Bank of America 2005 Annual Report Download - page 99

Download and view the complete annual report

Please find page 99 of the 2005 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

|

|

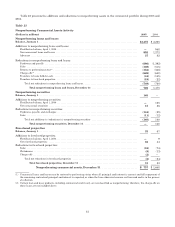

Included within the second component of the Allowance for Loan and Lease Losses are previously unallocated

reserves maintained to cover uncertainties that affect our estimate of probable losses including the imprecision inherent

in the forecasting methodologies, domestic and global economic uncertainty, large single name defaults and event risk.

In the fourth quarter of 2005, we assigned these reserves to our individual products to better reflect our view of risk in

these portfolios.

We monitor differences between estimated and actual incurred loan and lease losses. This monitoring process

includes periodic assessments by senior management of loan and lease portfolios and the models used to estimate

incurred losses in those portfolios.

Additions to the Allowance for Loan and Lease Losses are made by charges to the Provision for Credit Losses. Credit

exposures deemed to be uncollectible are charged against the Allowance for Loan and Lease Losses. Recoveries of

previously charged off amounts are credited to the Allowance for Loan and Lease Losses.

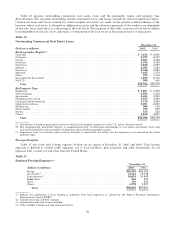

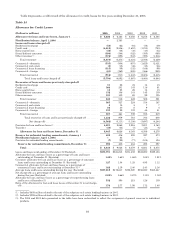

The Allowance for Loan and Lease Losses for the consumer portfolio as presented in Table 25 increased $137 million

from December 31, 2004 to $4.5 billion at December 31, 2005. Credit card accounted for $153 million of this increase and

was primarily driven by new advances on accounts for which previous loan balances were sold to the securitization

trusts, organic growth and continued seasoning which resulted in higher loss expectations. These increases were mostly

offset by the use of reserves to absorb the estimated bankruptcy net charge-off acceleration from 2006. Increases in the

allowance for non-credit card consumer products were driven by broad-based loan growth and seasoning, with the

exception of the other consumer product category which decreased as a result of the run-off portfolios from our

previously exited consumer businesses.

The allowance for commercial loan and lease losses was $3.5 billion at December 31, 2005, a $718 million decrease

from December 31, 2004. This decrease resulted from continued improvement in commercial credit quality, including

reduced exposure and an improved risk profile in Latin America, the use of reserves to absorb a portion of domestic

airline charge-offs and a reduction of reserves due to reduced uncertainties resulting from the completion of credit-

related integration activities for FleetBoston during 2005.

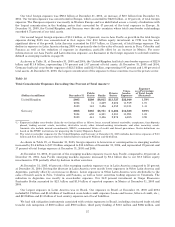

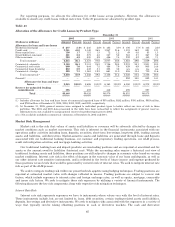

Reserve for Unfunded Lending Commitments

In addition to the Allowance for Loan and Lease Losses, we also estimate probable losses related to unfunded

lending commitments, such as letters of credit and financial guarantees, and binding unfunded loan commitments.

Unfunded lending commitments are subject to individual reviews, and are analyzed and segregated by risk according to

our internal risk rating scale. These risk classifications, in conjunction with an analysis of historical loss experience,

current economic conditions and performance trends within specific portfolio segments, and any other pertinent

information result in the estimation of the reserve for unfunded lending commitments. The reserve for unfunded lending

commitments is included in Accrued Expenses and Other Liabilities on the Consolidated Balance Sheet.

We monitor differences between estimated and actual incurred credit losses upon draws of the commitments. This

monitoring process includes periodic assessments by senior management of credit portfolios and the models used to

estimate incurred losses in those portfolios.

Changes to the reserve for unfunded lending commitments are made through the Provision for Credit Losses. The

reserve for unfunded lending commitments at December 31, 2005 was $395 million, a decrease of $7 million from

December 31, 2004.

63