Bank of America 2005 Annual Report Download - page 53

Download and view the complete annual report

Please find page 53 of the 2005 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

|

|

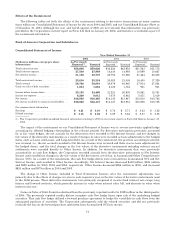

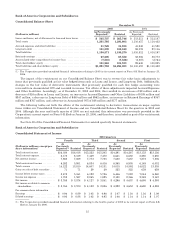

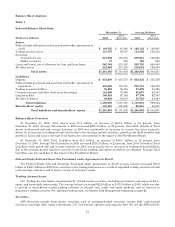

Bank of America Corporation and Subsidiaries

Consolidated Balance Sheet

2004 Quarters

Fourth Third Second First

(Dollars in millions)

As

Previously

Reported Restated

As

Previously

Reported Restated

As

Previously

Reported Restated

As

Previously

Reported Restated

Loans and leases, net of allowance

for loan and lease losses ......... $ 513,211 $ 513,187 $ 502,916 $ 502,890 $ 489,714 $ 489,685 $369,888 $369,858

Total assets ..................... 1,110,457 1,110,432 1,072,829 1,072,802 1,024,731 1,024,701 799,974 799,942

Accrued expenses and other

liabilities ...................... 41,243 41,590 28,851 29,205 28,682 28,747 18,635 19,269

Long-term debt .................. 98,078 97,116 100,586 99,582 98,319 98,082 81,231 79,474

Total liabilities ................... 1,010,812 1,010,197 974,818 974,168 928,910 928,738 751,198 750,075

Retainedearnings ................ 58,006 58,773 55,979 56,739 54,030 54,452 51,808 52,738

Accumulated other comprehensive

income (loss) ................... (2,587) (2,764) (2,669) (2,806) (3,862) (4,142) (2,743) (2,582)

Total shareholders’ equity ......... 99,645 100,235 98,011 98,634 95,821 95,963 48,776 49,867

Total liabilities and shareholders’

equity......................... $1,110,457 $1,110,432 $1,072,829 $1,072,802 $1,024,731 $1,024,701 $799,974 $799,942

Recent Events

On June 30, 2005, we announced a definitive agreement to acquire all outstanding shares of MBNA Corporation

(MBNA Merger), a leading provider of credit card and payment products, for approximately $35.0 billion in stock (85

percent) and cash (15 percent). This transaction closed on January 1, 2006. Under the terms of the agreement, MBNA

stockholders received 0.5009 of a share of our common stock plus $4.125 for each MBNA share of common stock.

On June 17, 2005, we announced a definitive agreement to purchase approximately nine percent of the stock of

China Construction Bank (CCB) for $3.0 billion. Under this agreement, we made an initial purchase of CCB shares for

$2.5 billion in August 2005 and an additional purchase of $500 million in October 2005, during CCB’s initial public

offering. These shares are non-transferable until the third anniversary of the initial public offering. We also hold an

option that allows us to increase our interest in CCB to 19.9 percent over the next five years. CCB is the third largest

commercial bank in China based on total assets.

Effective for the third quarter dividend, our Board of Directors (the Board) increased the quarterly cash dividend 11

percent from $0.45 to $0.50 per common share. In October 2005, the Board declared a fourth quarter cash dividend

which was paid on December 23, 2005 to common shareholders of record on December 2, 2005. In January 2006, the

Board declared a quarterly cash dividend of $0.50 per common share payable on March 24, 2006 to shareholders of

record on March 3, 2006.

On October 15, 2004, we acquired 100 percent of National Processing, Inc. (NPC), for $1.4 billion in cash, creating

the second largest merchant processor in the United States.

On April 1, 2004, we closed our merger with FleetBoston Financial Corporation (FleetBoston Merger). The merger

was accounted for under the purchase method of accounting. Accordingly, results for 2004 include the impact of

FleetBoston for nine months of combined company results.

Economic Overview

In 2005, economic performance was strong, despite a near doubling in energy prices, persistent hikes in the Federal

Funds rate and the destructive hurricanes in the second half of 2005. In the United States, real Gross Domestic Product

rose a solid 3.6 percent. Global economic expansion was healthy, as robust growth in Asian nations was offset by weaker

activity in core European nations. In the U.S., consumer spending was particularly resilient to the higher energy prices

that reduced real purchasing power. Rising employment and wages lifted personal income and financial wealth reached

an all-time high, while the rate of personal savings fell again. Following several years of robust increases in real estate

activity and housing values, real estate softened in the second half of 2005 and the volume of mortgage refinancing

receded. Heightened efficiencies generated sustained productivity gains that constrained costs of production and

contributed to record-breaking operating profits and cash flows. While business investment spending was strong and

employment gains firm, inventories remained lean. The strong business performance generated growth in business

lending and supported healthy credit quality. Although the higher energy prices pushed up headline inflation, core

inflation, which excludes the volatile food and energy prices, remained low. The Federal Reserve raised rates at every

Federal Open Market Committee meeting in 2005, lifting the Federal Funds rate to 4.25 percent at year-end. However,

these rate hikes were widely anticipated, contributing to very low bond yields and a significantly flatter yield curve.

17