impact of this transaction on the Consolidated Statement of Income

was the reduction in Interest Income of approximately $1 million and

the reclassification of approximately $37 million from Net Interest

Income to Noninterest Income for 2003. At December 31, 2004, this

entity had total assets of $10.0 billion. Our exposure to this entity is

included in the total amount of liquidity agreements and SBLCs noted

above. There was no material impact to Net Income or Tier 1 Capital

as a result of the adoption of FIN 46 or the subsequent deconsoli-

dation of this entity, and prior periods were not restated. In December

2003, the FASB issued FASB Interpretation No. 46 (Revised

December 2003), “Consolidation of Variable Interest Entities, an

interpretation of ARB No. 51” (FIN 46R), which is an update of FIN

46. We adopted FIN 46R as of March 31, 2004. As a result of the

adoption of FIN 46R, there was no material impact on our results of

operations or financial condition.