Bank of America 2005 Annual Report Download - page 55

Download and view the complete annual report

Please find page 55 of the 2005 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

|

|

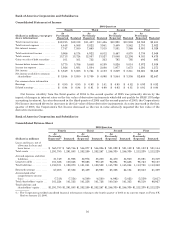

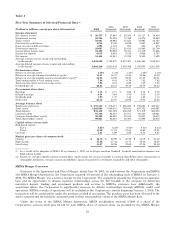

Financial Highlights

Net Interest Income

Net Interest Income on a FTE basis increased $2.9 billion to $31.6 billion in 2005 compared to 2004. The primary

drivers of the increase were the FleetBoston Merger, organic growth in consumer (primarily credit card and home

equity) and commercial loans, higher domestic deposit levels and a larger ALM portfolio (primarily securities). Partially

offsetting these increases was the adverse impact of spread compression due to the flattening of the yield curve, which

contributed to lower Net Interest Income. The net interest yield on a FTE basis declined 33 basis points (bps) to 2.84

percent in 2005. This was primarily due to the adverse impact of an increase in lower-yielding, trading-related balances

and spread compression, which was partially offset by growth in core deposit and consumer loans. For more information

on Net Interest Income on a FTE basis, see Table I on page 80.

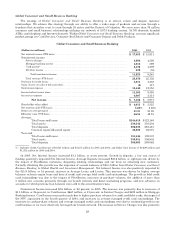

Noninterest Income

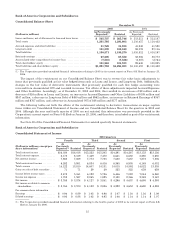

Noninterest Income

(Dollars in millions) 2005 2004

(Restated)

Servicecharges ........................................................ $ 7,704 $ 6,989

Investment and brokerage services ....................................... 4,184 3,614

Mortgage banking income ............................................... 805 414

Investment banking income ............................................. 1,856 1,886

Equity investment gains ................................................ 2,040 863

Cardincome .......................................................... 5,753 4,592

Trading account profits ................................................. 1,812 869

Otherincome.......................................................... 1,200 1,778

Total noninterest income ......................................... $25,354 $21,005

Noninterest Income increased $4.3 billion to $25.4 billion for 2005 compared to 2004, due to the following which

includes the impact of FleetBoston:

• Service Charges grew $715 million driven by organic account growth.

• Investment and Brokerage Services increased $570 million due to increases in asset management fees and mutual

fund fees.

• Mortgage Banking Income increased $391 million due to lower MSR impairment charges which were partially

offset by lower production income.

• Equity Investment Gains increased $1.2 billion, primarily in Principal Investing, as liquidity in the private equity

markets increased.

• Card Income increased $1.2 billion due to increased interchange income and merchant discount fees driven by

growth in debit and credit purchase volumes and the acquisition of NPC.

• Trading Account Profits increased $943 million due to increased customer activity driven by our strategic

initiative in Global Capital Markets and Investment Banking to expand business capabilities and opportunities,

and the absence of a writedown of the Excess Spread Certificates (the Certificates) that occurred in the prior year.

For more information on the Certificates, see Note 1 of the Consolidated Financial Statements.

• Other Income decreased $578 million primarily related to losses on derivative instruments used as economic

hedges in the ALM process that did not qualify for SFAS 133 hedge accounting.

Provision for Credit Losses

The Provision for Credit Losses increased $1.2 billion to $4.0 billion in 2005 with credit card being the primary

driver of the increase. Consumer credit card net charge-offs increased $1.3 billion from 2004 to $3.7 billion with an

estimated $578 million related to the increase in bankruptcy filings prior to the effective date of the new bankruptcy

legislation enacted in the fourth quarter of 2005. We estimate that approximately 70 percent of these bankruptcy-related

charge-offs represent acceleration from 2006 and were provided for previously. Also impacting credit card net charge-offs

and the Provision for Credit Losses were organic growth and seasoning of the portfolio, the impact of the FleetBoston

portfolio and new advances on accounts for which previous loan balances were sold to the securitization trusts. The

provision also increased as the rate of credit quality improvement slowed in the commercial portfolio and a $50 million

reserve was established for estimated losses associated with Hurricane Katrina. Partially offsetting these increases was

a reduction in the reserves of $250 million due to reduced uncertainties resulting from the completion of credit-related

integration activities for FleetBoston.

19