Bank of America 2005 Annual Report Download - page 86

Download and view the complete annual report

Please find page 86 of the 2005 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

|

|

We manage credit risk based on the risk profile of the borrower or counterparty, repayment sources, the nature of

underlying collateral, and other support given current events, conditions and expectations. We classify our Loans and

Leases as either consumer or commercial and monitor their credit risk separately as discussed below.

Consumer Portfolio Credit Risk Management

Credit risk management for the consumer portfolio begins with initial underwriting and continues throughout a

borrower’s credit cycle. Statistical techniques are used to establish product pricing, risk appetite, operating processes

and metrics to balance risks and returns. Consumer exposure is grouped by product and other attributes for purposes of

evaluating credit risk. Statistical models are built using detailed behavioral information from external sources such as

credit bureaus as well as internal historical experience. These models are essential to our consumer credit risk

management process and are used in the determination of credit decisions, collections management strategies, portfolio

management decisions, determination of the allowance for consumer loan and lease losses, and economic capital

allocations for credit risk.

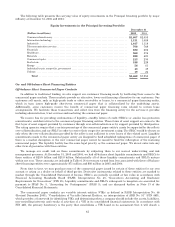

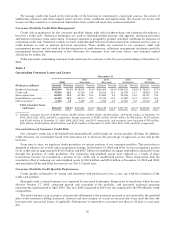

Table 8 presents outstanding consumer loans and leases for each year in the five-year period ending at December 31,

2005.

Table 8

Outstanding Consumer Loans and Leases

December 31

2005 2004

(Restated) 2003

(Restated) 2002

(Restated) 2001

(Restated)

(Dollars in millions) Amount Percent Amount Percent Amount Percent Amount Percent Amount Percent

Residential mortgage ......... $182,596 51.3% $178,079 54.3% $140,483 58.5% $108,332 54.8% $ 78,203 47.3%

Creditcard .................. 58,548 16.5 51,726 15.8 34,814 14.5 24,729 12.5 19,884 12.0

Homeequitylines ............ 62,098 17.5 50,126 15.3 23,859 9.9 23,236 11.8 22,107 13.4

Direct/Indirect consumer ...... 45,490 12.8 40,513 12.3 33,415 13.9 31,068 15.7 30,317 18.4

Other consumer(1) ............ 6,725 1.9 7,439 2.3 7,558 3.2 10,355 5.2 14,744 8.9

Total consumer loans

and leases ............ $355,457 100.0% $327,883 100.0% $240,129 100.0% $197,720 100.0% $165,255 100.0%

(1) Includes consumer finance of $2,849 million, $3,395 million, $3,905 million, $4,438 million, and $5,331 million at December 31,

2005, 2004, 2003, 2002, and 2001, respectively; foreign consumer of $3,841 million, $3,563 million, $1,969 million, $1,970 million,

and $2,092 million at December 31, 2005, 2004, 2003, 2002, and 2001, respectively; and consumer lease financing of $35 million,

$481 million, $1,684 million, $3,947 million, and $7,321 million at December 31, 2005, 2004, 2003, 2002, and 2001, respectively.

Concentrations of Consumer Credit Risk

Our consumer credit risk is diversified both geographically and through our various product offerings. In addition,

credit decisions are statistically based with tolerances set to decrease the percentage of approvals as the risk profile

increases.

From time to time, we purchase credit protection on certain portions of our consumer portfolio. This protection is

designed to enhance our overall risk management strategy. At December 31, 2005 and 2004, we have mitigated a portion

of our credit risk on approximately $110.4 billion and $88.7 billion of residential mortgage and indirect automobile loans

through the purchase of credit protection. Our regulatory risk-weighted assets were reduced as a result of these

transactions because we transferred a portion of our credit risk to unaffiliated parties. These transactions had the

cumulative effect of reducing our risk-weighted assets by $30.6 billion and $25.5 billion at December 31, 2005 and 2004,

and resulted in 28 bp and 26 bp increases in our Tier 1 Capital ratio.

Consumer Portfolio Credit Quality Performance

Credit quality continued to be strong and consistent with performance from a year ago with the exception of the

credit card portfolio.

Managed credit card performance was impacted by increased bankruptcy filings prior to legislation which became

effective October 17, 2005, continued growth and seasoning of the portfolio, and increased minimum payment

requirements implemented in April 2004. The year 2005 compared to 2004 was also impacted by the FleetBoston credit

card portfolio.

The entire balance of an account is contractually delinquent if the minimum payment is not received by the specified

date on the customer’s billing statement. Interest and fees continue to accrue on our past due loans until the date the

loan goes into nonaccrual status, if applicable. Delinquency is reported on accruing loans that are 30 days or more past

due.

50