Bank of America 2005 Annual Report Download - page 64

Download and view the complete annual report

Please find page 64 of the 2005 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

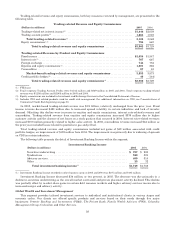

|

|

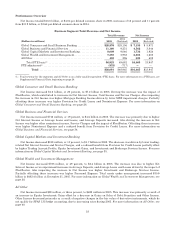

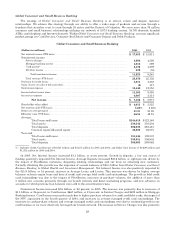

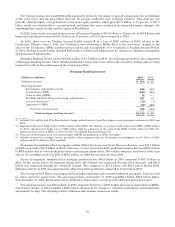

Global Consumer and Small Business Banking

The strategy of Global Consumer and Small Business Banking is to attract, retain and deepen customer

relationships. We achieve this strategy through our ability to offer a wide range of products and services through a

franchise that stretches coast to coast through 29 states and the District of Columbia. We serve more than 38 million

consumer and small business relationships utilizing our network of 5,873 banking centers, 16,785 domestic branded

ATMs, and telephone and Internet channels. Within Global Consumer and Small Business Banking, our most significant

product groups are Card Services, Consumer Real Estate and Consumer Deposit and Debit Products.

Global Consumer and Small Business Banking

(Dollars in millions) 2005 2004

Net interest income (FTE basis) ........................................................... $ 17,053 $ 15,911

Noninterest income:

Servicecharges...................................................................... 4,996 4,329

Mortgage banking income ............................................................ 1,012 589

Card income(1) ....................................................................... 5,476 4,359

Allotherincome ..................................................................... 339 (32)

Total noninterest income ......................................................... 11,823 9,245

Total revenue (FTE basis) ............................................................ 28,876 25,156

Provision for credit losses ................................................................. 4,271 3,333

Gains (losses) on sales of debt securities .................................................... (2) 117

Noninterest expense ..................................................................... 13,440 12,555

Income before income taxes ............................................................... 11,163 9,385

Income tax expense ...................................................................... 4,007 3,414

Net income .......................................................... $ 7,156 $ 5,971

Shareholder value added ................................................................. $ 4,013 $ 3,325

Net interest yield (FTE basis) ............................................................. 5.63% 5.46%

Return on average equity ................................................................. 21.31 21.28

Efficiency ratio (FTE basis) ............................................................... 46.54 49.91

Average:

Totalloansandleases .................................................. $144,019 $122,148

Total assets ........................................................... 330,342 316,204

Total deposits ......................................................... 306,038 283,481

Common equity/Allocated equity ......................................... 33,589 28,057

Year end:

Totalloansandleases .................................................. 151,646 139,507

Total assets ........................................................... 335,551 336,902

Total deposits ......................................................... 306,083 299,062

(1) Includes Credit Card Income of $3,847 million and $3,127 million for 2005 and 2004, and Debit Card Income of $1,629 million and

$1,232 million for 2005 and 2004.

In 2005, Net Interest Income increased $1.1 billion, or seven percent. Growth in deposits, a low cost source of

funding, positively impacted Net Interest Income. Average Deposits increased $22.6 billion, or eight percent, driven by

the impact of FleetBoston customers, deepening existing relationships and our focus on attracting new customers.

Partially offsetting this growth was the migration of account balances of $28.1 billion from Global Consumer and Small

Business Banking to Global Wealth and Investment Management. Net Interest Income was also positively impacted by

the $21.9 billion, or 18 percent, increase in Average Loans and Leases. This increase was driven by higher average

balances on home equity loans and lines of credit and average held credit card outstandings. The growth in held credit

card outstandings was due to the impact of FleetBoston, increases in purchase volumes, the addition of more than

5 million new accounts primarily through our branch network and direct marketing programs, and new advances on

accounts for which previous loan balances were sold to the securitization trusts.

Noninterest Income increased $2.6 billion, or 28 percent, in 2005. The increase was primarily due to increases of

$1.1 billion, or 26 percent, in Card Income, $667 million, or 15 percent, in Service Charges and $423 million in Mortgage

Banking Income. Card Income increased mainly due to higher purchase volumes for credit and debit cards, the impact of

the NPC acquisition in the fourth quarter of 2004, and increases in average managed credit card outstandings. The

increases in card purchase volumes and average managed credit card outstandings were due to continued growth in our

card business as we more effectively leveraged our branch network. The increase in Service Charges was due primarily

28