Bank of America 2005 Annual Report Download - page 81

Download and view the complete annual report

Please find page 81 of the 2005 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

|

|

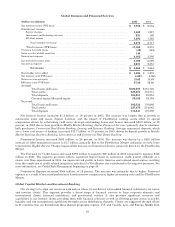

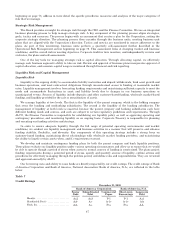

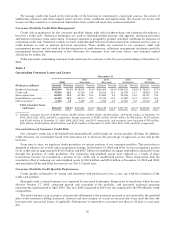

The following table summarizes the total unfunded, or off-balance sheet, credit extension commitment amounts by

expiration date. At December 31, 2005, charge cards (nonrevolving card lines) to individuals and government entities

guaranteed by the U.S. government in the amount of $9.4 billion (related outstandings of $171 million) were not

included in credit card line commitments in the table below.

Table 6

Credit Extension Commitments

December 31, 2005

(Dollars in millions)

Expires

in 1

year

or less

Expires

after 1

year

through

3 years

Expires

after 3

years

through

5 years

Expires

after 5

years Total

Loan commitments(1) ................................................. $112,829 $55,840 $80,748 $ 28,340 $277,757

Homeequitylinesofcredit ........................................... 1,317 714 1,673 74,922 78,626

Standby letters of credit and financial guarantees ....................... 22,320 8,661 5,361 6,753 43,095

Commercial letters of credit .......................................... 4,627 29 17 481 5,154

Legallybindingcommitments ..................................... 141,093 65,244 87,799 110,496 404,632

Creditcardlines .................................................... 180,694 12,274 — — 192,968

Total ...................................................... $321,787 $77,518 $87,799 $110,496 $597,600

(1) At December 31, 2005, there were equity commitments of $1.4 billion related to obligations to further fund Principal Investing

equity investments.

Managing Risk

Overview

Our management governance structure enables us to manage all major aspects of our business through an

integrated planning and review process that includes strategic, financial, associate, customer and risk planning. We

derive much of our revenue from managing risk from customer transactions for profit. In addition to qualitative factors,

we utilize quantitative measures to optimize risk and reward trade offs in order to achieve growth targets and financial

objectives while reducing the variability of earnings and minimizing unexpected losses. Risk metrics that allow us to

measure performance include economic capital targets, SVA targets and corporate risk limits. By allocating capital to a

business unit, we effectively define that unit’s ability to take on risk. Country, trading, asset allocation and other limits

supplement the allocation of economic capital. These limits are based on an analysis of risk and reward in each business

unit and management is responsible for tracking and reporting performance measurements as well as any exceptions to

guidelines or limits. Our risk management process continually evaluates risk and appropriate metrics needed to

measure it. Our business exposes us to the following major risks: strategic, liquidity, credit, market and operational.

Strategic Risk is the risk that adverse business decisions, ineffective or inappropriate business plans or failure to

respond to changes in the competitive environment, business cycles, customer preferences, product obsolescence,

execution and/or other intrinsic risks of business will impact our ability to meet our objectives. Liquidity risk is the

inability to accommodate liability maturities and deposit withdrawals, fund asset growth and meet contractual

obligations through unconstrained access to funding at reasonable market rates. Credit risk is the risk of loss arising

from a borrower’s or counterparty’s inability to meet its obligations. Market risk is the risk that values of assets and

liabilities or revenues will be adversely affected by changes in market conditions, such as interest rate movements.

Operational risk is the risk of loss resulting from inadequate or failed internal processes, people and systems or external

events.

Risk Management Processes and Methods

We have established control processes and use various methods to align risk-taking and risk management

throughout our organization. These control processes and methods are designed around “three lines of defense”: lines of

business; support units (including Risk Management, Compliance, Finance, Human Resources and Legal); and

Corporate Audit.

Management is responsible for identifying, quantifying, mitigating and managing all risks within their lines of

business, while certain enterprise-wide risks are managed centrally. For example, except for trading-related business

activities, interest rate risk associated with our business activities is managed in the Corporate Treasury and Corporate

Investment functions. Line of business management makes and executes the business plan and is closest to the changing

nature of risks and, therefore, we believe is best able to take actions to manage and mitigate those risks. Our lines of

business prepare quarterly self-assessment reports to identify the status of risk issues, including mitigation plans, if

45