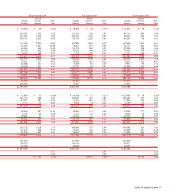

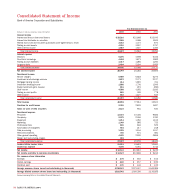

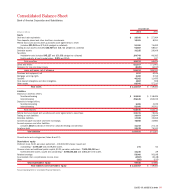

Bank of America 2004 Annual Report Download - page 104

Download and view the complete annual report

Please find page 104 of the 2004 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

|

|

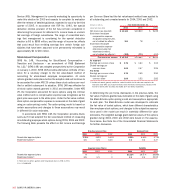

Compensation expense under the fair value-based method is recog-

nized over the vesting period of the related stock options.

Accordingly, the pro forma results of applying SFAS 123 in 2004,

2003 and 2002 may not be indicative of future amounts.

Cash and Cash Equivalents

Cash on hand, cash items in the process of collection, and amounts

due from correspondent banks and the Federal Reserve Bank are

included in Cash and Cash Equivalents.

Securities Purchased under Agreements to Resell and

Securities Sold under Agreements to Repurchase

Securities Purchased under Agreements to Resell and Securities

Sold under Agreements to Repurchase are treated as collateralized

financing transactions and are recorded at the amounts at which the

securities were acquired or sold plus accrued interest. The

Corporation’s policy is to obtain the use of Securities Purchased

under Agreements to Resell. The market value of the underlying secu-

rities, which collateralize the related receivable on agreements to

resell, is monitored, including accrued interest. The Corporation may

require counterparties to deposit additional collateral or return col-

lateral pledged, when appropriate.

Collateral

The Corporation has accepted collateral that it is permitted by con-

tract or custom to sell or repledge. At December 31, 2004, the fair

value of this collateral was approximately $152.5 billion of which

$117.5 billion was sold or repledged. At December 31, 2003, the fair

value of this collateral was approximately $86.9 billion of which

$62.8 billion was sold or repledged. The primary source of this col-

lateral is reverse repurchase agreements. The Corporation pledges

securities as collateral in transactions that consist of repurchase

agreements, public and trust deposits, Treasury tax and loan notes,

and other short-term borrowings. This collateral can be sold or

repledged by the counterparties to the transactions.

In addition, the Corporation obtains collateral in connection

with its derivative activities. Required collateral levels vary depend-

ing on the credit risk rating and the type of counterparty. Generally,

the Corporation accepts collateral in the form of cash, U.S. Treasury

securities and other marketable securities. Based on provisions con-

tained in legal netting agreements, the Corporation has netted cash

collateral against the applicable derivative mark-to-market expo-

sures. Accordingly, the Corporation offsets its obligation to return or

its right to reclaim cash collateral against the fair value of the deriv-

atives being collateralized.

Trading Instruments

Financial instruments utilized in trading activities are stated at fair

value. Fair value is generally based on quoted market prices. If quoted

market prices are not available, fair values are estimated based on

dealer quotes, pricing models or quoted prices for instruments with

similar characteristics. Realized and unrealized gains and losses are

recognized in Trading Account Profits.

Derivatives and Hedging Activities

All derivatives are recognized on the Consolidated Balance Sheet at

fair value, taking into consideration the effects of legally enforceable

master netting agreements that allow the Corporation to settle posi-

tive and negative positions and offset cash collateral held with the

same counterparty on a net basis. For exchange-traded contracts, fair

value is based on quoted market prices. For non-exchange traded con-

tracts, fair value is based on dealer quotes, pricing models or quoted

prices for instruments with similar characteristics. The Corporation

designates at inception whether the derivative contract is considered

hedging or non-hedging for SFAS No. 133, “Accounting for Derivative

Instruments and Hedging Activities” (SFAS 133) accounting purposes.

Non-hedging derivatives held for trading purposes are included in the

Corporation’s trading portfolio with changes in fair value reflected in

Trading Account Profits. Other non-hedging derivatives for accounting

purposes that are considered economic hedges are also included in

the trading portfolio with changes in fair value generally recorded in

Trading Account Profits. Most credit derivatives used by the

Corporation do not qualify for hedge accounting under SFAS 133 and

despite being effective economic hedges, changes in the fair value of

these derivatives are included in Trading Account Profits. Changes in

the fair value of derivatives that serve as economic hedges of MSRs

are recorded in Mortgage Banking Income.

For SFAS 133 hedges, the Corporation formally documents at

inception all relationships between hedging instruments and hedged

items, as well as its risk management objectives and strategies for

undertaking various accounting hedges. Additionally, the Corporation

uses dollar offset or regression analysis at the hedge’s inception, and

quarterly thereafter, to assess whether the derivative used in its

hedging transaction is expected to be or has been highly effective in

offsetting changes in the fair value or cash flows of the hedged items.

The Corporation discontinues hedge accounting when it is deter-

mined that a derivative is not expected to be or has ceased to be

highly effective as a hedge, and then reflects changes in fair value in

earnings after termination of the hedge relationship.

The Corporation uses its derivatives designated as hedging for

accounting purposes as either fair value hedges, cash flow hedges or

hedges of net investments in foreign operations. The Corporation man-

ages interest rate and foreign currency exchange rate sensitivity pre-

dominantly through the use of derivatives. Fair value hedges are used

to limit the Corporation’s exposure to total changes in the fair value of

its fixed interest-earning assets or interest-bearing liabilities that are

due to interest rate or foreign exchange volatility. Cash flow hedges

are used to minimize the variability in cash flows of interest-earning

BANK OF AMERICA 2004 103