Bank of America 2004 Annual Report Download - page 45

Download and view the complete annual report

Please find page 45 of the 2004 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

|

|

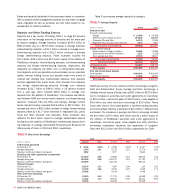

Mortgage Banking Income decreased from $2.1 billion in 2003

to $595 million. The following summarizes the components of

Mortgage Banking Income. Mortgage Banking Income includes the

performance of loans sold in the secondary market and the performance

of the servicing portfolio.

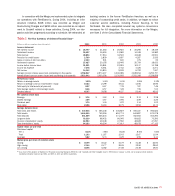

Mortgage Banking Income

(Dollars in millions) 2004 2003

Production income $ 771 $ 1,927

Servicing income:

Servicing fees and ancillary income 614 348

Amortization of MSRs (345) (135)

Net MSR and SFAS 133 derivative

hedge adjustments(1) 18 –

Impairment of MSRs (463) –

Total net servicing income (176) 213

Total mortgage banking income $ 595 $ 2,140

(1) Represents derivative hedge gains of $228, offset by a decrease in the value of the MSRs

under SFAS 133 hedges of $210 for 2004. See Note 8 of the Consolidated Financial Statements.

The decrease in Mortgage Banking Income was primarily driven by a

decline in the size of the first mortgage production market from the

record levels of 2003. In 2004, we produced $87.5 billion residential

first mortgages compared to $131.1 billion in the prior year. Of the

2004 volume, $57.5 billion was originated through retail channels

and $30.0 billion was originated in our wholesale channel. This com-

pares to 2003 with $91.8 billion originated through retail channels

and $39.3 billion originated through wholesale channels. During

2004, approximately 58 percent of the production was refinance activ-

ity compared to 84 percent in 2003. Additionally, the market and cus-

tomer preference has shifted the mix of fixed rate loans to 64 percent

in 2004, down from 80 percent in 2003. The decline in the size of the

market, excess industry capacity, and the rising interest rate environ-

ment also resulted in decreased operating margins. The volume reduc-

tions resulted in lower loan sales to the secondary market, which

totaled $69.4 billion, a 35 percent decrease from the prior year.

During 2004, impairment charges totaled $463 million, includ-

ing a $261 million adjustment for changes in valuation assumptions

and prepayment adjustments to align with changing market condi-

tions and customer behavioral trends. As an economic hedge to the

changes associated with the value of MSRs, a combination of deriv-

atives and AFS securities (e.g. mortgage-backed securities) was uti-

lized. During 2004, Consumer Real Estate realized $117 million in

Gains on Sales of Debt Securities and $65 million of Net Interest

Income from Securities used as an economic hedge of MSRs. At

December 31, 2004, $564 million in MSRs were covered by these

economic hedges. The remaining $1.8 billion in MSRs were hedged

using a SFAS No. 133, “Accounting for Derivative Instruments and

Hedging Activities” (SFAS 133) strategy.

Additionally, contributing to Consumer Real Estate revenue,

Trading Account Profits decreased by $190 million. Prior to conversion

of the Certificates to MSRs in June 2004, changes in the value of the

Certificates, MSRs and derivatives used for risk management were

recognized as Trading Account Profits. Trading Account Profits

included $342 million and $310 million of downward adjustments for

changes to valuation assumptions and prepayment adjustments in

2004 and 2003, respectively. For more information on the conversion,

see Note 1 of the Consolidated Financial Statements.

Other income includes premiums collected through our mortgage

insurance captive and other miscellaneous revenue items.

Servicing income is recognized when cash is received for per-

forming servicing activities for others. Servicing activities primarily

include collecting cash for principal, interest and escrow payments

from borrowers, and accounting for and remitting principal and inter-

est payments to investors of mortgage-backed securities. Servicing

income also includes any ancillary income, such as late fees, derived

in connection with these activities. The servicing portfolio includes

originated and retained residential mortgages, loans serviced for

others and home equity loans. As discussed more fully below, the

servicing portfolio ended 2004 at $332.5 billion, an increase of

$57.4 billion from December 31, 2003. The addition of FleetBoston

customers contributed $33.8 billion of this increase.

We recognize an intangible asset for the MSRs, which repre-

sents the right to perform specified residential mortgage servicing

activities for others. The amount capitalized as MSRs represents the

current fair value of future net cash flows expected to be realized for

performing servicing activities. MSRs are amortized as a reduction of

actual servicing income received. The following table outlines statistical

information on the MSRs:

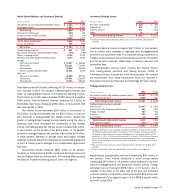

Mortgage Servicing Rights

December 31

(Dollars in millions) 2004 2003

MSR data:

Balance(1,2) $ 2,359 $ 2,684

Capitalization rate 1.19% 1.47%

Unpaid balance(3) $ 197,795 $183,116

Number of customers (in thousands) 1,582 1,586

(1) MSRs outside of Global Consumer and Small Business Banking at December 31, 2004 and 2003

were $123 and $78, respectively, in Global Capital Markets and Investment Banking.

(2) Includes $2,283 of Certificates at December 31, 2003. For more information on the Certificates,

see Note 1 of the Consolidated Financial Statements.

(3) Represents only loans serviced for others.

As of December 31, 2004, the MSR balance was $2.4 billion, or 12

percent lower than at the end of 2003. This value represented 119

bps as a percent of the related unpaid principal balance, a 19 percent

decrease from 2003. For more information on MSRs, see Notes 1

and 8 of the Consolidated Financial Statements.

44 BANK OF AMERICA 2004