Bank of America 2005 Annual Report Download - page 154

Download and view the complete annual report

Please find page 154 of the 2005 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

|

|

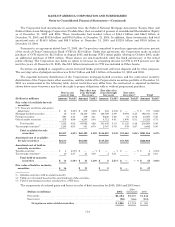

BANK OF AMERICA CORPORATION AND SUBSIDIARIES

Notes to Consolidated Financial Statements—(Continued)

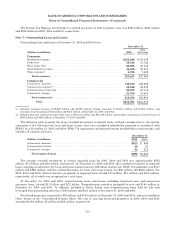

Key economic assumptions used in measuring the fair value of certain residual interests (included in Other Assets)

in securitizations and the sensitivity of the current fair value of residual cash flows to changes in those assumptions are

as follows:

Credit Card(1)

Subprime Consumer

Finance(2)

Automobile

Loans Commercial

Loans

(Dollars in millions) 2005 2004 2005 2004 2005 2004 2005 2004

Carrying amount of residual interests (at fair value)(3) ..... $ 203 $ 349 $ 290 $ 313 $93$34$92$ 130

Balance of unamortized securitized loans .................. 2,237 6,903 2,667 4,892 3,996 1,644 1,904 3,337

Weighted average life to call or maturity (in years)(4) ....... 0.5 1.2 0.8 1.3 1.6 1.4 1.8 1.8

Revolving structures—annual payment rate ............... 12.1% 13.7% 25.8% 26.0%

Amortizing structures—annual constant prepayment rate:

Fixed rate loans ....................................... 26.3-28.9% 28.3-32.7% 17.6-25.5% 24.9%

Adjustable rate loans .................................. 37.6 27.0-40.8 ——

Impact on fair value of 100 bps favorable change .............. $2$1$—$1$—$— $— $2

Impact on fair value of 200 bps favorable change .............. 32—11 1—12

Impact on fair value of 100 bps adverse change ................ (2) (1) (8) (9) (1) ——(1)

Impact on fair value of 200 bps adverse change ................ (3) (2) (9) (17) (1) (1) (1) (1)

Expected credit losses(5) ................................... 4.0-4.3% 5.3-9.7% 3.9-5.6% 5.1-11.3% 1.8-1.8% 1.6% 0.4% 0.4%

Impact on fair value of 10% favorable change ................. $3$18$7$27$7$3$1$1

Impact on fair value of 25% favorable change ................. 847 18 71 15 622

Impact on fair value of 10% adverse change ................... (3) (15) (7) (27) (6) (2) (1) (1)

Impact on fair value of 25% adverse change ................... (8) (27) (18) (68) (15) (6) (2) (2)

Residual cash flows discount rate (annual rate) ............ 12.0% 6.0-12.0% 30.0% 30.0% 15.0-20.0% 20.0% 12.3% 12.3%

Impact on fair value of 100 bps favorable change .............. $—$—$5$6$3$1$1$1

Impact on fair value of 200 bps favorable change .............. ——11 12 5112

Impact on fair value of 100 bps adverse change ................ ——(5) (6) (2) (1) (1) (1)

Impact on fair value of 200 bps adverse change ................ ——(10) (12) (5) (1) (1) (2)

(1) The impact of changing residual cash flows discount rates is immaterial.

(2) Subprime consumer finance includes subprime real estate loan securitizations, which are serviced by third parties.

(3) Residual interests include interest-only strips, one or more subordinated tranches, accrued interest receivable, and in some cases, a cash reserve

account.

(4) Before any optional clean-up calls are executed, economic analysis will be performed.

(5) Annual rates of expected credit losses are presented for credit card, home equity lines and commercial securitizations. Cumulative lifetime rates of

expected credit losses (incurred plus projected) are presented for subprime consumer finance securitizations and auto securitizations.

The sensitivities in the preceding table are hypothetical and should be used with caution. As the amounts indicate,

changes in fair value based on variations in assumptions generally cannot be extrapolated because the relationship of

the change in assumption to the change in fair value may not be linear. Also, the effect of a variation in a particular

assumption on the fair value of the retained interest is calculated without changing any other assumption. In reality,

changes in one factor may result in changes in another, which might magnify or counteract the sensitivities.

Additionally, the Corporation has the ability to hedge interest rate risk associated with retained residual positions. The

above sensitivities do not reflect any hedge strategies that may be undertaken to mitigate such risk.

Static pool net credit losses are considered in determining the value of retained interests. Static pool net credit

losses include actual losses incurred plus projected credit losses divided by the original balance of each securitization

pool. For auto loan securitizations, weighted average static pool net credit losses for securitizations entered into in 2005

were 1.77 percent for the year ended December 31, 2005. For securitizations entered into in 2004, the weighted average

static pool net credit losses were 1.79 percent for the year ended December 31, 2005, and 1.63 percent for the year ended

December 31, 2004. For the subprime consumer finance securitizations, weighted average static pool net credit losses for

securitizations entered into in 2001 were 5.50 percent for the year ended December 31, 2005, and 5.93 percent for the

year ended December 31, 2004. For securitizations entered into in 1999, the weighted average static pool net credit

losses were 9.16 percent for the year ended December 31, 2005, and 12.22 percent for the year ended December 31, 2004.

Proceeds from collections reinvested in revolving credit card securitizations were $2.0 billion and $6.8 billion in 2005

and 2004. Credit card servicing fee income totaled $97 million and $134 million in 2005 and 2004. Other cash flows

received on retained interests, such as cash flows from interest-only strips, were $206 million and $345 million in 2005

and 2004, for credit card securitizations. Proceeds from collections reinvested in revolving commercial loan

securitizations were $8.7 billion and $7.5 billion in 2005 and 2004. Servicing fees and other cash flows received on

retained interests, such as cash flows from interest-only strips, were $3 million and $34 million in 2005, and $4 million

and $11 million in 2004 for commercial loan securitizations.

The Corporation reviews its loans and leases portfolio on a managed basis. Managed loans and leases are defined as

on-balance sheet Loans and Leases as well as loans in revolving securitizations, which include credit cards, home equity

lines and commercial loans. New advances on accounts for which previous loan balances were sold to the securitization

trusts will be recorded on the Corporation’s Consolidated Balance Sheet after the revolving period of the securitization,

which has the effect of increasing Loans and Leases on the Corporation’s Consolidated Balance Sheet and increasing Net

118