Bank of America 2005 Annual Report Download - page 108

Download and view the complete annual report

Please find page 108 of the 2005 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

|

|

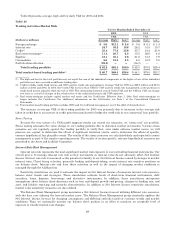

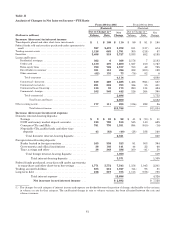

The following table includes derivatives utilized in our ALM process, including those designated as SFAS 133

hedges and those used as economic hedges that do not qualify for SFAS 133 hedge accounting treatment. The fair value

of net ALM contracts decreased from $3.4 billion at December 31, 2004 to $(386) million at December 31, 2005. The

decrease was attributable to decreases in the value of options, foreign exchange contracts and futures and forward rate

contracts, partially offset by increases in the value of interest rate swaps. The decrease in the value of options was due to

reduction in outstanding option positions due to terminations, maturities and decreases in the values of remaining open

options positions. The decrease in the value of foreign exchange contracts was due to the strengthening of the U.S. dollar

against most foreign currencies during 2005. The decrease in the value of futures and forward rate contracts was due to

the impact of increases in interest rates during 2005 on long futures and forward rate contracts.

Table 29

Asset and Liability Management Interest Rate and Foreign Exchange Contracts

December 31, 2005 Expected Maturity Average

Estimated

Duration

(Dollars in millions, average

estimated duration in years) Fair

Value Total 2006 2007 2008 2009 2010 Thereafter

Receive fixed interest rate

swaps(1) .................... $(1,390) 4.17

Notional amount ............ $108,985 $ 4,337 $ 13,080 $ 6,144 $39,107 $10,387 $35,930

Weighted average fixed

rate ..................... 4.62% 4.75% 4.66% 4.02% 4.51% 4.43% 4.77%

Pay fixed interest rate

swaps(1) .................... (408) 3.85

Notional amount ............ $102,281 $ 5,100 $ 55,925 $10,152 $ — $ — $31,104

Weighted average fixed

rate ..................... 4.61% 3.23% 4.46% 4.24% — % — % 5.21%

Basisswaps .................. (644)

Notional amount(3) .......... $ 17,806 $ 514 $ 174 $ 884 $ 2,839 $ 3,094 $10,301

Option products(2) ............. 1,349

Notional amount(3) .......... 57,246 — — 57,246 — — —

Foreign exchange contracts .... 909

Notional amount ............ 16,061 1,335 51 1,436 1,826 3,485 7,928

Futures and forward rate

contracts(4) ................. (202)

Notional amount(3) .......... 34,71634,716———— —

Net ALM contracts ...... $ (386)

December 31, 2004 Expected Maturity Average

Estimated

Duration

(Dollars in millions, average

estimated duration in years) Fair

Value Total 2005 2006 2007 2008 2009 Thereafter

Receive fixed interest rate

swaps(1) .................... $ (880) 4.43

Notional amount ............ $167,324 $ 2,580 $ 7,290 $ 23,598 $46,917 $25,601 $61,338

Weighted average fixed

rate ..................... 4.04% 4.78% 4.52% 3.11% 3.47% 3.83% 4.83%

Pay fixed interest rate

swaps(1) .................... (2,248) 4.77

Notional amount ............ $157,837 $ 39 $ 6,320 $62,584 $16,136 $ 10,289 $ 62,469

Weighted average fixed

rate ..................... 4.24% 5.01% 3.54% 3.58% 3.91% 3.85% 5.13%

Basisswaps .................. (4)

Notional amount(3) .......... $ 6,700 $ 500 $ 4,400 $ — $ — $ — $ 1,800

Option products(2) ............. 3,492

Notional amount(3) .......... 323,835 145,200 90,000 17,500 58,404 — 12,731

Foreign exchange contracts .... 2,748

Notional amount ............ 13,606 71 1,529 55 1,587 2,091 8,273

Futures and forward rate

contracts(4) ................. 287

Notional amount(3) .......... (10,889) 10,111 (21,000) — — — —

Net ALM contracts ...... $ 3,395

(1) At December 31, 2005, $46.6 billion of the receive fixed swap notional amount and $41.9 billion of the pay fixed swap notional

amount represented forward starting swaps that will not be effective until their respective contractual start dates. At December 31,

2004, $39.9 billion of the receive fixed swap notional amount and $75.9 billion of the pay fixed swap notional amount represented

forward starting swaps that will not be effective until their respective contractual start dates.

(2) Option products include caps, floors, swaptions and exchange-traded options on index futures contracts. These strategies may

include option collars or spread strategies, which involve the buying and selling of options on the same underlying security or

interest rate index.

(3) Reflects the net of long and short positions.

(4) Futures and forward rate contracts include Eurodollar futures, U.S. Treasury futures, and forward purchase and sale contracts.

72