Bank of America 2005 Annual Report Download - page 73

Download and view the complete annual report

Please find page 73 of the 2005 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

|

|

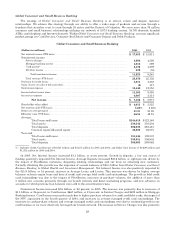

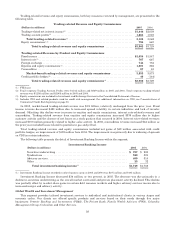

Global Capital Markets and Investment Banking

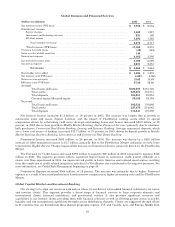

(Dollars in millions) 2005 2004

Net interest income (FTE basis):

Core net interest income ................................................ $ 1,854 $ 2,019

Trading-related net interest income ...................................... 1,444 2,039

Total net interest income ............................................ 3,298 4,058

Noninterest income:

Servicecharges ........................................................ 1,146 1,287

Investment and brokerage services ....................................... 806 705

Investment banking income ............................................. 1,749 1,783

Trading account profits ................................................. 1,664 1,023

Allotherincome ....................................................... 346 190

Total noninterest income ............................................ 5,711 4,988

Total revenue (FTE basis) .................................................. 9,009 9,046

Provision for credit losses ....................................................... (244) (445)

Gains (losses) on sales of debt securities .......................................... 117 (10)

Noninterest expense ........................................................... 6,678 6,581

Income before income taxes ..................................................... 2,692 2,900

Incometaxexpense ............................................................ 956 976

Net income .......................................................... $ 1,736 $ 1,924

Shareholder value added ....................................................... $ 642 $ 873

Net interest yield (FTE basis) ................................................... 0.92% 1.47%

Returnonaverageequity....................................................... 16.73 19.34

Efficiency ratio (FTE basis) ..................................................... 74.13 72.76

Average:

Totalloansandleases .................................................. $ 34,353 $ 33,891

Trading-related earning assets .......................................... 299,374 227,230

Total assets ........................................................... 410,979 321,743

Total deposits ......................................................... 84,979 74,738

Common equity/Allocated equity ......................................... 10,372 9,946

Period end:

Totalloansandleases .................................................. 40,213 33,387

Trading-related earning assets .......................................... 282,456 189,596

Total assets ........................................................... 395,900 303,897

Total deposits ......................................................... 86,144 76,986

Net Interest Income declined $760 million, or 19 percent, in 2005. Driving the decrease was lower trading-related

Net Interest Income of $595 million, or 29 percent. Despite the growth in average trading-related earning assets of $70.9

billion, or 33 percent, the contribution to Net Interest Income decreased due to a flattening yield curve. In 2005, core net

interest income decreased $165 million to $1.9 billion primarily due to spread compression. Average Deposits increased

$10.2 billion, or 14 percent, due to higher foreign deposits and escrow balances.

Noninterest Income increased $723 million, or 14 percent, in 2005. Driving the increase were higher Trading

Account Profits of $641 million, Equity Investment Gains (included in all other income) of $123 million and Investment

and Brokerage Services of $101 million. The increase in Trading Account Profits was due to growth in average trading-

related earning assets as a result of increased client activity as we continued to invest in the business. These increases

were partially offset by declines in Service Charges of $141 million due to effects of rising earnings credits on balances

required for services and lower Investment Banking Income of $34 million.

Provision for Credit Losses increased $201 million to negative $244 million in 2005, compared to negative $445

million in 2004, driven by a slower rate of improvement in commercial credit quality. Net charge-offs declined $245

million from the prior year, driven partially by increased recoveries. For more information, see Credit Risk Management

beginning on page 49.

Noninterest Expense remained relatively unchanged in 2005. Other general operating expense decreased primarily

due to the segment’s share of the mutual fund settlement and other litigation reserves recorded in 2004. This decrease

was offset by higher Personnel expense, including costs associated with the strategic initiative.

37