Bank of America 2005 Annual Report Download - page 106

Download and view the complete annual report

Please find page 106 of the 2005 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

|

|

We prepare forward looking forecasts of Net Interest Income. These baseline forecasts take into consideration

expected future business growth, ALM positioning, and the direction of interest rate movements as implied by the

markets’ forward interest rate curve. We then measure and evaluate the impact that alternative interest rate scenarios

have to these static baseline forecasts in order to assess interest rate sensitivity under varied conditions. The spot and

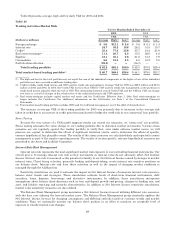

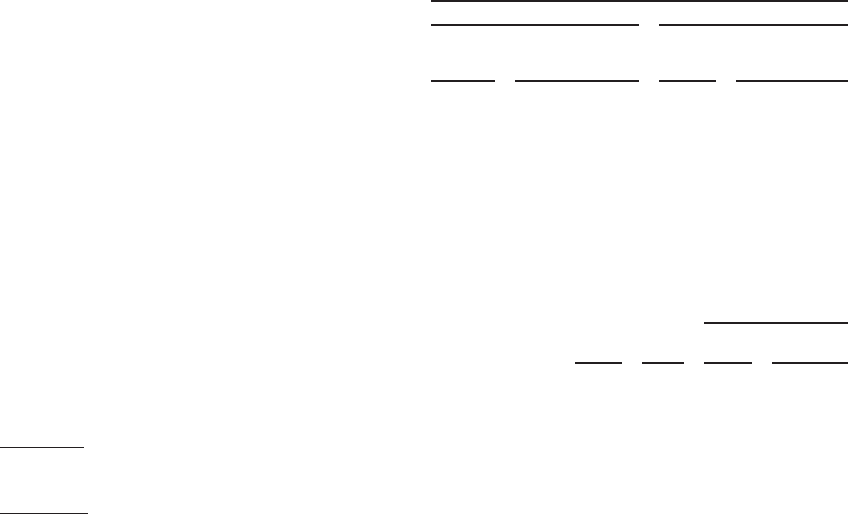

12-month forward rates used in our respective baseline forecasts at December 31, 2005 and 2004 were as follows:

Table 27

Forward Rates

December 31

2005 2004

Federal

Funds

Ten-Year

Constant

Maturity Swap Federal

Funds

Ten-Year

Constant

Maturity Swap

Spotrates .................................. 4.25% 4.94% 2.25% 4.64%

12-monthforwardrates ...................... 4.75 4.97 3.25 4.91

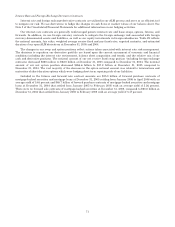

The following table reflects the pre-tax dollar impact to forecasted Core Net Interest Income over the next twelve

months from December 31, 2005 and 2004, resulting from a 100 bp gradual parallel increase, a 100 bp gradual parallel

decrease, a 100 bp gradual curve flattening (increase in short-term rates) and a 100 bp gradual curve steepening

(increase in long-tem rates) from the forward curve.

Table 28

Estimated Net Interest Income at Risk

(Dollars in millions) December 31

Curve Change Short

Rate Long

Rate 2005 2004

(Restated)

+100 Parallel shift .......................................... +100 +100 $(357) $(183)

-100Parallelshift .......................................... -100 -100 244 (126)

Flatteners

Shortend.............................................. +100 — (523) (462)

Longend .............................................. — -100 (298) (677)

Steepeners

Shortend.............................................. -100 — 536 497

Longend .............................................. — +100 168 97

The sensitivity analysis above assumes that we take no action in response to these rate shifts over the indicated

years.

Beyond what is already implied in the forward curve, we are modestly exposed to rising rates primarily due to

increased funding costs. Conversely, we would benefit from falling rates or a steepening of the yield curve beyond what is

already implied in the forward curve.

As part of the ALM process, we use securities, residential mortgages, and interest rate and foreign exchange

derivatives in managing interest rate sensitivity.

Securities

The securities portfolio is integral to our ALM process. The decision to purchase or sell securities is based upon the

current assessment of economic and financial conditions, including the interest rate environment, liquidity and

regulatory requirements, and the relative mix of our cash and derivative positions. During 2005, we purchased securities

of $204.5 billion, sold $134.5 billion, and received paydowns of $37.7 billion. During 2004, we purchased securities of

$243.6 billion, sold $117.7 billion, and received paydowns of $31.8 billion. During the year, we continuously monitored

our interest rate risk position and effected changes in the securities portfolio in order to manage prepayment risk and

interest rate risk. Through sales in the securities portfolio, we realized $1.1 billion in Gains on Sales of Debt Securities

during 2005 and $1.7 billion during 2004. The decrease was primarily due to lower gains realized on mortgage-backed

securities and corporate bonds.

Residential Mortgage Portfolio

During 2005, we purchased $32.0 billion of residential mortgages related to the ALM process. We had whole

mortgage loan sales of $10.1 billion during 2005. During 2004, we purchased $65.9 billion of residential mortgages

related to the ALM process and had minimal sales of whole mortgage loans. Additionally, we received paydowns of $35.8

billion and $44.4 billion for 2005 and 2004. Through sales of whole mortgage loans, we recognized gains that were

recorded as Other Income of $45 million for 2005, compared to losses of $2 million in 2004.

70