Bank of America 2005 Annual Report Download - page 161

Download and view the complete annual report

Please find page 161 of the 2005 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

169 -

170

170 -

171

171 -

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

|

|

BANK OF AMERICA CORPORATION AND SUBSIDIARIES

Notes to Consolidated Financial Statements—(Continued)

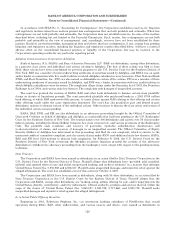

Note 13—Commitments and Contingencies

In the normal course of business, the Corporation enters into a number of off-balance sheet commitments. These

commitments expose the Corporation to varying degrees of credit and market risk and are subject to the same credit and

market risk limitation reviews as those instruments recorded on the Corporation’s Consolidated Balance Sheet.

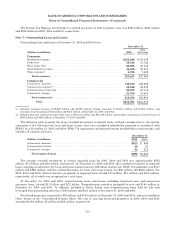

Credit Extension Commitments

The Corporation enters into commitments to extend credit such as loan commitments, SBLCs and commercial

letters of credit to meet the financing needs of its customers. The outstanding unfunded lending commitments shown in

the following table have been reduced by amounts participated to other financial institutions of $30.4 billion and $23.4

billion at December 31, 2005 and 2004. The carrying amount for these commitments, which represents the liability

recorded related to these instruments, at December 31, 2005 and 2004 was $458 million and $520 million. At

December 31, 2005, the carrying amount included deferred revenue of $63 million and a reserve for unfunded lending

commitments of $395 million. At December 31, 2004, the carrying amount included deferred revenue of $118 million and

a reserve for unfunded lending commitments of $402 million.

December 31

(Dollars in millions) 2005 2004

Loan commitments(1) ........................................................... $277,757 $245,042

Homeequitylinesofcredit ...................................................... 78,626 60,128

Standby letters of credit and financial guarantees .................................. 43,095 42,850

Commercial letters of credit ..................................................... 5,154 5,653

Legallybindingcommitments................................................ 404,632 353,673

Creditcardlines ............................................................... 192,968 165,694

Total ................................................................. $597,600 $519,367

(1) At December 31, 2005 and 2004, there were equity commitments of $1.4 billion and $2.0 billion, related to obligations to further

fund Principal Investing equity investments.

Legally binding commitments to extend credit generally have specified rates and maturities. Certain of these

commitments have adverse change clauses that help to protect the Corporation against deterioration in the borrowers’

ability to pay.

The Corporation issues SBLCs and financial guarantees to support the obligations of its customers to beneficiaries.

Additionally, in many cases, the Corporation holds collateral in various forms against these SBLCs. As part of its risk

management activities, the Corporation continuously monitors the creditworthiness of the customer as well as SBLC

exposure; however, if the customer fails to perform the specified obligation to the beneficiary, the beneficiary may draw

upon the SBLC by presenting documents that are in compliance with the letter of credit terms. In that event, the

Corporation either repays the money borrowed or advanced, makes payment on account of the indebtedness of the

customer or makes payment on account of the default by the customer in the performance of an obligation to the

beneficiary up to the full notional amount of the SBLC. The customer is obligated to reimburse the Corporation for any

such payment. If the customer fails to pay, the Corporation would, as contractually permitted, liquidate collateral and/or

set off accounts.

Commercial letters of credit, issued primarily to facilitate customer trade finance activities, are usually

collateralized by the underlying goods being shipped to the customer and are generally short-term. Credit card lines are

unsecured commitments that are not legally binding. Management reviews credit card lines at least annually, and upon

evaluation of the customers’ creditworthiness, the Corporation has the right to terminate or change certain terms of the

credit card lines.

The Corporation uses various techniques to manage risk associated with these types of instruments that include

obtaining collateral and/or adjusting commitment amounts based on the borrower’s financial condition; therefore, the

total commitment amount does not necessarily represent the actual risk of loss or future cash requirements. For each of

these types of instruments, the Corporation’s maximum exposure to credit loss is represented by the contractual amount

of these instruments.

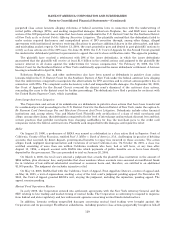

Other Commitments

At December 31, 2005 and 2004, charge cards (nonrevolving card lines) to individuals and government entities

guaranteed by the U.S. government in the amount of $9.4 billion and $10.9 billion were not included in credit card

125