Bank of America 2005 Annual Report Download - page 146

Download and view the complete annual report

Please find page 146 of the 2005 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

|

|

BANK OF AMERICA CORPORATION AND SUBSIDIARIES

Notes to Consolidated Financial Statements—(Continued)

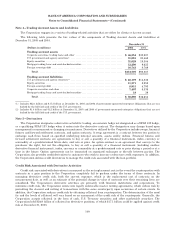

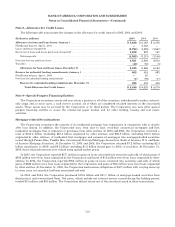

A portion of the derivative activity involves exchange-traded instruments. Exchange-traded instruments conform to

standard terms and are subject to policies set by the exchange involved, including margin and security deposit

requirements. Management believes the credit risk associated with these types of instruments is minimal. The average

fair value of Derivative Assets for 2005 and 2004 was $25.9 billion and $28.0 billion. The average fair value of Derivative

Liabilities for 2005 and 2004 was $16.8 billion and $15.7 billion.

The following table presents the contract/notional amounts and credit risk amounts at December 31, 2005 and 2004

of all the Corporation’s derivative positions. These derivative positions are primarily executed in the over-the-counter

market. The credit risk amounts take into consideration the effects of legally enforceable master netting agreements,

and on an aggregate basis have been reduced by the cash collateral applied against Derivative Assets. At December 31,

2005 and 2004, the cash collateral applied against Derivative Assets on the Consolidated Balance Sheet was $9.3 billion

and $9.4 billion. In addition, at December 31, 2005 and 2004, the cash collateral placed against Derivative Liabilities

was $7.6 billion and $6.0 billion.

Derivatives(1)

December 31

2005 2004

(Dollars in millions) Contract/

Notional Credit

Risk Contract/

Notional Credit

Risk

Interest rate contracts

Swaps ................................................................ $14,401,577 $11,085 $11,597,813 $12,705

Futuresandforwards ................................................... 2,113,717 — 1,833,216 332

Written options ........................................................ 900,036 — 988,253 —

Purchased options ...................................................... 869,471 3,345 1,243,809 4,840

Foreign exchange contracts

Swaps ................................................................ 333,487 3,735 305,999 7,859

Spot, futures and forwards ............................................... 944,321 2,481 956,995 3,593

Written options ........................................................ 214,668 — 167,225 —

Purchased options ...................................................... 229,049 1,214 163,243 679

Equity contracts

Swaps ................................................................ 28,287 548 34,130 1,039

Futuresandforwards ................................................... 6,479 44 4,078 —

Written options ........................................................ 69,048 — 37,080 —

Purchased options ...................................................... 57,693 6,729 32,893 5,741

Commodity contracts

Swaps ................................................................ 8,809 2,475 10,480 2,099

Futuresandforwards ................................................... 5,533 — 6,307 6

Written options ........................................................ 7,854 — 9,270 —

Purchased options ...................................................... 3,673 546 5,535 301

Credit derivatives(2) .......................................... 2,017,896 766 499,741 430

Creditriskbeforecashcollateral ......................................... 32,968 39,624

Less: Cash collateral applied ............................................. 9,256 9,389

Total derivative assets ............................................ $23,712 $30,235

(1) Includes long and short derivative positions.

(2) The increase in credit derivatives notional amounts reflects structured basket transactions and customer-driven activity.

ALM Process

Interest rate contracts and foreign exchange contracts are utilized in the Corporation’s ALM process. The

Corporation maintains an overall interest rate risk management strategy that incorporates the use of interest rate

contracts to minimize significant fluctuations in earnings that are caused by interest rate volatility. The Corporation’s

goal is to manage interest rate sensitivity so that movements in interest rates do not significantly adversely affect Net

Interest Income. As a result of interest rate fluctuations, hedged fixed-rate assets and liabilities appreciate or depreciate

in market value. Gains or losses on the derivative instruments that are linked to the hedged fixed-rate assets and

liabilities are expected to substantially offset this unrealized appreciation or depreciation. Interest Income and Interest

Expense on hedged variable-rate assets and liabilities increase or decrease as a result of interest rate fluctuations. Gains

and losses on the derivative instruments that are linked to these hedged assets and liabilities are expected to

substantially offset this variability in earnings.

110