Bank of America 2005 Annual Report Download - page 90

Download and view the complete annual report

Please find page 90 of the 2005 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

|

|

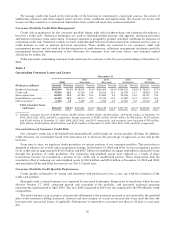

At December 31, 2005 and 2004, we had a net notional amount of credit default protection purchased in our credit

derivatives portfolio of $14.7 billion and $10.8 billion. Our credit portfolio hedges, including the impact of

mark-to-market, resulted in net gains of $49 million in 2005 and net losses of $144 million in 2004. Gains for 2005

primarily reflected the impact of spread widening in certain industries in the first half of the year.

Table 13 shows commercial utilized credit exposure by industry based on Standard & Poor’s industry classifications

and includes commercial loans and leases, SBLCs and financial guarantees, derivative assets, assets held-for-sale, and

commercial letters of credit. These amounts exclude the impact of our credit hedging activities, which are separately

included in the table. To lessen the cost of obtaining our desired credit protection levels, credit exposure may be added

within an industry, borrower or counterparty group by selling protection. A negative notional amount indicates a net

amount of protection purchased in a particular industry; conversely, a positive notional amount indicates a net amount

of protection sold in a particular industry. Credit protection is purchased to cover the funded portion as well as the

unfunded portion of credit exposure. As shown in the table below, commercial utilized credit exposure is diversified

across a range of industries.

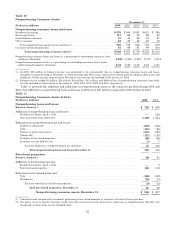

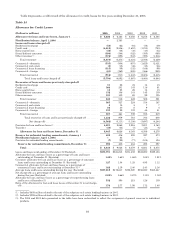

Table 13

Commercial Utilized Credit Exposure and Net Credit Default Protection by Industry

Commercial Utilized Credit Exposure(1) Net Credit Default Protection(2)

December 31 December 31

(Dollars in millions) 2005 2004 2005 2004

Real estate(3) ................................. $ 41,665 $ 36,672 $ (788) $ (268)

Banks ....................................... 26,514 25,265 31 61

Diversified financials .......................... 25,859 25,932 (543) (1,177)

Retailing ..................................... 23,913 23,149 (1,124) (829)

Education and government ..................... 22,331 17,429 ——

Individuals and trusts ......................... 17,237 16,110 (30) —

Materials .................................... 16,477 14,123 (1,149) (469)

Consumer durables and apparel ................. 14,988 13,427 (772) (406)

Capital goods ................................. 13,640 12,633 (751) (819)

Commercial services and supplies ............... 13,605 11,944 (472) (175)

Transportation ............................... 13,449 13,234 (392) (143)

Healthcare equipment and services .............. 13,294 12,196 (709) (354)

Leisureandsports,hotelsandrestaurants ....... 13,005 13,331 (874) (357)

Food, beverage and tobacco ..................... 11,578 11,687 (621) (226)

Energy ...................................... 9,992 7,579 (559) (457)

Media ....................................... 6,608 6,232 (1,790) (801)

Religious and social organizations ............... 6,340 5,710 ——

Utilities ...................................... 4,858 5,615 (899) (402)

Insurance .................................... 4,692 5,851 (1,453) (643)

Food and staples retailing ...................... 3,802 3,610 (334) (258)

Technology hardware and equipment ............ 3,737 3,398 (563) (301)

Telecommunicationservices .................... 3,461 3,030 (1,205) (808)

Softwareandservices.......................... 2,668 3,292 (299) (131)

Automobiles and components ................... 1,681 1,894 (679) (1,431)

Pharmaceuticals and biotechnology .............. 1,647 1,441 (470) (202)

Household and personal products ............... 379 371 75 8

Other........................................ 2,587 3,132 1,677(4) (260)(4)

Total .................................... $320,007 $298,287 $(14,693) $(10,848)

(1) Derivative assets are reported on a mark-to-market basis and have not been reduced by the amount of collateral applied. Derivative

asset collateral totaled $17.1 billion and $17.7 billion at December 31, 2005 and 2004.

(2) Represents notional amounts at December 31, 2005 and 2004.

(3) Industries are viewed from a variety of perspectives to best isolate the perceived risks. For purposes of this table, the real estate

industry is defined based upon the borrowers’ or counterparties’ primary business activity using operating cash flow and primary

source of repayment as key factors.

(4) Represents net CDS index positions, which were principally investment grade. Indices are comprised of corporate credit derivatives

that trade as an aggregate index value. Generally, they are grouped into portfolios based on specific ratings of credit quality or

global geographic location. As of December 31, 2005, CDS index positions were sold to reflect a short-term positive view of the credit

markets.

54