Bank of America 2005 Annual Report Download - page 9

Download and view the complete annual report

Please find page 9 of the 2005 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

|

|

8 Bank of America 2005

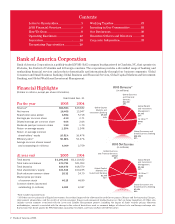

How We Grow: 2005 Financial Overview

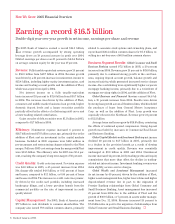

Earning a record $16.5 billion

Double-digit year-over-year growth in net income, earnings per share and revenue

In 2005 Bank of America earned a record $16.5 billion,

as revenue growth accompanied by strong operating

leverage drove an 18 percent increase in profit over 2004.

Diluted earnings per share rose 11 percent to $4.04. Return

on average common equity for the year was 17 percent.

Revenue: Fully taxable-equivalent revenue grew 15 percent

to $56.9 billion from $49.7 billion in 2004. Revenue growth

was driven by a 21 percent increase in noninterest income to

$25.4 billion, including higher equity investment gains, card

income and trading account profits and the addition of Fleet,

which was acquired on April 1, 2004.

Net interest income on a fully taxable-equivalent

basis increased 10 percent to $31.6 billion from $28.7 billion

in 2004. The increase was driven by the addition of Fleet,

consumer and middle market business loan growth, higher

domestic deposit levels and a larger securities portfolio

partially offset by the effects of a flattening yield curve and

a lower trading-related contribution.

Gains on sales of debt securities were $1.1 billion in 2005,

compared to $1.7 billion in 2004.

Efficiency: Noninterest expense increased 6 percent to

$28.7 billion from $27.0 billion a year ago, primarily due to the

addition of Fleet and an investment in the capital markets

business. Included in 2005 expenses were $412 million in

pre-tax merger and restructuring charges related to the Fleet

merger. Full-year 2005 cost savings from the merger with Fleet

were $1.85 billion. The efficiency ratio for 2005 was 50.4 per-

cent, reaching the company’s long-term target of 50 percent.

Credit Quality: Credit costs increased. Provision expense

was $4.0 billion in 2005, a 45 percent increase from 2004.

Net charge-offs totaled $4.6 billion, or 0.85 percent of loans

and leases, compared to $3.1 billion, or 0.66 percent of loans

and leases in 2004. The increase in credit costs was primar-

ily driven by the credit card portfolio, including increased

bankruptcy filings, and a lower provision benefit from the

commercial portfolio as the rate of improvement in credit

quality slowed.

Capital Management: For 2005, Bank of America paid

$7.7 billion in cash dividends to common shareholders. The

company also issued 79.6 million common shares, primarily

related to associate stock options and ownership plans, and

repurchased 126.4 million common shares for $5.8 billion, re-

sulting in a net decrease of 46.9 million common shares.

Business Segment Results: Global Consumer and Small

Business Banking earned $7.2 billion in 2005, a 20 percent

increase from 2004. Revenue grew 15 percent to $28.9 billion,

primarily due to continued strong growth in the card busi-

ness, ongoing deposit account growth, balance growth and

increased activity, which generated increased service charge

income. Also contributing were significantly higher corporate

mortgage banking income, primarily due to a writedown of

mortgage servicing rights in 2004, and the addition of Fleet.

Global Business and Financial Services earned $4.6 bil-

lion, a 19 percent increase from 2004. Results were driven

by strong loan growth across all business lines, which included

the purchase of loans from General Motors Acceptance

Corp. as well as the addition of Fleet. Loan growth was

especially robust in the Northeast. Revenue grew 21 percent

to $11.2 billion.

Average loans and leases grew by $28.8 billion, countering

the effects of continued spread compression. Strong deposit

growth was fueled by increases in Commercial Real Estate

and Business Banking.

Global Capital Markets and Investment Banking net income

declined 10 percent to $1.7 billion in 2005, primarily due

to a decline in the provision benefit as a result of slowing

improvement in credit quality. Revenue was essentially

unchanged at $9.0 billion in 2005 and 2004. Noninterest

income increased 14 percent, led by trading profits and equity

commissions that more than offset the decline in trading-

related net interest income. Investment banking revenue was

down slightly, as were service charges.

Global Wealth and Investment Management increased

its net income by 49 percent, driven by the addition of Fleet,

higher asset management fees, higher loan volume and higher

deposit-related revenue due in part to the migration of

Premier Banking relationships from Global Consumer and

Small Business Banking. Asset management fees increased

21 percent from 2004 due to the addition of Fleet and the

growth of $30.9 billion, or 7 percent, in assets under manage-

ment from Dec. 31, 2004. Revenue increased 25 percent to

$7.4 billion due in part to the migration of relationships from

Global Consumer and Small Business Banking.