Bank of America 2005 Annual Report Download - page 67

Download and view the complete annual report

Please find page 67 of the 2005 Bank of America annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

|

|

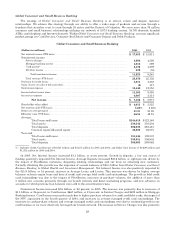

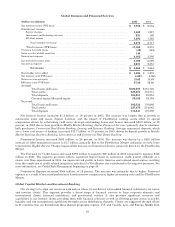

Held Provision for Credit Losses increased $887 million to $4.0 billion in 2005, driven primarily by higher net

charge-offs. Consumer card net charge-offs were $3.7 billion, or 6.76 percent in 2005 compared to $2.3 billion, or 5.31

percent in 2004. Higher credit card net charge-offs were driven by an increase in bankruptcy related charge-offs of $578

million as card customers “rushed to file” ahead of the new bankruptcy law. Also impacting net charge-offs were organic

portfolio growth and seasoning, increases effective in 2004 in credit card minimum payment requirements, the impact of

FleetBoston and new advances on accounts for which previous loan balances were sold to the securitization trusts. We

estimate that approximately 70 percent of the increased bankruptcy-related charge-offs represent acceleration from

2006. Excluding bankruptcy-related charge-offs representing acceleration from 2006 and charge-offs associated with the

2004 changes in credit card minimum payment requirements that were provided for in late 2004, the increased net

charge-offs were the primary driver of the higher Provision for Credit Losses. In addition, the Provision for Credit Losses

was impacted by new advances on accounts for which previous loan balances were sold to the securitization trusts, and

the establishment of reserves in 2005 for additional changes made in late 2005 in credit card minimum payment

requirements.

Managed card revenue increased $1.3 billion, or 15 percent, to $9.4 billion in 2005, driven by a $474 million, or nine

percent, increase in managed Net Interest Income, and a $778 million, or 25 percent increase, in managed Noninterest

Income. Average managed credit card outstandings were $59.0 billion in 2005 compared to $50.3 billion in 2004. The

impact of FleetBoston and organic growth drove the increases in 2005.

Managed consumer credit card net losses were $4.1 billion, or 6.92 percent of total average managed credit card

loans in 2005, compared to $2.8 billion, or 5.62 percent in 2004. Higher managed credit card net losses were driven by an

increase in bankruptcy net losses resulting from the change in the bankruptcy law, continued growth and seasoning,

increases effective in 2004 in credit card minimum payment requirements and the impact of FleetBoston. For more

information, see Credit Risk Management beginning on page 49.

Consumer Real Estate

Consumer Real Estate generates revenue by providing an extensive line of mortgage products and services to

customers nationwide. Consumer Real Estate products are available to our customers through a retail network of

personal bankers located in 5,873 banking centers, dedicated sales account executives in over 150 locations and through

a dedicated sales force offering our customers direct telephone and online access to our products. Additionally, we serve

our customers through a partnership with more than 6,600 mortgage brokers in 49 states. The mortgage product

offerings for home purchase and refinancing needs include fixed and adjustable rate loans, and home equity lines of

credit. To manage this portfolio, these products are either sold into the secondary mortgage market to investors while

retaining Bank of America customer relationships or are held on our balance sheet for ALM purposes.

Consumer Real Estate is managed with a focus on its two primary businesses, first mortgage and home equity. The

first mortgage business includes the origination, fulfillment and servicing of first mortgage loan products. Servicing

activities primarily include collecting cash for principal, interest and escrow payments from borrowers, and accounting

for and remitting principal and interest payments to investors. Servicing income includes ancillary income derived in

connection with these activities, such as late fees. The home equity business includes lines of credit and second

mortgages. These two businesses provide us with a business model that meets customer real estate borrowing needs in

various interest rate cycles.

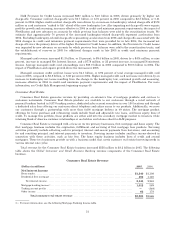

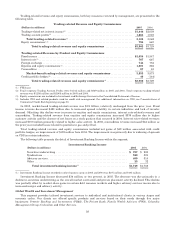

Total revenue for the Consumer Real Estate business increased $558 million to $3.2 billion in 2005. The following

table shows the Global Consumer and Small Business Banking revenue components of the Consumer Real Estate

business.

Consumer Real Estate Revenue

(Dollars in millions) 2005 2004

Net Interest Income

Homeequity................................................................................. $1,340 $1,108

Residential first mortgage ..................................................................... 806 1,140

Netinterestincome ....................................................................... 2,146 2,248

Mortgage banking income(1) .................................................................... 1,012 589

Trading account profits ....................................................................... —(349)

Otherincome ................................................................................ 66 178

Total consumer real estate revenue ................................................. $3,224 $2,666

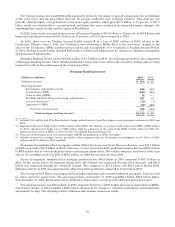

(1) For more information, see the following Mortgage Banking Income table.

31