Bank of America 2005 Annual Report Download - page 153

Download and view the complete annual report

Please find page 153 of the 2005 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

|

|

BANK OF AMERICA CORPORATION AND SUBSIDIARIES

Notes to Consolidated Financial Statements—(Continued)

The Corporation has retained MSRs from the sale or securitization of mortgage loans. Servicing fee and ancillary fee

income on all mortgage loans serviced, including securitizations, was $789 million and $568 million in 2005 and 2004.

The following table presents activity in MSRs in 2005 and 2004. Effective June 1, 2004, Excess Spread Certificates (the

Certificates) were converted to MSRs.

(Dollars in millions) 2005 2004

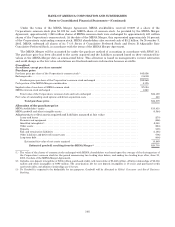

Balance, January 1 ............................................................... $2,481 $ 479

Additions .......................................................................... 910 3,035(1)

Amortization ....................................................................... (637) (360)

SalesofMSRs ...................................................................... (176) —

Valuation adjustment of MSRs(2) ...................................................... 228 (673)

Balance, December 31(3) ....................................................... $2,806 $2,481

(1) Includes $2.2 billion of Excess Spread Certificates converted to MSRs on June 1, 2004.

(2) For 2005 and 2004, includes $291 million and $(210) million related to change in value attributed to SFAS 133 hedged MSRs and

$63 million and $463 million of impairment.

(3) Net of impairment allowance of $257 million and $361 million for 2005 and 2004.

The estimated fair value of MSRs was $2.8 billion and $2.5 billion at December 31, 2005 and 2004.

The key economic assumptions used in valuations of MSRs include modeled prepayment rates and resultant

expected weighted average lives of the MSRs and the option adjusted spread (OAS) levels. An OAS model runs multiple

interest rate scenarios and projects prepayments specific to each one of those interest rate scenarios.

As of December 31, 2005, the modeled weighted average lives of MSRs related to fixed and adjustable rate loans

(including hybrid ARMs) were 4.94 years and 3.03 years. A decrease of 10 and 20 percent in modeled prepayments would

extend the expected weighted average lives for MSRs related to fixed rate loans to 5.26 years and 5.63 years, and would

extend the expected weighted average lives for MSRs related to adjustable rate loans to 3.30 years and 3.63 years. The

expected extension of weighted average lives would increase the value of MSRs by a range of $126 million to $269

million. An increase of 10 and 20 percent in modeled prepayments would reduce the expected weighted average lives for

MSRs related to fixed rate loans to 4.65 years and 4.40 years, and would reduce the expected weighted average lives for

MSRs related to adjustable rate loans to 2.81 years and 2.62 years. The expected reduction of weighted average lives

would decrease the value of MSRs by a range of $112 million to $212 million. A decrease of 100 and 200 basis points

(bps) in the OAS level would result in an increase in the value of MSRs ranging from $97 million to $202 million, and an

increase of 100 and 200 bps in the OAS level would result in a decrease in the value of MSRs ranging from $90 million to

$175 million.

For purposes of evaluating and measuring impairment, the Corporation stratifies the portfolio based on the

predominant risk characteristics of loan type and note rate. Indicated impairment, by risk stratification, is recognized as

a reduction in Mortgage Banking Income, through a valuation allowance, for any excess of adjusted carrying value over

estimated fair value.

Other Securitizations

As a result of the FleetBoston Merger in 2004, the Corporation acquired an interest in several credit card, home

equity loan and commercial loan securitization vehicles, which had aggregate debt securities outstanding of $4.1 billion

as of December 31, 2005.

At December 31, 2005 and 2004, the Corporation retained investment grade securities of $4.4 billion (including $2.6

billion issued in 2005) and $2.9 billion, which are valued using quoted market prices, in the AFS securities portfolio. At

December 31, 2005 there were no recognized servicing assets associated with these securitization transactions.

The Corporation has provided protection on a subset of one consumer finance securitization in the form of a

guarantee with a maximum payment of $220 million that will only be paid if over-collateralization is not sufficient to

absorb losses and certain other conditions are met. The Corporation projects no payments will be due over the remaining

life of the contract, which is less than one year.

117